Notice: The next column will share the data on changes in share capital of Tencent every year since its listing, including the number of employee options and restricted shares added over the years, as well as the number of shares repurchased and cancelled over the years, so stay tuned.

Recently, Tencent’s popularity is very high, and many people follow it. The reason is that, as one of the best companies in China, Tencent’s stock price has fallen very much in the past year. With a drop of nearly 64%, the stock price is directly back to June 2017 levels.

Of course, the reason for the plummeting stock price is not the focus of today’s article. Today’s focus is on Tencent’s intrinsic value, that is, how much Tencent is really worth. Although many people think that Tencent is undervalued, most people can’t tell how much Tencent is worth and how much it is undervalued. Therefore, today we mainly use the method of discounted cash flow to quantitatively analyze Tencent’s intrinsic value.

First, we define the intrinsic value of the enterprise: the intrinsic value of the enterprise is equal to the sum of the discounted present value of the net cash flow generated each year during the existence of the company. Why it is the sum of discounted present value instead of the simple sum of cash, here involves a proper term – the concept of “discounted cash flow technique” (Discounted Cash Flow Technique, DCF for short). The definition and calculation method of DCF in textbooks are extremely complicated. I try to popularize the logic of DCF in the most understandable language.

Discounted cash flow simply means that because of the existence of risk-free interest rates (for example, the yield of 30-year US government bonds is 4%), anyone can obtain risk-free asset appreciation by investing in government bonds. For example, if you buy 1 million government bonds this year, next year It becomes 1.04 million, so next year’s 1.04 million is only worth 1 million to you now. 104/(1+4%)=100, this is discounting.

Similarly, for a company, discounted cash flow is the discount of the free cash flow generated in the future to the current value. Take Tencent as an example. If Tencent’s annual free cash flow in the next ten years is 110 billion, then the cash owned by Tencent in 10 years will be 1100*10=1100 billion, but if it is discounted according to the risk-free interest rate to the present, Tencent will have ten The annual cash generated is now only worth 892.2 billion, as shown in the figure below.

Looking at the picture above, it is estimated that many people already understand what DCF means. Indeed, the logic and calculation of DCF is not difficult. The real difficulty is the selection of parameters, that is, the estimation of the future cash flow of the enterprise and the selection of the discount rate. This is the core and difficulty of DCF.

Next, let’s talk about my personal estimate of Tencent’s intrinsic value.

My personal valuation logic is:

1. To estimate Tencent’s future cash flow, first select a relatively conservative cash flow value, use this value to calculate Tencent’s intrinsic value, and see where the lower limit of revenue space is.

2. Be optimistic (but not exaggerated) to estimate Tencent’s future cash flow, give the growth rate in sections, calculate the approximate intrinsic value of Tencent under the condition of growth, and use this as the income space for investing in Tencent upper limit.

3. Compare the lower limit and the upper limit to see if this income range is satisfactory, and use this as the basis for investing in Tencent.

1. Conservatively calculate the intrinsic value of Tencent:

Preferences:

A. Free cash flow: 110 billion, similar to 2021.

B. Growth rate: 0, that is, it will never grow, and it has been maintained at 110 billion per year.

C. Discount rate: 5% (risk-free rate of 4%, plus a 1% risk premium).

D. Duration: Permanent, for the convenience of table display, choose 100 years.

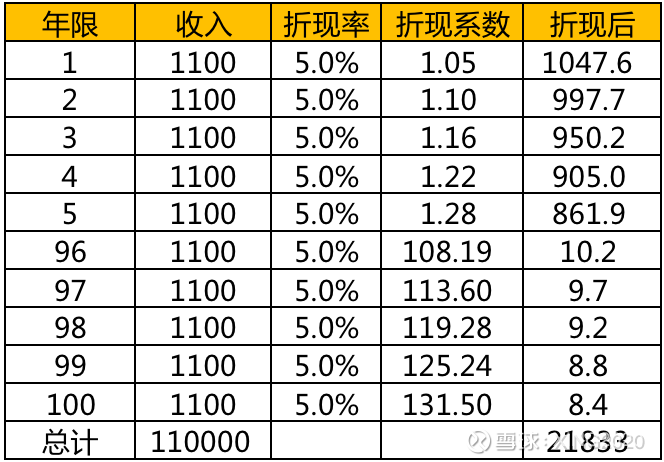

Calculation results: For the convenience of picture display, the data of 90 years from 6 to 95 are hidden

