At the beginning of 2023, A-shares have reversed their two-year decline and headed upwards. In January, with only 16 trading days, the CSI 300 Index rose by 7.37%, and this year (to February 1) it rose by 7.99%.

People’s minds are focused on the equity market, and they seem to have forgotten the existence of the bond market. Perhaps they have not yet emerged from the shadow of the sharp drop in the pure bond market in November last year?

In fact, with the rapid recovery of the equity market, “fixed income +” funds (including equity and debt bases) also performed well in January .

” China Securities Non-Pure Bond Index ” has increased by 1.70% this year (to February 1);

” Wonder Partial Debt Hybrid Fund Index ” has increased by 2.09% this year (to February 1);

The ” Wind Hybrid Bond Secondary Fund Index ” has increased by 2.13% this year (to February 1);

” Wind Convertible Bond Fund Index ” has increased by 7.39% this year (to February 1);

” China Securities Convertible Bond Fund Index ” has increased by 8.01% this year (to February 1);

Interpretation of #2022Four Seasons Report#

Next, let’s interpret the four seasons reports of several “fixed income +” funds ( held by me ) to see what happened on the eve of the market recovery (the fourth quarter of last year).

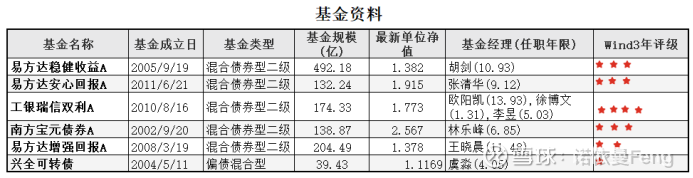

1. Several “fixed income +” funds held by me

I have disclosed these funds in my 2022 fund holdings in the long article ” 2022 Fund Investment Summary: Grow in Sharing, Sharing Weekly Harvest “.

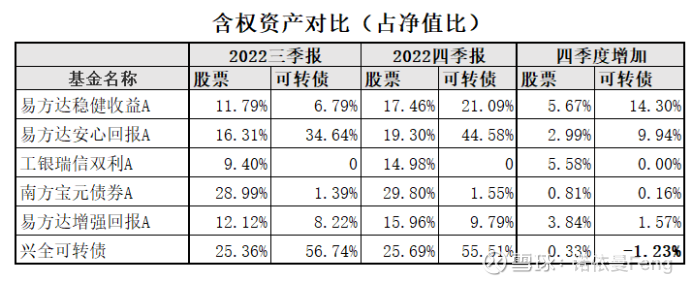

In the first and fourth quarters, equity assets were generally increased

1. Equity assets generally increased in the fourth quarter

Both the secondary debt base and partial debt mixed base can allocate a certain proportion of stocks; and convertible bonds themselves are bonds and can be converted into shares. They are both debt and equity, and they are equity-containing assets.

E Fund achieved stable returns. In the fourth quarter, the ratio of stocks to (net value) increased by 5.67%, and the ratio of convertible bonds to (net value) increased by 14.30%. It is the highest proportion of equity assets among the six funds.

ICBC Credit Suisse Shuangli has no convertible bond assets, and stock assets increased from 9.40% to 14.98%, an increase of 5.58%;

E Fund’s reassuring return is the one with the highest equity ratio among the five secondary debt funds, with the proportion of stocks increasing by 2.99% and convertible bonds increasing by 9.94%;

Nanfang Baoyuan bonds have the highest proportion of stocks in the secondary debt base, and the allocation of convertible bonds is relatively small; the increase in equity-containing assets in the fourth quarter is relatively small;

Xingquan convertible bond, although it is a bond fund, but the convertible bond itself is a right-containing asset, and a relatively high proportion of stock assets is allocated at the same time; the stock increased slightly in the fourth quarter, and the convertible bond decreased by 1.23%; it is six funds Among them, the ratio of the only right-containing asset allocation is reduced.

2. Asset allocation in the fourth quarter

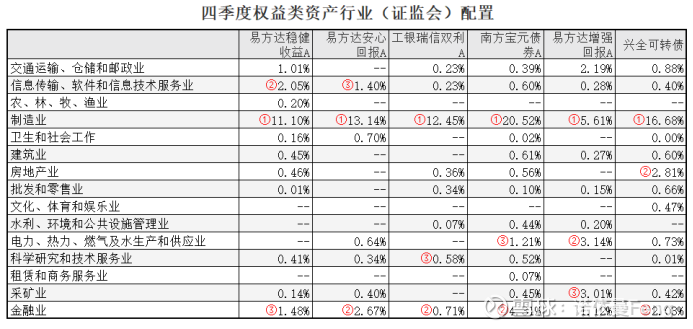

(1) Industry allocation of stocks (according to the industry classification of the China Securities Regulatory Commission, which is consistent with that disclosed by the fund)

The funds generally focus on the manufacturing and financial industries; they all regard the manufacturing industry as the largest industry allocation, and the financial industry as the second and third largest industry allocations.

