The production capacity of various links in the photovoltaic industry is rapidly expanding, and the importance of differentiated layout of enterprises in the industry is highlighted. Last year, LONGi launched a high-profile P-type new battery HPBC based on gallium wafers. It started with 29GW, mainly for the distributed market. It is expected that LONGi will launch a new battery for ground-based power stations soon, most likely based on gallium-based P-HJT or P-TOPCON, and the starting point should not be lower than 40GW.

The gallium sheet is not mysterious. It is the same as the phosphorus-doped N-type sheet, and its purpose is to avoid the attenuation caused by boron-oxygen recombination. Silicon wafer companies in the industry have more or less conducted research on gallium wafers, but why is it that only one company, Longji, currently uses gallium wafers, while others are taking the N-type route? Perhaps the scarcity of gallium is a consideration.

1. Gallium reserves

The general data is about 300,000 tons, and some data is 1 million tons.

This figure shows that the reserves of gallium are very small and absolutely scarce. But even if it is 300,000 tons, compared to the current consumption of hundreds of tons, it is enough!

2. Output

Gallium compounds are associated with other metal ores, and the content is extremely low. They are scattered resources and are mainly by-products in the aluminum smelting process. Therefore, the relationship between gallium output and demand is relatively small, but it is more related to the demand for industrial metals; for the same reason, its price can fall to a low level that does not match its scarcity.

Gallium recycling has increased rapidly in recent years, accounting for almost half of production.

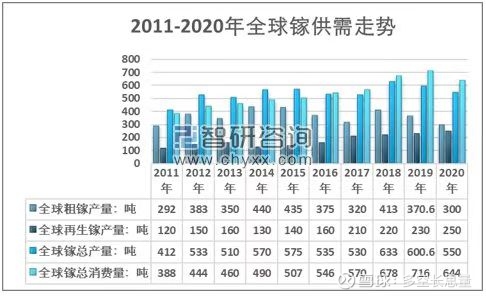

The output and demand of gallium are shown in the table below

1. In the table, since 2015, the production of crude gallium has decreased rapidly, which is due to the substantial shutdown of crude gallium production capacity in countries other than China. At present, crude gallium is basically produced by Chinese manufacturers.

2. From 2011 to 2015, the supply of gallium has always been in excess of demand. Since 2016, the relationship between production and demand of gallium has reversed.

3. In 2018 and 2019, the demand for gallium has grown rapidly, which is due to the surge in demand brought about by LED replacement of incandescent lamps.

4. From 2011 to 2015, 311 tons were accumulated, and from 2016 to 2020, 306 tons were destocked. If consumption continues to exceed production, gallium will usher in a price increase cycle after destocking.

3. Purpose

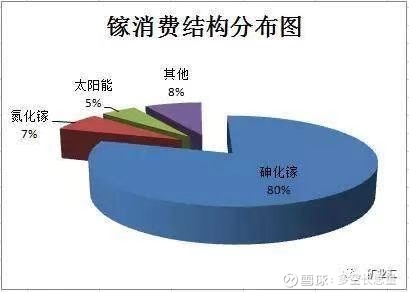

The following table shows the use of gallium in the world in 2017

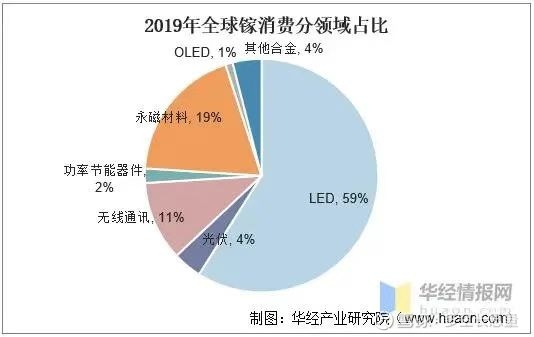

The figure below shows the application by field in 2019

It can be seen that gallium is mainly used in semiconductor materials, mainly in LED, new energy magnetic materials, and communications. These aspects are sure growth, so the consumption growth of gallium will continue.