The figure above shows that Tencent’s total cash flow in the next 100 years will be 11.11 trillion yuan, discounted to the current at a 5% discount rate, which is about 2,183.3 billion yuan (sustainable = 1100/5% = 22,000), here is 2,200 billion.

Calculate Tencent’s valuation based on today’s share price:

Share price: HKD 270

Share capital: 9.6 billion

Market value: 270*96=2,592 billion Hong Kong dollars = 2,358.7 billion yuan

Net assets: 736.5 billion yuan

Conclusion: It is conservatively estimated that Tencent’s future cash flow discounted to the present value is 2.2 trillion, plus net assets of 736.5 billion, then Tencent’s intrinsic value is 2,936.5 billion, the current market value of Tencent is 2,358.7 billion, and the intrinsic value is greater than the market value of 577.8 billion. It is equivalent to if you buy the entire Tencent for 1622.2 billion (23587-7365) now, you will earn 577.8 billion immediately. That is, in the most conservative case, Tencent’s profit margin is 5778/(23587-7365)=36%.

In the same way, if you think that Tencent can generate 120 billion cash flow every year in the future, then the sum of the discounted present value of Tencent is 2000 billion (1200/5%), and the intrinsic value of Tencent is 3136.5 billion, which is nearly 2000 more than when it was 110 billion. 100 million. It can be seen that a small change in a value can have a huge impact on the intrinsic value.

Highlights:

A. In many cases, when DCF is used to calculate intrinsic value, the discounted value is the intrinsic value. In theory, net assets cannot be added. Whether to add net assets depends on: 1. If net assets are a non-essential condition for future cash flow generation, the intrinsic value needs to be added to net assets. For example, Tencent is an asset-light company. The realization of future cash flow mainly depends on software and manpower. Even if Tencent distributes all the net assets on the account to shareholders, it will not affect Tencent’s future cash flow generation. 2. If net worth is a necessary condition for future cash flow generation, then intrinsic value cannot be added to net worth. For example, if you spend 1 million to buy a house for rent, and the rent received in the future (permanently) is discounted to the current value of 1.5 million, then the intrinsic value of your house is the discounted cash flow value of 1.5 million, and cannot be added The value of the house (net worth) is 1 million. Because this suite is a necessary condition for generating rent, as long as this suite is always rented, then this suite will always be occupied, and you cannot sell this suite to realize it. If you want to rent it permanently for rent, then the intrinsic value cannot be counted as the value of the house.

B. The risk-free rate of return of treasury bonds is 4%. Why should the discount rate be 5%? This is mainly related to risk issues. The 1% increase is the risk premium. The higher the risk of the investment product, the higher the risk premium rate. The lower the risk, the lower the risk premium rate. rate, the margin of safety will be higher. For example, if you invest in a risk-free product, then the discount rate can be directly used at 4%. For me, Tencent’s moat is deep, and the risk of being disrupted is relatively small, and the value of Tencent’s future free cash flow I set above is conservative, so the corresponding risk premium rate is relatively low. Therefore, the setting of the discount rate is related to the company, and the second is related to one’s own subjective consciousness, and there is no fixed standard.

