Following the tragic decline of the major A-share mainstream indexes last week, the declines of the major indexes during the year all exceeded -15%. So today, Fengyunjun will briefly talk with you about the most concerned issue of investors: how to deal with the current market? What ideas do you have in the selection of private equity strategies and products?

Question 1: What is the current market environment?

First of all, from the perspective of the current operating characteristics of A-shares, there are still some difficulties: from overseas, the recession in the United States continues, the European energy crisis, and inflation is high, while the inflation turning point and the recession signal in the United States still need to wait; from our internal point of view Although the central bank cut interest rates unexpectedly in August and the economic data in August was slightly better than expected, the uncertainty of external risks caused the wind of funds to be low, the inflection point is unknown, and the market as a whole is in a wait-and-see mood. Therefore, the operating characteristics of the current market are still highly likely to be in the stage of oscillating to find the “bottom”.

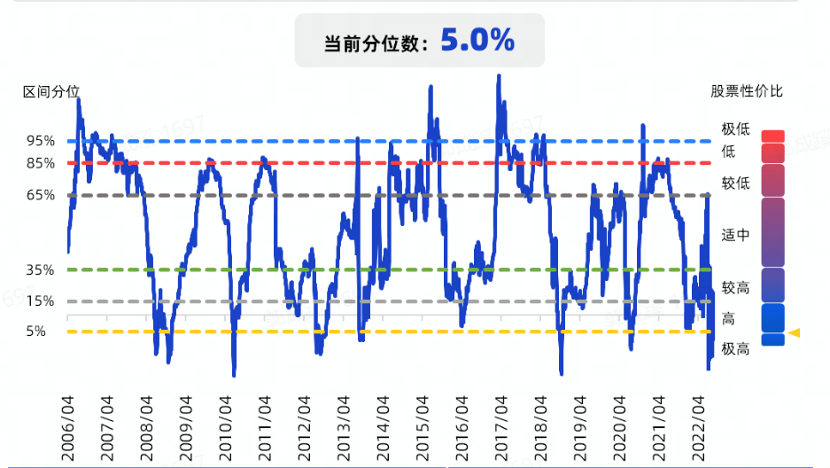

So, has the current position of the index reached a stage of high cost performance? Let’s take a look at the index of the price-performance ratio of stocks and bonds. For example, we can use the reciprocal of the price-earnings ratio of the CSI 300 Index – the yield of ten-year government bonds to measure the current “cost-effectiveness” of the CSI 300 Index. The top of the stock-bond price performance index often corresponds to The bottom of the market, the bottom of the stock-bond price index corresponds to the top of the market. (The inverse of the index price-earnings ratio can be understood as the yield of the index, and the higher the yield of stocks relative to bonds, the greater the probability of future rises)

We can see that the quantile of the current price-performance ratio of stocks and bonds has reached 5%, which belongs to the “extremely high” price-performance stage. At this stage, and the two bottom areas of the market in the past 7 years: January 2019 and January 2016, both the stock and bond price performance indicators and the macroeconomic environment (the Fed raising interest rates, economic recession) have converged. To sum up, perhaps in the short term, the market still needs to go through a process of waiting for a shock and looking for an “inflection point”, but the price-performance ratio has gradually emerged. At this time, we can think about –

Question 2: What ideas can you have in the selection of private equity strategies and products?

1. Quantitative index increase

Index-added products often have significant allocation value in the high cost-effective stage of the index. The two sources of revenue of the index product are β+excess α of the index part, of which the part of α is accumulated for a long time, which can play the dual role of safety pad and accelerator. At present, the excess of the top 500 index increase managers can still be maintained at more than 20%, and the excess of the top 1000 index increase managers can be maintained at more than 25%. We need to pay attention to two core issues: one is to buy in the index. Relative to the “bottom” to obtain better long-term beta returns; the second is to choose managers with excess long-term stability to ensure the sustainability of Alpha.

