Recently, Feng Yunjun shared a lot of content on how to choose quantitative private equity. Among them, it was repeatedly mentioned that when we buy quantitative private equity products, it depends on whether the manager has the ability to create pure alpha (pure excess return). So today Fengyunjun will talk to you in detail about what pure alpha is and why it is important.

$ Zhuo Shi Albert (P001037)$ $ Peng Jin Yongning (P001068)$ $ Peng Jin Jin Shi Chi Yang (P001069)$

First of all, what is Pure alpha?

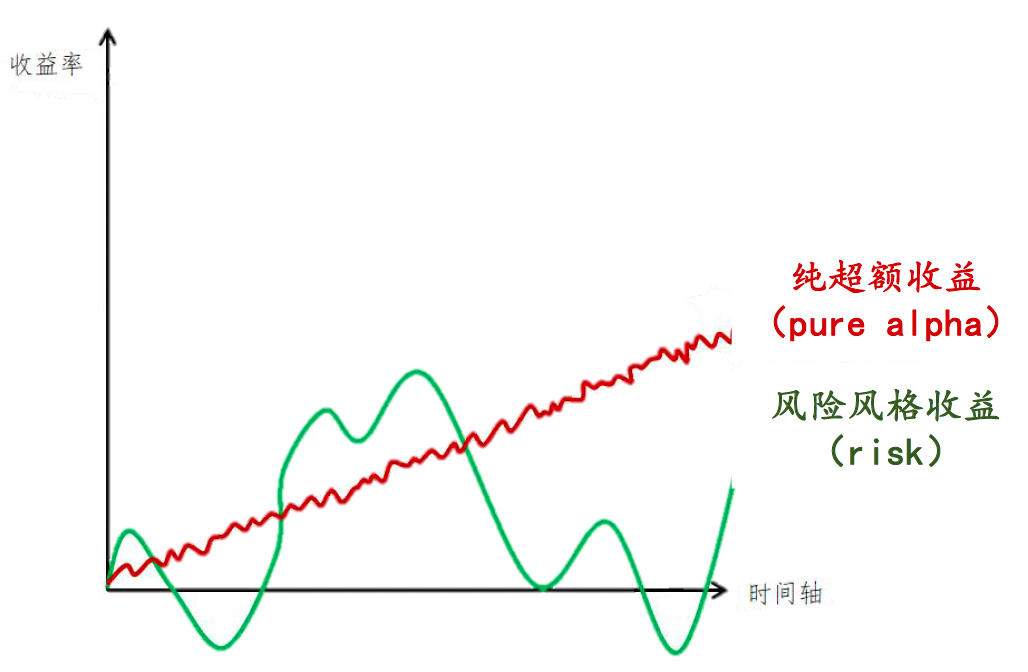

Let’s first review the revenue sources of quantitative index products. The revenue of quantitative index increase includes beta and alpha, where beta is the average revenue brought by the market, and alpha is the excess revenue obtained by the product. The source of alpha here can be simply divided into two parts (not considering offline new releases): pure alpha + risk-style returns. Pure alpha, including volume and price factors, fundamental factors, etc., can bring stable excess returns; risk-style returns are contributed by risk factors, including market factors, industry factors, style factors, etc., and the volatility of returns is very large.

We can feel it through the figure below, the stability of pure alpha and risk-style returns is clear at a glance.

So, why are risk-style returns fluctuating so much, or why do many managers choose too much exposure style? The main reasons are as follows:

1. Risk factor research and development has a low threshold and low difficulty . Major categories of style factors such as momentum, market value, growth, etc. are relatively common indicators. It does not require researchers to research and extract a large amount of information by themselves, and the relationship with the factors in the portfolio is also relatively high. Clear, so the threshold for research and development is low;

2. The risk factor has a large capacity . Like the value style factor, it tends to overweight assets with relatively low value. In fact, it is similar to the traditional pure long style strategy and has a larger capacity;

3. The stage performance is outstanding and the explosive power is strong . It may perform well in the suitable market, but once the market changes, the retracement will be very large. For example, the momentum factor is an obvious risk style. This factor means that if some stocks have risen well in the past few years, they may also rise well in the future. This factor made a lot of money last year, but at the same time it lost a lot of money after last September. The biggest feature of the style factor is that its income is unsustainable, and the experience of holding products that expose too much style is very poor. If you step on the style, the income will skyrocket. Once the market changes, the net value will plummet, which can be described as “ice and fire”. Heavy days.

