The inspiration came from looking at Li Bei’s speech at the 2014 Golden Bull Award Moment and a simple discussion with a self-operated FOF friend of global investment. Today, I will share with you the macro strategies that you don’t know. The straight-to-the-point conclusion is that managers who have done better in private equity macro strategies currently have a high proportion of underweight stocks, and their views are basically synchronized.

First, what is private equity macro strategy, and who is doing it?

Macro strategies are actually divided into two categories. The old school is represented by Soros’ Quantum Fund, also called active macro, and the new school is represented by Bridgewater Fund’s flagship all-weather product, also called passive macro.

The former is based on the extraordinary sense of smell of fund managers, betting between different investment varieties, seldom paying attention to the trend of a single bond, and often betting on the entire asset package. In the movie Big Short, a very detailed process has been imaged and reproduced. John Paulson’s moment when he bet on the subprime mortgage crisis.

The latter is based on “systematic” financial engineering and low correlation, striving to achieve a balanced configuration effect between different asset packages, so as to adapt to changes.

Subject to the shortage of domestic derivatives and the inability to trade key foreign exchange and other asset packages, in fact, domestic macro strategies are not the same as international mainstream funds, and it is very difficult to achieve the perfect operation of macro strategies in China, especially is 24/7.

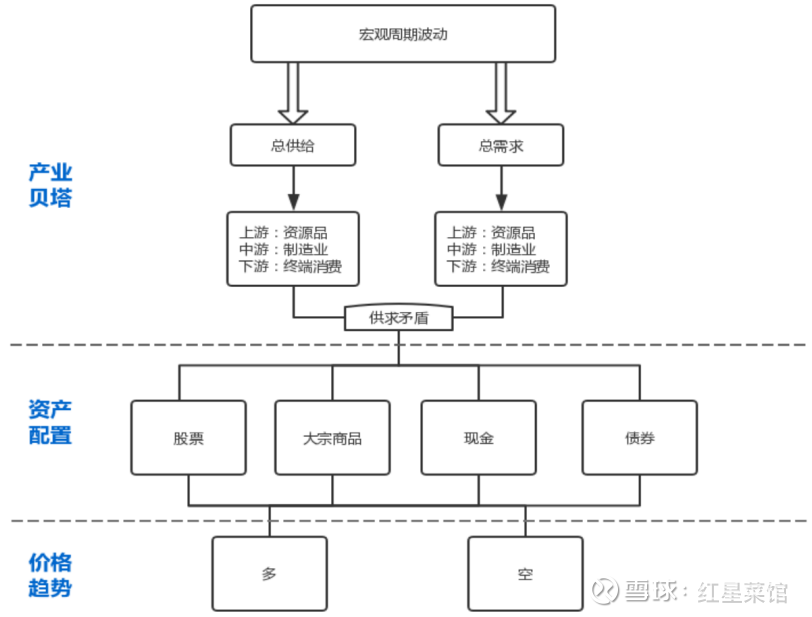

Therefore, our domestic macro strategy has basically formed the following strategy structure:

(Source: Tempo Academy)

The above picture is well organized, and there are three extensions in actual combat:

1) The variable research of consumption and demand in the research of industrial beta is relatively cumbersome, it is difficult to understand the real variables, and it is often too late to pass it on. This leads to the main research on changes in supply, involving stocks and liquidity+ Valuation is the main concern, and when it comes to commodities, that is, whether there is a shortage of upstream material supply, and the scope is relatively narrow, often making fund managers go around in the alley;

2) The asset allocation of cash and bonds is of little value to many managers. Treasury bond futures may be used. Except for managers from bonds such as Lerui, they really lack energy to dig deep into bonds. Therefore, it is still stocks + commodities, and the selection of companies in stocks is not deep enough, so you can only bet on styles, such as certain types of stocks. Typically, Banxia was overweight CSI 500 before, but the breadth of instrumental ETFs currently issued by public offerings is not enough. , the managers are extremely constrained, and in the end, many people have made CTAs again and again;

3) At present, domestic managers have simple hedging methods and insufficient hedging ideas, resulting in frequent betting in one direction.

In conclusion, narrow direction, few tools and single direction are the major drawbacks of domestic macro strategy.

