The share price of Aier Eye has fallen from a high point and has already been cut in half. Even so, the bears think: there is still 70 times the price-earnings ratio, why? Gotta cut again.

So, is Aier ophthalmology expensive at this stage?

It is generally believed that the intrinsic value of the company = the present value of all cash flows created by the company in the future. Then I try to use the discounted cash flow model to roughly estimate the intrinsic value of the current Aier Eye Company.

Taking the end of 2022 as the valuation point, let’s take a look at my valuation model:

1. Expansion mergers and acquisitions are not considered, only the existing hospital assets of listed companies are considered.

2. Net profit in 2022 is 2.8 billion.

3. Assuming the first ten years, from 2023 to the end of 2032, Aier Ophthalmology will still maintain a compound annual growth rate of 15%.

4. Enter 5% sustainable growth from 2033. The discount rate is 8%.

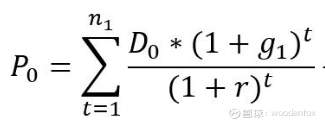

Now that the conditions are clear, we can use the two-stage DCF valuation formula to calculate:

The first stage: the medium-speed growth period in the first ten years

We put D. = 2.8 billion, the compound growth rate of the first stage g1=0.15, the discount rate r=0.08, n1=10 is substituted into the formula, and the discounted value P of the first stage is obtained. = 40.198 billion.

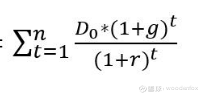

second stage:

Explain, D here. It is the net profit at the end of 2033 in the eleventh year. then D. =2.8 billion×1.15∧10×1.05=11.894 billion.

We substitute the perpetual growth rate g=0.05, the discount rate r=0.08, and t approaching infinity into the simplified formula D. /rg=396.467 billion.

Discounting this value to the end of 2022, 3964.67/1.08∧10=183.641 billion. That is, the present value of the second stage of sustainable growth is 183.641 billion.

The addition of the two stages yields a company valuation of 40.198 billion + 183.641 billion = 223.839 billion.

According to the closing price of 27.49 yuan on Friday, the total market value of Aier Ophthalmology is 197.28 billion yuan. According to the rough calculation of my valuation model, the intrinsic value of Aier Ophthalmology is 223.839 billion yuan. Compared with this, the current price of Aier still has a discount of about 12% to the intrinsic value.

Now, let’s confirm whether my model is reasonable.

First, the value I calculated above is the enterprise value. To calculate the equity value, subtract the company’s liabilities for 2022. At present, the company’s additional issuance has just been completed, and there is a large amount of cash on hand. I checked it, and the company’s liabilities and cash are basically the same, so the value calculated above is basically equal to the company’s equity value.

Second, although, the company’s free cash flow is not the same as net profit, because if there are capital expenditures in the future, net profit must deduct capital expenditures to approximate free cash flow. But my model takes this factor into account, because my assumption is the situation of existing hospitals, not involving mergers and acquisitions or capital expenditures for new hospitals.

Third, I refer to some research reports on the size of the ophthalmology market. Some reports believe that in the next ten years, with the aging of the society and the younger age and high incidence of myopia, the size of the ophthalmology medical market will remain around 13-15% of the overall speed up. In the entire fiscal year since Aier Ophthalmology was listed 12 years ago, the compound growth rate has been maintained at around 30%. I feel that the growth rate of 15% in the next 10 years is not outrageous. Although some people may question that the 30% growth rate has contributed to the extension of mergers and acquisitions, I have sorted out the 6 mature hospitals that rank in the top since the listing of Aier Ophthalmology. The adverse effects of shunting patients, they still maintained a 12-year endogenous CAGR of 16.98%. (For details, please refer to my work “Poke the Fog of Growth and Reveal the Truth of AIER Ophthalmology’s Endogenous Growth!”) Therefore, I think it is appropriate to take 15% as the expected compound growth rate of AIER in the next ten years.

As for the discount rate of 8% and the sustainable growth rate of 5%, there is no exact number. My numbers may be slightly optimistic, but not outrageous. Fortunately, the valuation itself cannot be an exact value, but the holder needs to have a basic judgment on the company he holds. With this judgment, investors will not be confused about the value of the company and arbitrarily make a decision to buy or sell the company.

There is one last question. This article does not take the capital expenditure factor into account. However, Aier Eye will inevitably conduct mergers and acquisitions of in vitro eye hospitals in the future. How to judge this static valuation and future dynamic Aier? Very simple, we just need to consider clearly, can the value of the hospital acquired in the future cover the cost of acquisition or even increase the value of the company?

Let me give an extreme example. In 2017, Aier acquired 75% of the equity of Dongguan Aier with nearly 100 million yuan. In 2021, the net profit of the 75% equity of Dongguan Aier was 46 million. We assume that after 2021, Dongguan Aier will enter a sustainable growth rate of 1% with a discount rate of 10%. Using the DCF valuation model, it is calculated that Dongguan Aier will be worth 516 million in 2021. It can be seen from this example that Aier’s capital expenditure is a chicken that can lay golden eggs, which is different from some ordinary enterprises that need to continuously invest capital and upgrade production materials in order to maintain their original market position and competitiveness. .

It may be that the dynamic Aier looks complicated and difficult to analyze, so I have hardly seen any articles that use the DCF model to analyze the intrinsic value of Aier ophthalmology. I tried to simplify the model and write it in this article, hoping to get some feedback from the majority of golfers.

@Today’s topic @snowball creator center @aierinvestor relations @bright avenue666 @anshun

$AIER Ophthalmology(SZ300015)$

This topic has 16 discussions in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/3651332251/234613297

This site is for inclusion only, and the copyright belongs to the original author.