4. The Chinese market represents the supply and demand of gallium

Bauxite smelting determines that crude gallium production is mainly provided by China.

Gallium is a rare metal, and all major countries have carried out strategic reserves. Due to the huge advantages of China’s primary manufacturing industry, the supply and demand relationship of gallium is basically reflected in the Chinese market. Especially due to the rapid expansion of China’s LED industry, China has replaced Japan as the largest gallium consumer since 2018.

5. Gallium will soon be in short supply

Crude gallium production is closely related to bauxite smelting. Due to the overproduction of primary aluminum for many years, the overlapping of some national resource barriers and the continuous decline in the grade of gallium in China’s bauxite, although the nominal production capacity of crude gallium is abundant, it is difficult to increase the actual production in a large amount.

It is expected that China’s economy will start to bottom out in 2023, and the demand for gallium will grow rapidly: LED lighting, Mini LED, Micro LED, LED applications for new energy vehicles; demand for communication radio frequency devices; demand for power devices; demand for magnetic materials brought by new energy vehicles.

This supply and demand logic is consistent with the conclusion of the previous global gallium supply and demand trend chart analysis: if consumption continues to exceed production, gallium will usher in a price increase cycle after destocking.

6. Consumption of gallium by LONGi gallium chips

The amount of gallium-doped gallium sheet: 40Kg silicon material doped with gallium 1g calculation.

LONGi’s 30GW HPBC needs about 2 tons of refined gallium per year, and if it is a 70GW gallium chip, it needs about 4.5 tons of refined gallium. It is estimated that the global module demand will be 600GW in 2025, LONGi’s target market share will be 20%, which is 120GW, and silicon wafers will be 150GW, which requires about 10 tons of refined gallium.

5. Is the gallium price increase cycle coming early?

For industrial metals, 10 tons is not enough, but for gallium, whose current output is only 600-700 tons, it is a large amount. The increase brought by one company is about 2% of the global output!

The rapid increase in the volume of gallium chips will push the shortage of gallium ahead of schedule.

6. The choice of gallium-doped and phosphorus-doped

At present, the price of refined gallium is about 2000-3000 yuan/Kg, and the cost of doping gallium can be ignored. But after the imbalance between supply and demand and the end of destocking, who can know the price?

When a certain resource is in short supply, the price will inevitably skyrocket. Due to the rapid development of new energy sources, the price of silicon materials has soared, and the price of lithium salts can rise tenfold in two years. The scarcity of silicon and lithium is difficult to compare with that of gallium. If the price of gallium reaches 150 yuan/g, the cost of gallium doped with silicon wafers will be close to the order of 0.01 yuan/w, which is no longer negligible.

According to LONGi’s official data, the company’s laboratory battery records are: P-HJT, 26.56%; HJT, 26.81%. 26.81% of the records did not specify the type of silicon wafer, and it was presumed to be N-type (if not, please notify the revision).

In 2021, LONGi announced that the research and development of single-crystal double-sided N-type TOPCon cells by LONGi’s battery R&D center achieved a conversion efficiency as high as 25.21%; the efficiency of single-crystal double-sided P-type TOPCon cells took the lead in the industry to break through 25%, achieving a world record of 25.02%.

It can be seen that in terms of conversion efficiency, LONGi’s gallium chips are still about 10% lower than N-type .

Cost reduction and efficiency increase are the constant pursuit of the photovoltaic industry. At present, there is still a gap between gallium wafers and N-type in conversion efficiency. It remains to be seen whether the cost increase caused by the scarcity of gallium and the future shortage of gallium supply will become a barrier to LONGi’s differentiation.

$LONGi Green Energy(SH601012)$ $TCL Central(SZ002129)$ $Chinalco(SH601600)$

There are 37 discussions on this topic in Xueqiu, click to view.

Snowball is an investor social network where smart investors are all here.

Click to download Xueqiu mobile client http://xueqiu.com/xz ]]>

This article is transferred from: http://xueqiu.com/2236698394/240673344

This site is only for collection, and the copyright belongs to the original author.