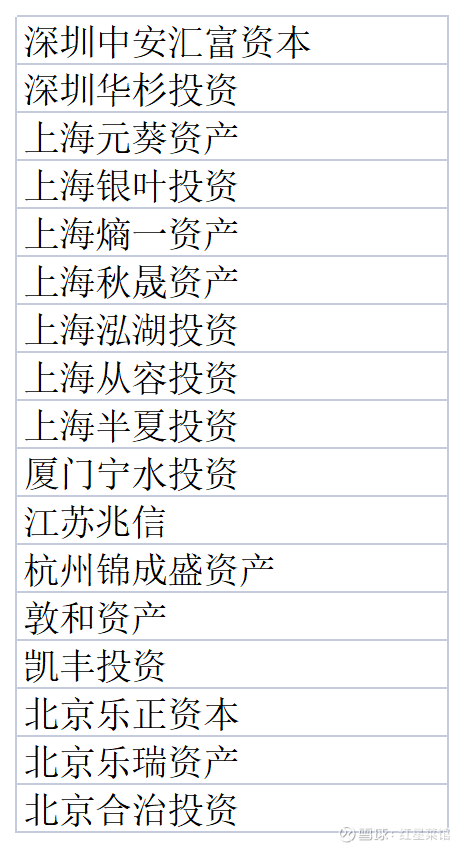

Under these drawbacks, there are very few managers in China who are really doing macro strategies. According to the classification of Huo Fu Niu, there are 96 managers, but if the small and micro managers with less than 500 million are cut off, and some managers are deleted that are no longer public According to the statistics of Red Star Restaurant, there are only 17 managers who issue macro products. They are:

(Source Huo Fu Niu, in alphabetical order)

Among them, there are tens of billions of super managers, as well as managers with a scale of just over 500 million. Compared with the huge selection of stock longs, it seems very weak, but fortunately, we can make some very interesting statistics.

Second, what is the historical effect of macro strategy?

Now that all the important samples have been selected, let’s look at these seventeen private equity managers.

1) Who is good and who is bad for key indicators;

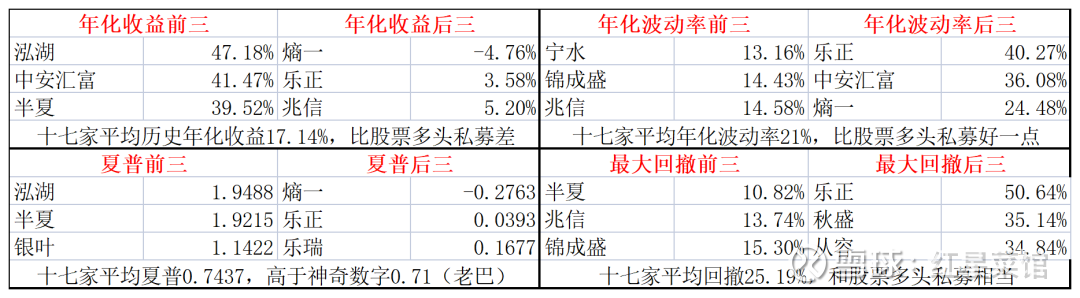

The simplest indicator perspective is the presentation of the effect statement of the past strategy, which does not represent the future, but can be eliminated:

(Data source: Huo Fu Niu)

A) The matching degree of returns and risks is not high, and the internal good and bad are mixed;

Among the macro strategies of 17 private equity firms with a scale of more than 500 million, some, like Jin Chengsheng, show the characteristics of low volatility, low drawdown and low returns, and are consistent; some, like Lezheng, show high volatility, high drawdown and low returns The characteristics are exaggerated; some are like Pinellia, with excellent data; some are like Zhongan Huifu, which trades higher volatility for higher yields; some are like Honghu, which is very high Sharp runs out of high yields….

The complex composition of macro strategies is vividly reflected in these data. Except for Pinellia, which is leading in all directions, it is difficult to see historical net worth with low risk and high returns. Then the question is, is Pinellia currently in super status? Can it continue?

In general, private equity macro strategies show a mismatch between returns and risks. Except for the best top managers, they are not very ideal.

B) The data is approaching the stock bulls, and there is no obvious advantage or disadvantage;

In the macro strategy of private equity of 17 companies with a scale of more than 500 million, the average result is similar to that of long-share private equity, and the return is worse, but the net value is also more stable, thus creating a better Sharp.

However, the degree of Sharpe is limited. The magical data in the table, 0.71, is the Sharpe ratio of Buffett’s ultra-long-term performance. The longer the time, the bigger the scale. Excellent fund products will continue to approach this value. Tianhui and other public offering star fund products are basically around 0.67.

At the same time, only 9 Sharps were higher than 0.71, accounting for 52%, about half. That is to say: although the timing and asset selection of the private equity macro strategy group have played a better investment effect, this conclusion is only limited to the top few Managers, they push up the industry average.

C) The average longest time without a new high is 394 days;

This means that in history, buying these 17 companies with a scale of more than 500 million private equity macro strategies, in the worst case, can lose money for one year.

This data is much better than private equity bulls.