2. Optimistically calculate the intrinsic value of Tencent:

Preferences:

A. Free cash flow: The base is 110 billion, which is similar to 2021.

B. Growth rate: 10% in 1-10 years, 8% in 11-20 years, 4% in 21-30 years, 1% in 31-100 years.

C. Discount rate: 8% (risk-free rate of 4%, plus a 4% risk premium).

D. Duration: Permanent, for the convenience of table display, choose 100 years.

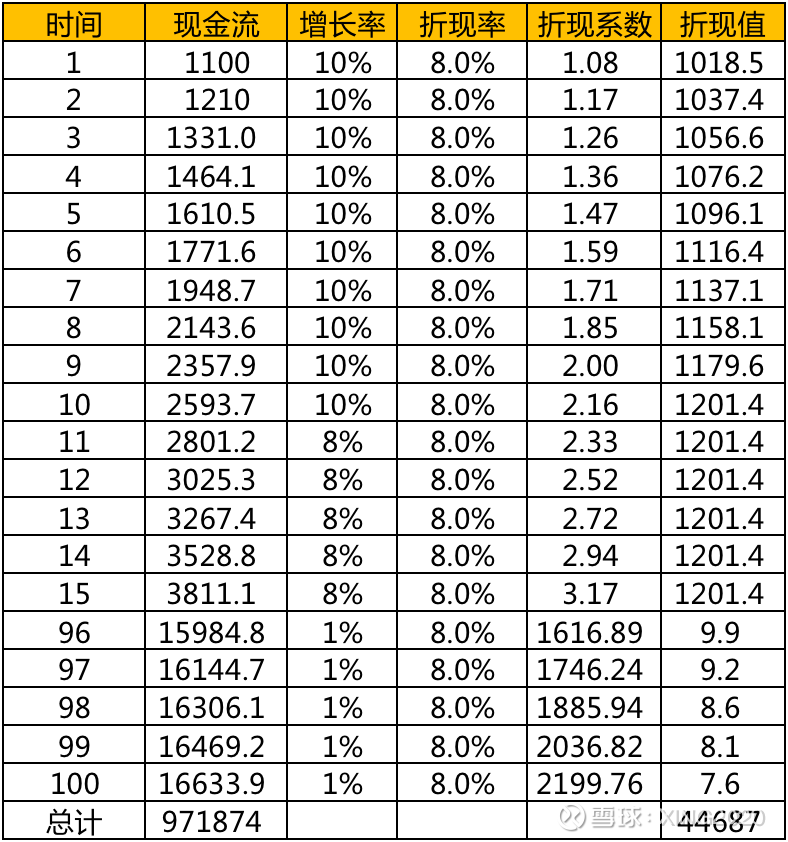

Calculation results: For the convenience of picture display, the data of 90 years from 16 to 95 are hidden.

As can be seen from the above figure, Tencent’s total cash flow in the next 100 years is about 97 trillion, which is about 4,468.7 billion when discounted to the current at an 8% discount rate.

Conclusion: Calculated according to the above segmented growth rate, the present value of Tencent’s cash flow in the next 100 years is 4,468.7 billion, and the net asset is 736.5 billion, Tencent’s intrinsic value is 5,205.2 billion yuan. Tencent’s current market value is 2,358.7 billion yuan, and its intrinsic value is 2.2 times the current market value. In this case, it took 1622.2 billion (23587-7365) to buy the entire Tencent, and the income was 2846.5 billion. That is to say, in an optimistic case, Tencent’s profit margin is 28465/(23587-7365)=175%.

Highlights:

1. DCF is a kind of thinking. The calculated data are gross estimates and cannot be true. In Duan Yongping’s words: Anyway, it must be obvious that it is cheap, and it is the kind of price that will not fall asleep.

2. Duan Yongping said that if you really use DCF to calculate intrinsic value, you should not invest. Munger said he has never seen Buffett count this thing. Well, we are still ordinary people, and we are too far away from the great gods, so it doesn’t matter if we do the math.

3. Some people will say that Tencent will earn 1.6 trillion yuan every year after 100 years. This is too exaggerated. In fact, due to the discounted cash flow, this value is not an exaggeration. After discounting the 1,600 billion yuan in 100 years, it is equivalent to 760 million today. That is to say, it is not much more difficult to earn 1,600 billion yuan in 100 years than it is to earn 760 million yuan now. There is another value for reference: China’s GDP in 1962 was 47.2 billion US dollars, and in 2021, its GDP was 17.73 trillion US dollars, an increase of 375 times in 60 years. The above estimates that Tencent’s annual cash flow will only increase 15 times in 100 years. If Tencent can live for 100 years, and there is no subversion, the probability of 15 times growth is underestimated.