So, how do we judge whether a manager has the ability to create pure alpha?

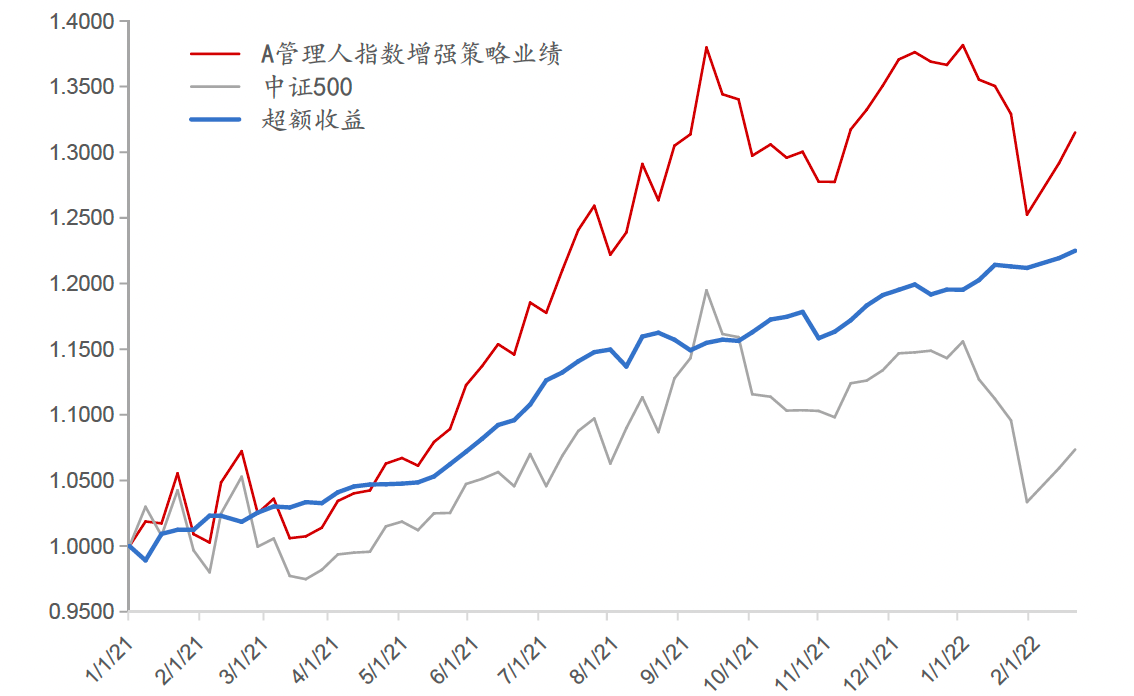

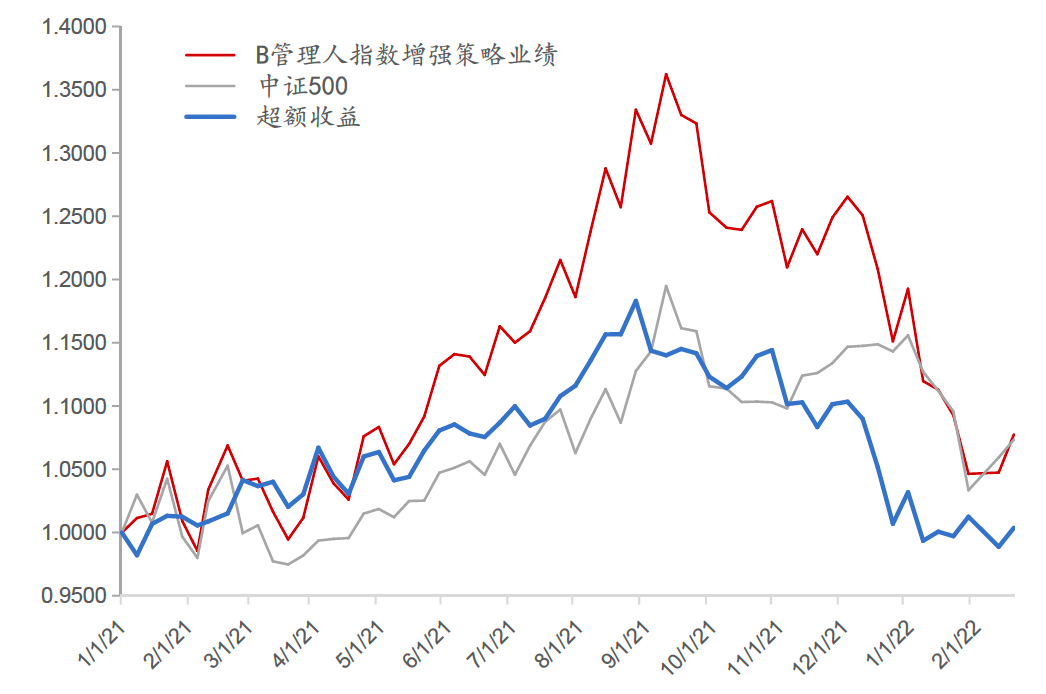

The main thing is to see the stability of the excess, that is to say, when the market is good, it can bring excess, and when the market is bad, it can also create excess . For example, the following figure selects the income of the two managers from January 1, 2021 to January 2, 2022. We can clearly see that the excess return of Manager A is very stable, whether it is Whether the market rose before September last year or the market fell after September, the excess of manager A has risen steadily; on the other hand, the excess return of manager B has fallen with the CSI 500 index since September last year. In this case Next, it is obvious whether to expose the style. If you are unfortunate enough to buy the B product, the income will be like a roller coaster.

true alpha

fake alpha

The main reason why we buy quantitative products is that product returns are relatively certain. Otherwise, it is not much different from buying subjective products. The most important thing to buy quantitative index growth is to hope to obtain a stable excess return relative to the index . Relatively speaking, managers who can provide stable excess returns have the ability to create pure alpha.

How can I choose a product with stable performance?

After dispersing the systemic risk to close to 0 through decentralized positions and strict barra model risk control, the main features of managers who have done a good job of excess stability in the market are: comprehensive coverage of frequency band signals and diversified alpha sources , which can adapt to different market conditions, and at the same time, the strategy iteration speed is relatively fast, and