2) Exponential curve situation;

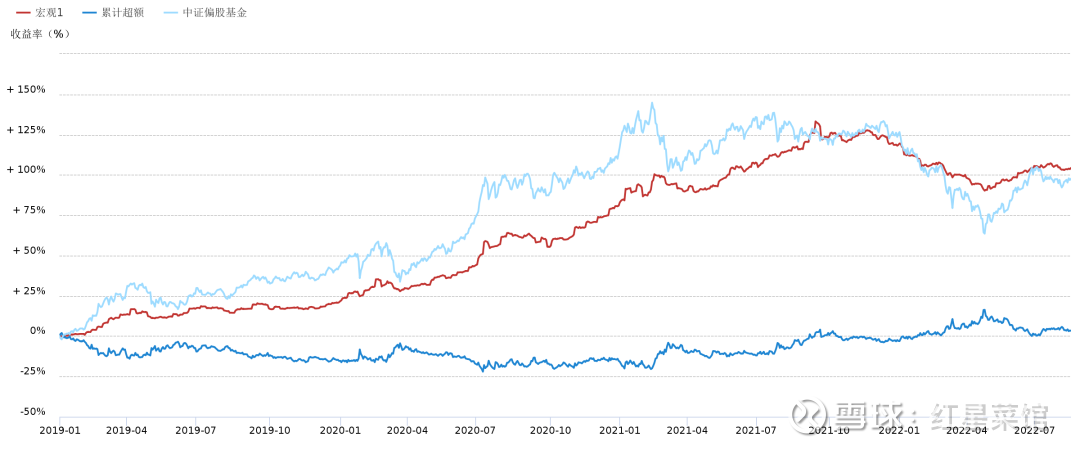

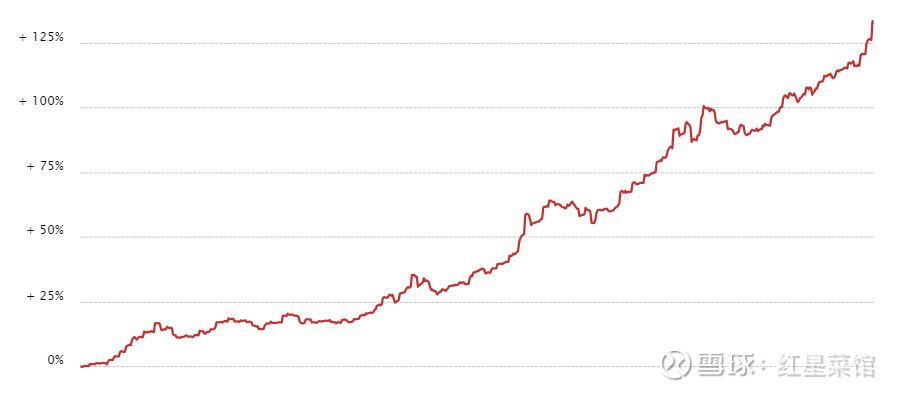

To observe the situation of a group, a very important thing is to draw an exponential curve. When I make a combination of these 17,500 million or more private equity macro strategies according to the evenly distributed amount, his historical performance is clear at a glance :

(Source of back-test data: Huo Fu Niu, red is the macro strategy index of 17 private equity firms with a scale of more than 500 million)

There are a few key points in this comparison chart that need to be dismantled, and there are certain surprises:

A) Before September 2021, the combination of seventeen macro strategies reached a Sharpe of 3.31 (twice the partial stock in the same period). This Sharpe value lasted for nearly two years, which has already increased the factor of managers’ backtesting than many quantitative indexes. The returns are sharply higher, which is a very terrifying effect; at the same time, the maximum drawdown in this range is only 5.6%, while the partial stock fund is 17.42% in the same period. I released the combined net value of this time period, which makes people very refreshing….

B) After September 2021, the combination of the seventeen macro strategies did not continue to be strong, nor did they get rid of the decline in the stock market, contributing to negative returns, but it was precisely at this time that the excess of the comparative equity fund was manifested. In April After rebounding, it fell again. The reason is very simple. The macro strategy takes less time to fill up stocks, and the long-term return is of course lower than that of partial stock funds.

It is expected that the above two phenomena will continue. The macro strategy group contributes very well to Sharp, but it fails to outperform stocks every few years, and the accumulated yield gap will be relatively large.

C) High monthly win rate:

Of the 43 calendar months, 83.7% had positive returns.

In fact, among the seventeen managers, very few managers have achieved a monthly win rate of 83.7%. Why is the index effect so good when they are combined?