Most of the other generally allocated industries are industries damaged by the epidemic, such as transportation, warehousing and postal services, wholesale and retail; and information transmission, software and information technology services, which have experienced large declines.

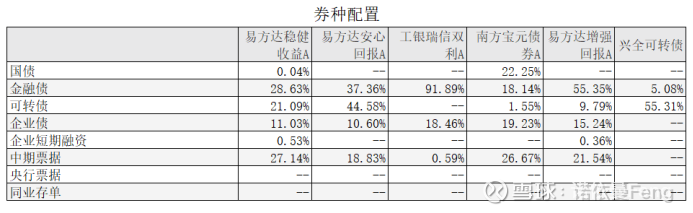

(2) Types of bond allocation

ICBC Credit Suisse Shuangli and E Fund Enhanced Return mainly focus on financial bond allocation; E Fund Anxin Return and Xingquan Convertible Bond mainly focus on convertible bond allocation; ) mainly; Nanfang Baoyuan also allocated a relatively high proportion of national debt;

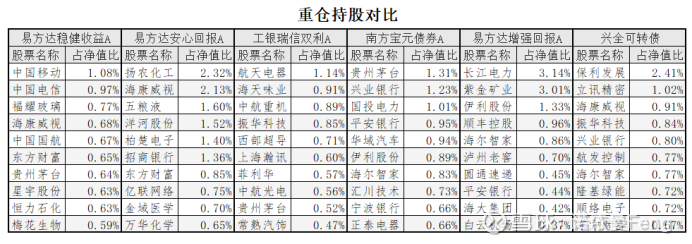

3. Heavy positions in stocks and bonds

(1) Top 10 heavily held stocks

The stocks allocated by each fund are quite different. Even for funds of the same company (E Fund has 3 funds), the selection of individual stocks is also different. In comparison, E Fund’s stable income and E Fund’s reassuring return are more comparable (from the previous industry configuration, it can also be seen that the top three industries have the same configuration), all of which are equipped with food and beverage, consumer electronics, finance, chemical industry, electronics, etc. and other sub-sectors.

2) Top five most heavily held bonds

The top five of Nanfang Baoyuan, which allocates up to 22.25% of government bonds, are all government bonds, while ICBC Credit Suisse Shuangli, which takes financial bonds as the largest bond allocation, has allocated four bank perpetual bonds among the top five; Among the top five convertible bonds, E Fund Anxin Return and Xingquan Convertible Bonds have three convertible bonds.

4. The specific operation of each fund in the fourth quarter

(1) E Fund’s stable income

The portfolio actively adjusted the allocation of major categories of assets, increased the risk exposure of equity and the proportion of convertible bond allocation, and reduced the duration and position of bonds. The portfolio has gradually increased its positions in stocks and convertible bonds since late October, and increased its positions to a relatively high level after November. In terms of bonds, the portfolio observed an increase in the central bank’s central interest rate level after October, reducing the effective duration of the portfolio from a high level to near the benchmark index. After the change in the epidemic prevention policy in November, the bond position and duration continued to be reduced to a low level .

(2) E Fund returns with peace of mind

In terms of stocks, positions have been increased to near the upper limit, and structural optimization and adjustments have continued. In terms of industry allocation, the portfolio continues to reduce the allocation ratio of the pharmaceutical and photovoltaic industries, and increase positions to benefit from post-epidemic recovery of food and beverages, basic chemicals related to stable growth, banking and other pro-cyclical industries. In terms of convertible bonds, as valuations have fallen, positions have increased. The overall allocation is still dominated by balanced convertible bonds in the market, mainly adding positions to balanced convertible bonds with low absolute prices and low premium rates. In addition, a small allocation of valuation Reasonable new coupon. In terms of bonds, the duration and position level have been reduced. The holdings are mainly high-grade credit bonds and bank capital supplement tools. Pay attention to credit risks, continue to optimize the holdings of individual bonds, and moderately participate in the band operation of interest rate bonds .

(3) ICBC Credit Suisse Shuangli

In terms of asset allocation, the Fund’s bond duration and stock positions have both increased, and the overall leverage has increased slightly. Specifically, with the adjustment of the bond market, especially the sharp increase in the yield of high-grade credit bonds, the Fund increased the allocation of secondary and perpetual bonds of state-owned commercial banks in mid-to-late November to increase the duration. In terms of stocks, the fund increased its positions in late December, and its structure is mainly based on sectors such as national defense and military industry, food and beverage, pharmaceuticals and biology, and power equipment .