the factor effectiveness and diversity are relatively strong. Although various managers on the market will say that they have full frequency coverage and rich alpha sources, the real reaction is revealed in the performance. For investors, it can be judged by the index of excess return drawdown, such as Zhuoshi, Zhongyang, Si Xie, etc. The excess return in the past two years can be controlled within -3%.

For example, the frequency band signal coverage of Zhuozhi is more comprehensive, covering minutes, hours, days, and weeks, and it can capture the alpha of each frequency band. Therefore, in the first half of this year, when the high frequency did not make money, Zhuozhi played well in the middle and low frequencies. It can also make excess; while Zhongyang’s alpha is mainly based on the core alpha factor of volume and price factors, supplemented by fundamentals and event-driven factors; Si Xie’s alpha sources are also very rich, currently covering intraday trading execution alpha, daily between volume and price alpha, long-term fundamentals and alternative data alpha.

Private placements with strong pure alpha capabilities can bring relatively stable excess returns, and the holding experience is relatively good. But this is not to say that the risk factor is not good, but the over-exposure style will make the product’s return fluctuate greatly, which is more suitable for investors with higher risk appetite, and the quantitative index product is relatively quantitative. The stock selection product still needs to strictly control the risk exposure Investors can choose according to their own needs.

There are 3 discussions on this topic in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/9047540546/228052497

This site is for inclusion only, and the copyright belongs to the original author.