The market has been bad recently. I only talk about logic and don’t chase hot spots. Falling down is actually a good layout opportunity.

——————-

In this issue, we will talk about the opportunities brought by the European energy crisis. Many industry sectors are not in high positions, and there will be many opportunities in the future.

The causes of the energy crisis

In fact, everyone understands the big logic. Let’s quantify it in detail here, which is more intuitive.

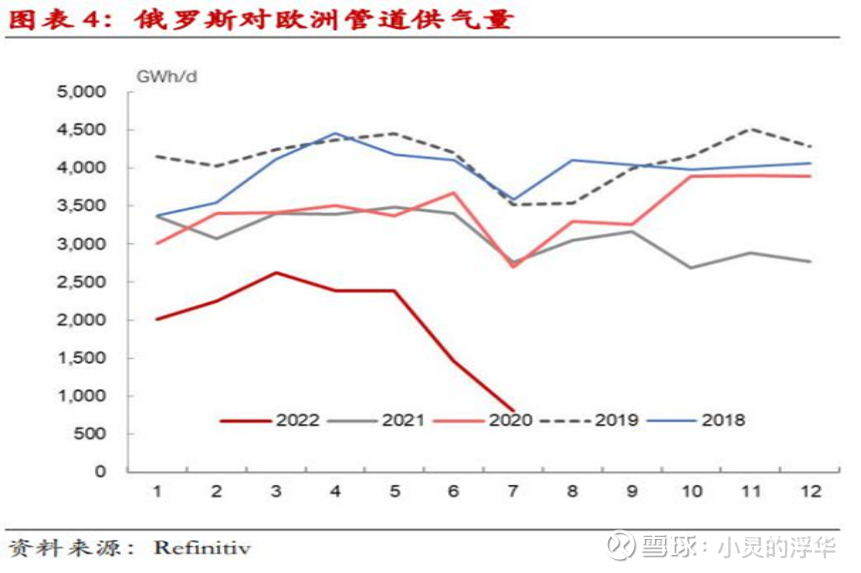

European countries have taken too big steps towards clean energy, and traditional energy has been withdrawn too early, so they are very dependent on Russia. As Europe’s largest energy supplier, Russia will provide 40% of Europe’s natural gas in 2021, 10% of which will be used for power generation, 10% for heating, and 40% for industrial production.

After the Russia-Ukraine incident, Russia’s pipeline gas supply to Europe dropped sharply to 20% of the previous level, and it was announced that it would stop gas just last week.

We all know that the winter in Europe is very cold and long. In order to avoid humanitarian disasters, there must be priority for civilian use. The most direct and effective way is to cut off some industrial gas and ensure civilian use as much as possible.