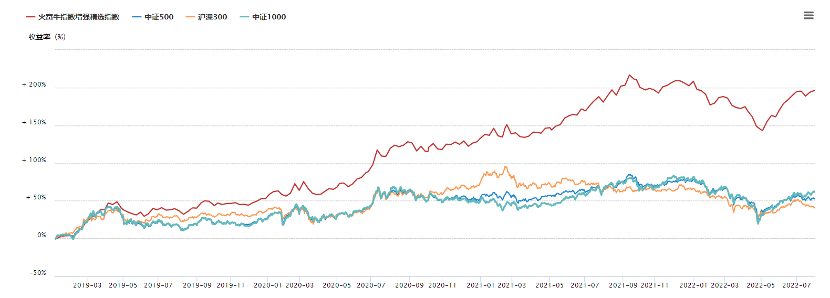

For example, we bought index products in the two bottom areas mentioned above, and the annualized return of buying the Huofu Bull Index Enhanced Select Index in January 2019 was 35%; The annualized return is 24% (this return includes this year’s bear market). The excess is relatively stable, such as Yanfu, Jiaqi, Zhuoshi, Zhongyang and so on.

2. Multi-stock strategy

After the index is adjusted to this position, it is possible that some products with high elasticity and relatively strong performance recovery capabilities begin to have a certain focus value. For example, Zhengyuan, Genxi, Qingli, Gathering, Qinyuan, Conmander and so on. These managers usually have in-depth industry research, are good at exploring high-prosperity industries, and have strong stock selection and trading capabilities. In addition, some managers are good at macro trends, industry rotation, and style switching. Simply put, the price/performance ratio of this part of managers buying after the deep retracement of the broader market is relatively good.

3. Quantitative multi-strategy and low-volatility robust strategies.

Quantitative multi-strategy is to combine different low-correlation strategies to achieve the effect of enhancing the combined returns in different market environments. For example: CTA+ index increase, CTA+ quantitative stock selection, CTA+ neutral/arbitrage, etc. The allocation principle of multi-strategy has two aspects: one is the low correlation between commodities and stocks, which can reduce the volatility of the portfolio in the long run; the other is that the margin trading of CTA will make a large amount of idle funds in the portfolio replaced by stock assets, thereby greatly improving the portfolio. capital utilization rate. Well-known quantitative multi-strategy managers in the market have performed relatively stable this year. For example, Black Wing and Qianxiang have achieved positive returns during the year. Under the current market environment, both the stock market and the commodity market have undergone significant adjustments, and the CTA strategy has also released early risks in the slump from June to August. The margin is relatively high.

Finally, there is the low-volatility robust class strategy . The current allocation significance of this part of the strategy is mainly reflected in obtaining some stable returns in the market adjustment cycle. In addition, the low volatility strategy is of great significance in long-term asset allocation. Such strategies mainly focus on arbitrage, neutral or a mix of quantitative hedging + arbitrage. This part of the strategy has long-term stability and small volatility and drawdown, and also has an irreplaceable role in asset allocation, especially in the bear market. Some managers of arbitrage strategies have run out of low volatility for a long time, but they have not lost or even exceeded the performance of most multi-stock managers. For example, Zhanhong, who specializes in cross-border commodity arbitrage + stock index arbitrage; Shen Yi, who specializes in option arbitrage, Shengquan Hengyuan, who specializes in multi-strategy arbitrage; Xuanling and Newda, which focus on convertible bond arbitrage, etc.

In the current market, which manager are you optimistic about? Welcome players to leave a message and discuss~

$Yanfu Index No.3(P001228)$ $Pengjin Yongning(P001068)$ $Zhengweiye(P001037)$ $Zhengyuan No.1(P000946)$ $Genxi No.1(P000998)$ $Qingli Changxing(P666012 ) )$ $Meet Munger Phase 1(P000984)$ $Commander No.003A Active Management (P001057)$ $Qinyuan Select (P000732)$ $Black Wings Choice Multi-Strategy No.1A(P001044)$ $Qianxiang Excellence 3 No. CSI 500 Index Enhancement A (P001025) $ $ Zhanhong Wenjin No. 1 Phase 10 (P001091) $ $ Shenyi Gewu No. 34 A (P001053) $ $ Xuanling No. A (P001209 ) $ $ Newda Investment Convertible Bonds No. 1(P001177)$

This topic has 0 discussions in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/9047540546/231165386

This site is for inclusion only, and the copyright belongs to the original author.