Summary: According to the conservative and optimistic conditions above, Tencent’s intrinsic value is about 2,936.5 billion-5,205.2 billion yuan, and the corresponding stock price is 336-596 Hong Kong dollars. Although the specific value can be calculated through the formula, it should be noted that the greater significance of DCF is qualitative: that is, if the conservative estimate is underestimated, then there is investment value and a margin of safety.

The above is a typical DCF valuation process. In fact, DCF can also be used for valuation from the perspective of opportunity cost. The following is a brief introduction.

Explain the opportunity cost from the perspective of investment: Originally, I could invest 1 million yuan in government bonds and earn 40,000 yuan a year. Now I invest the money in Tencent, resulting in a loss of 40,000 yuan for not being able to invest in government bonds. This 40,000 yuan is me Opportunity cost of investing in Tencent. From this perspective, the discount rate is actually the opportunity cost of investing in stocks.

Everyone’s opportunity cost is different. For the same 1 million yuan, some people can only invest in government bonds and can only earn a 4% rate of return; some invest in industry and can earn a 10% rate of return. So everyone can set the discount rate of DCF according to their own opportunity cost.

Let’s take a look at Tencent’s valuation today:

Share price: 270 Hong Kong dollars; share capital: 9.6 billion; market value: 270*96=2358.7 billion yuan; market value: 2358.7 billion yuan; net assets = 736.5 billion yuan.

Let’s take a look at the conservative estimate of Tencent’s valuation:

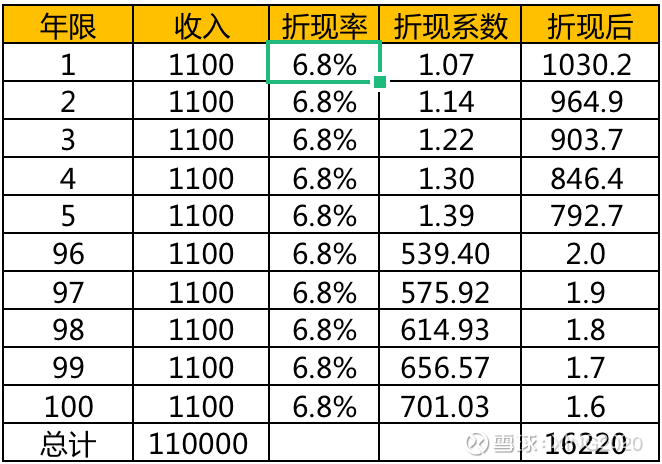

Still based on the annual cash flow of 110 billion, when the discount rate is 6.8%, the sum of the discounted cash flow in the next 100 years is 1,622 billion yuan, and the net asset is 7,365. The intrinsic value is 2,358.5 billion, which is basically equal to the current market value of 23,587. .

Understand the above picture from the perspective of opportunity cost: For example, the opportunity cost of your investment is 6.8% (that is, investing in other products can get 6.8% return), so use 6.8% as the discount rate to value Tencent, and calculate Tencent The intrinsic value of Tencent is equal to Tencent’s current valuation (not overvalued or undervalued). At this time, if you invest in Tencent or invest in other products, the rate of return is actually the same, that is, the rate of return of investing in Tencent at 270 Hong Kong dollars is 6.8% (simple interest). Or understand it this way: you spent 1,622 billion to buy the entire Tencent, and then Tencent can earn you 110 billion in cash every year, then this is similar to a fixed-yield time deposit, and the deposit interest is 1100/16220=6.8%.