(4) Southern Baoyuan Bonds

In terms of equity investment, we continue to maintain the bottom position allocation of consumer goods with long-term stable growth and competitive advanced manufacturing. The overall portfolio is relatively balanced. The large consumer sector has experienced repeated impacts from the epidemic in the past two years. Although there are still uncertainties in the short term, it is believed that the long-term impact of the epidemic will eventually recede, and the stock price also has a good margin of safety. It is worth making a mid-term layout. Due to various reasons, the direction of steady growth has not been exerted, but 2023 is still worth looking forward to, and we have also maintained a certain position. At the same time, the stock prices of some booming sub-sectors in the growth sector also have good investment value after the correction in the fourth quarter. We also select high-quality companies among them for bottom-up layout. In terms of fixed-income investment, the Fund’s bond positions are relatively stable, with the purpose of holding them to obtain stable returns at maturity. The overall rating of credit bonds is relatively high, and the duration and leverage ratio are controlled at an appropriate level .

(5) E Fund Enhanced Return

During the reporting period, the duration and position of the Fund were relatively flexible. The duration and position of the portfolio in the early reporting period were neutral and low. However, the unexpected adjustment and redemption of the bond market still brought large fluctuations to the portfolio. The upward portfolio has gradually increased the duration and positions. In terms of bond allocation, it is still dominated by short-to-medium-term mid-to-high-grade credit bonds; in terms of stock positions, the reserved stock positions are designed to obtain long-term returns exceeding bonds under the premise of withstanding certain fluctuations; In terms of convertible bond positions, the portfolio mainly holds large-cap convertible bonds with better liquidity, and will continue to seek more opportunities in the equity market through methods such as convertible bond conversion and fixed increase .

(6) Xingquan Convertible Bonds

Due to the adjustment of the bond market in the fourth quarter, the overall valuation of convertible bonds has been compressed. With the decline of the overall absolute price, the long-term expected yield of convertible bond assets has increased. In the fourth quarter, the overall position structure of the portfolio was relatively stable .

Earnings in the second and fourth quarters

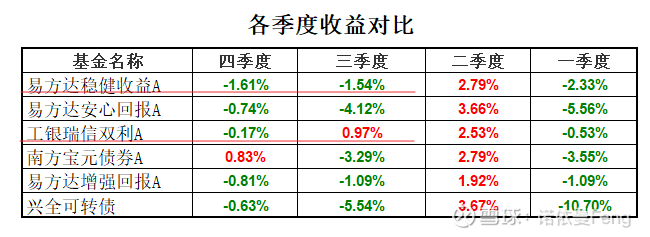

(1) Most of the performance of the funds in the fourth quarter was better than that in the third quarter

4 of the 6 funds performed better than in the third quarter;

ICBC Credit Suisse Shuangli and E Fund’s stable income in the fourth quarter was lower than the third quarter; among them, ICBC Credit Suisse’s Shuangli income turned from positive to negative; E Fund’s stable income did not differ much.

Among the four funds that outperformed, E Fund Anxin Return, Nanfang Baoyuan, and Xingquan Convertible Bonds had higher excess returns than those in the third quarter; among them, Nanfang Baoyuan bonds had positive returns in the fourth quarter.

Even so, we found that regardless of ups and downs, the “range” in the fourth quarter was the smallest, and there were obvious signs of market stabilization.

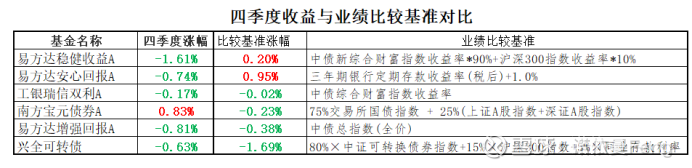

(2) Most of the funds’ income in the fourth quarter fell short of the performance comparison benchmark

The performance comparison benchmarks of the 6 funds are different.

In the fourth quarter, the returns of Nanfang Baoyuan bonds and Xingquan convertible bonds were higher than the performance comparison benchmarks, and the excess returns were both 1.06%. The fourth-quarter returns of the other four funds were not as good as the performance comparison benchmark.

(3) Analysis of the reasons why the performance of the four seasons report did not reach the comparison benchmark

The quarterly report does not disclose financial data and can only be analyzed from the outside.

First of all, due to the wave of redemption of wealth management products triggered by the large-scale sell-off in the bond market that began on November 14, the net redemption of “fixed income +” funds was triggered, which led to an increase in the downward fluctuation of net worth.