3. Low correlation between macro strategies

As mentioned earlier, the macro strategy involves many different points of judgment, and it is based on very vague macro data, and there are many changes, so it is difficult for everyone to make the same decisions, which shows a very good low in the net value of funds. Related Features:

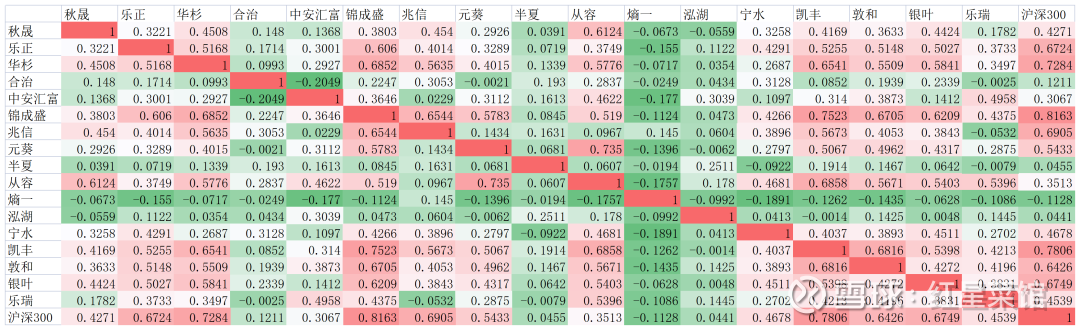

(Data source: manual statistics of Red Star Restaurant, the picture is relatively large, double-click to open)

How to reflect the low correlation between strategies?

1) Some are closely related to CSI 300 (17% higher than 0.7 ratio), and some are not closely related to CSI 300 (29% or less), the numerical gap between the head and tail is very large;

2) The average correlation between the seventeen managers is 0.31, the same as above, the relationship is not close.

Among them, the three managers who have little relationship with the stock market and everyone, but have high performance effects, I call them the Royal Three, represent the current benchmarking level of domestic private equity macro strategies: Zhongan Huifu, Honghu, Pinellia. If the degree of connection between stocks is not considered, Kaifeng Plus is four, which is more representative.

Pull away, say it back. The reason why the combination of seventeen private equity macro strategies can far exceed the effect of a single one is that they form a better combination because of their low correlation with each other. This is the role of fund portfolios and indexation.

4. Their current convergent views

After talking about the differences between private equity macro strategies, I will talk about a feature discovered in the past two days.

They are gradually contributing to a convergent view: underweight stocks.

One of the most conspicuous data is that the average correlation with the CSI 300 has dropped from 40% a year ago to 20% in the most recent month, which can be simply understood as the average stock allocation ratio of 17 private equity macro strategies halved.

But the details differ:

1) The biggest changes in position adjustment are (in order):

Kaifeng, Zhongan Huifu, Dunhe, from the perspective of net worth, they may have almost no stock positions at present;

2) The smallest changes in position adjustment are (in order):

Pinellia, Yuankui, Ningshui, in terms of net worth, they may not have changed much at present;

3) Among them, there are relatively large stock increase actions (in order):

Honghu, Yinye, Zhaoxin, from the perspective of net worth, they may be adding positions silently at present.

But the overall stock reduction is actually happening.

I have collected the full text of Dun and Xu Xiaoqing’s outlook for the second half of the year. The fund products he manages are obviously reducing their positions in stocks. His original words are representative:

“The possibility of a bull market (such as 2019) is also relatively small, because now domestic and foreign demand cannot form a resonance…. The upward and downward elasticity of the entire stock market is not sufficient…. Both the interest rate hike cycle and the balance sheet contraction cycle are It’s not over yet, so we still have to be cautious in general… In a state of stagflation, it is difficult for stocks and bonds to gain positive returns, and only commodities perform relatively well… How did commodities and stocks perform during the stagflation period in the 1970s? Equities have been weak, all commodities have outperformed equities, with crude oil being the best performer, followed by gold, copper, soybeans.”

This may be the average perception that the seventeen private equity macro strategies are gradually forming from their positions, and it is the average decision-making currently being made by this group of managers whose main job is to select timing and assets.

Five, are their average decisions correct? Want to follow?

Their timing has historically produced better investment outcomes on average, but only for a few managers whose average decisions have following value.

But here involves the choice of active macro and passive macro.

I use the chatting process I mentioned with my friends at the beginning of this article to comment:

“The uncertainty of the current situation is very obvious. Choosing to reduce the allocation of stocks will definitely reduce the probability of extreme risks and make your asset portfolio more stable; but I am a passive macro school, and I know the event will pass, and it will involve me. It’s a second timing issue to buy it back, after all, stocks are cheap now. You’re not wrong, and I’m not going to be wrong either.”

This is my opinion and attitude. The current average choice of this batch of macro strategies is correct, and their future risks will be reduced; the choice of the stock long strategy with high positions now is also correct, and their future returns will be higher.

It depends on what you really want in your investment.

@ @ Fund Fengyunlu @ @Today’s topic

There are 8 discussions on this topic in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/8915001532/228785304

This site is for inclusion only, and the copyright belongs to the original author.