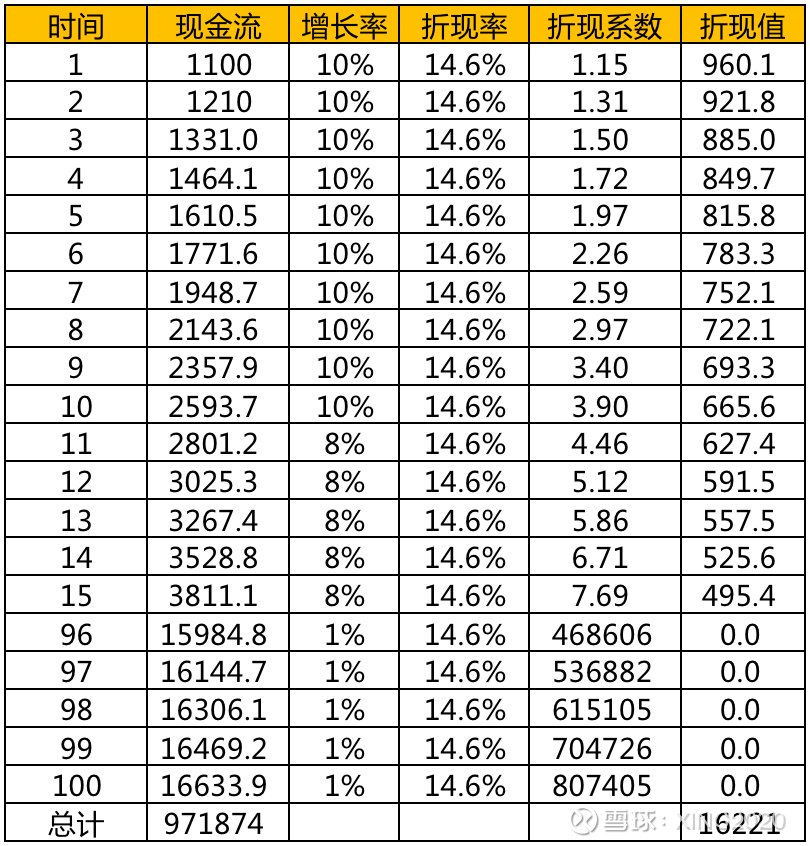

Let’s take a look at the optimistic estimate of Tencent’s valuation:

When the discount rate is 14.6%, the sum of discounted cash flow of Tencent in the next 100 years is 1,622.1 billion yuan, and the net asset is 7,365 yuan, and the intrinsic value is 2,358.5 billion yuan, which is basically equal to the current market value of 23,587 yuan. According to the logic of the above opportunity cost, that is, in an optimistic case, the rate of return of your investment in Tencent at HKD 270 is 14.6% (simple interest).

Summary: According to the conservative and optimistic conditions, Tencent is valued, and from the perspective of opportunity cost, Tencent is bought at the current price of 270 Hong Kong dollars, and the yield is between 6.8% and 14.6%. This is equivalent to giving you a financial product with a guaranteed return of 6.8%, and then the upper limit of return may reach 14.6%. If this wealth management product is a bank’s risk-free wealth management product, then people all over the country should rush to buy this wealth management product, because the guaranteed minimum rate of return is too attractive, and it may be higher. However, because investing in Tencent still has certain risks, it will not happen that people all over the country are rushing to buy Tencent stocks.

Although the guaranteed annual rate of return of 6.8% does not seem to be very high, the risk is relatively small after all. Especially in the past two years, the general environment is not good, the bank’s wealth management income has fallen below 3%, not to mention the stock market, let alone +6.8% in the past two years, very few can achieve -6.8%. Therefore, in the past two years, there is no good way to maintain and increase the value of assets with low risk. In addition, 6.8% is only the most conservative estimate. Tencent has a high probability of developing better than the conservative estimate, so the rate of return may be higher. The risk is not large, there is a guarantee, and there may be additional surprises. The most important thing is to buy Tencent and sleep well regardless of whether it rises or falls. This is the logic of my investment in Tencent.

$Tencent Holdings(00700)$ $Tencent Holdings ADR(TCEHY)$ $Alibaba(BABA)$ @Today’s Topic

There are 93 discussions on this topic in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/6490468241/231993362

This site is for inclusion only, and the copyright belongs to the original author.