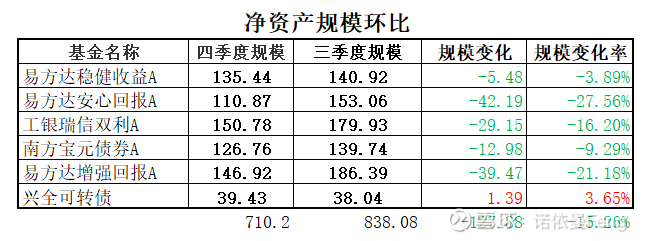

In this paper, the scale of 6 fixed income + funds and 5 secondary debt bases all shrank in the fourth quarter, and only the scale of Xingquan convertible bonds with high equity content increased.

Two famous fixed income + fund players Zhang Qinghua and Wang Xiaochen’s E Fund Anxin Return and E Fund Enhanced Return both experienced a decline of more than 20% in the fourth quarter, 27.56% and 21.18% respectively; star Ouyang Kai’s ICBC Credit Suisse Shuangli suffered a net redemption of 16.20% ; The average quarter-on-quarter decline in the size of the six funds reached 15.26% in the fourth quarter;

A large-scale redemption of the fund in a short period of time will cause the fund to be forced to sell its stocks and bonds, causing the net value of the fund to shrink rapidly in the short term.

Secondly , since the external environment of the equity market has improved significantly since November, and it is believed that it will have a positive impact on the fundamentals of the economy, the adjustment of funds in the fourth quarter has generally increased , which will lead to fluctuations in net worth, especially in When the market continues to pick up, it will affect the growth of net worth;

As Hu Jian, manager of E Fund’s stable income fund, said in the Four Seasons News:

” Overall, in the past quarter, the fund insisted on obtaining long-term competitive investment returns as its goal, and actively adjusted its asset structure. The net value of the portfolio fluctuated to a certain extent , but the overall performance was still relatively stable. “

When the market environment changes, the purpose of actively adjusting positions is to ” obtain long-term competitive investment returns “.

3. The outlook of fund managers for fixed income + funds

Logically speaking, the allocation of equity assets will be increased in the fourth quarter only if one is optimistic about the future equity market.

It is a common view of fund managers to be optimistic about the equity market in the “post-epidemic era”.

Regarding the outlook for the market outlook, Hu Jian, manager of E Fund’s stable income bond fund, has a representative view:

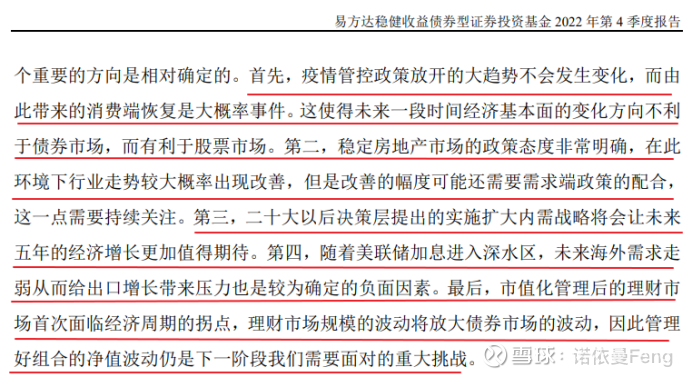

Hu Jian believes that ” changes in economic fundamentals in the future will not be conducive to the bond market, but will be beneficial to the stock market . “

This is not only the main reason why fund managers of secondary debt funds increased their positions in equity assets in the fourth quarter, but also the basis for the market to judge fund portfolio management in the future.

Hu Jian gave five determined directions for the future in the Four Seasons News:

First, the rapid recovery of the consumer side;

Second, the stability of the real estate market;

Third, economic growth in the next five years is worth looking forward to;

Fourth, weak demand in overseas markets has put pressure on export growth;

Fifth, fluctuations in the bond market pose challenges to the management of portfolio net value fluctuations;

(full text)

( Note: 1. The content of this article only represents my point of view. It can only be used for reference. It does not constitute investment advice. It cannot be used as a recommendation or guarantee for buying, selling, or subscribing securities or other financial instruments. 2. Comments are welcome for criticism and discussion. 3. Information and data sources: Wind Financial Terminal; Xueqiu Fund APP; Tiantian Fund Platform)

@雪球创作者中心@今日读论@雪球基金@球友喜欢$ E Fund Repayment Bond A(F110027)$ $Southern Baoyuan Bond(F202101)$ $Xingquan Convertible Bond Hybrid(F340001)$

There are 3 discussions on this topic in Xueqiu, click to view.

Snowball is an investor social network where smart investors are all here.

Click to download Xueqiu mobile client http://xueqiu.com/xz ]]>

This article is transferred from: http://xueqiu.com/3179670287/241241052

This site is only for collection, and the copyright belongs to the original author.