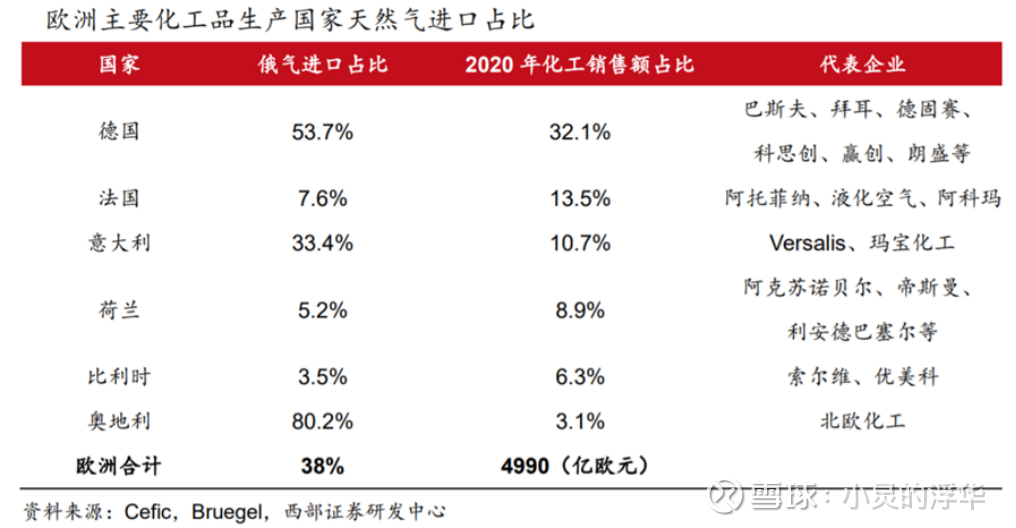

The chemical industry in Europe is very dependent on natural gas, and energy accounts for more than one-third. Now that the price of natural gas in Europe has exploded, the production cost of chemical companies has increased significantly. When the temperature drops in Q4, the problem of natural gas shortage will be further exposed. At that time, many companies will stop production, whether it is due to profit considerations or government pressure, the probability is quite high .

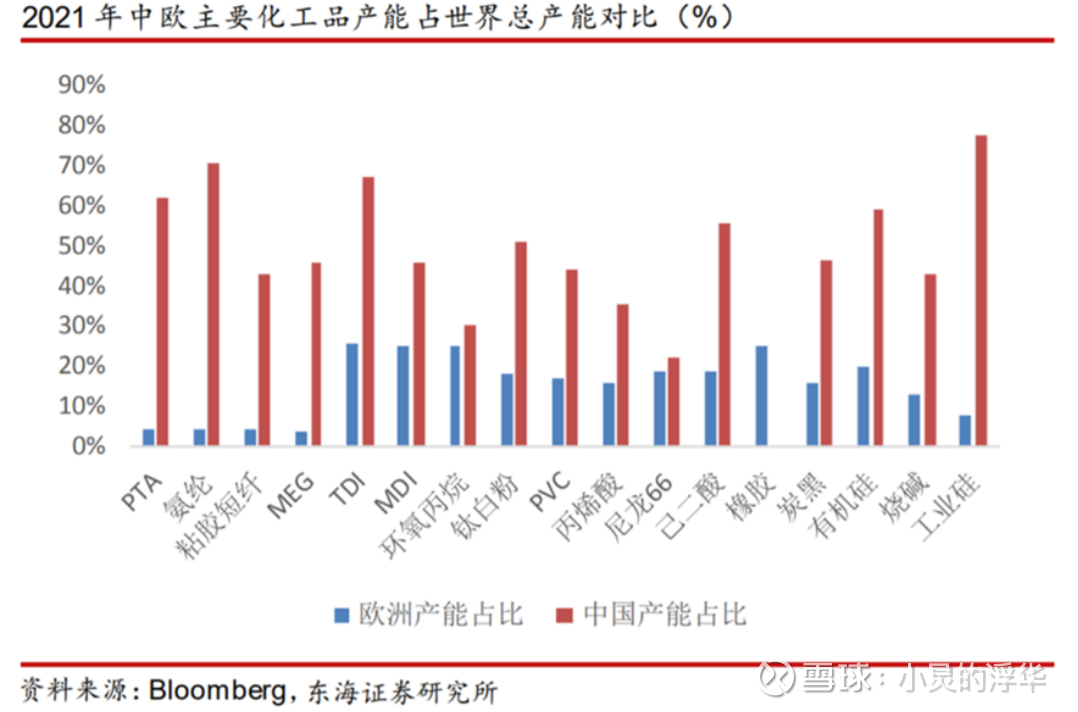

2. Comparison of chemical production capacity between China and Europe

At present, the largest production capacity in the global chemical industry is concentrated in China and Europe. European chemical industry is affected, and we are the direct beneficiaries.

In the short term, due to the large cost gap between domestic and European chemical products, it has brought opportunities for domestic related enterprises to substitute energy for export;

In the long run, the current energy shortage in Europe may evolve into a major industrial transfer, increasing the overall market share of the Chinese market.

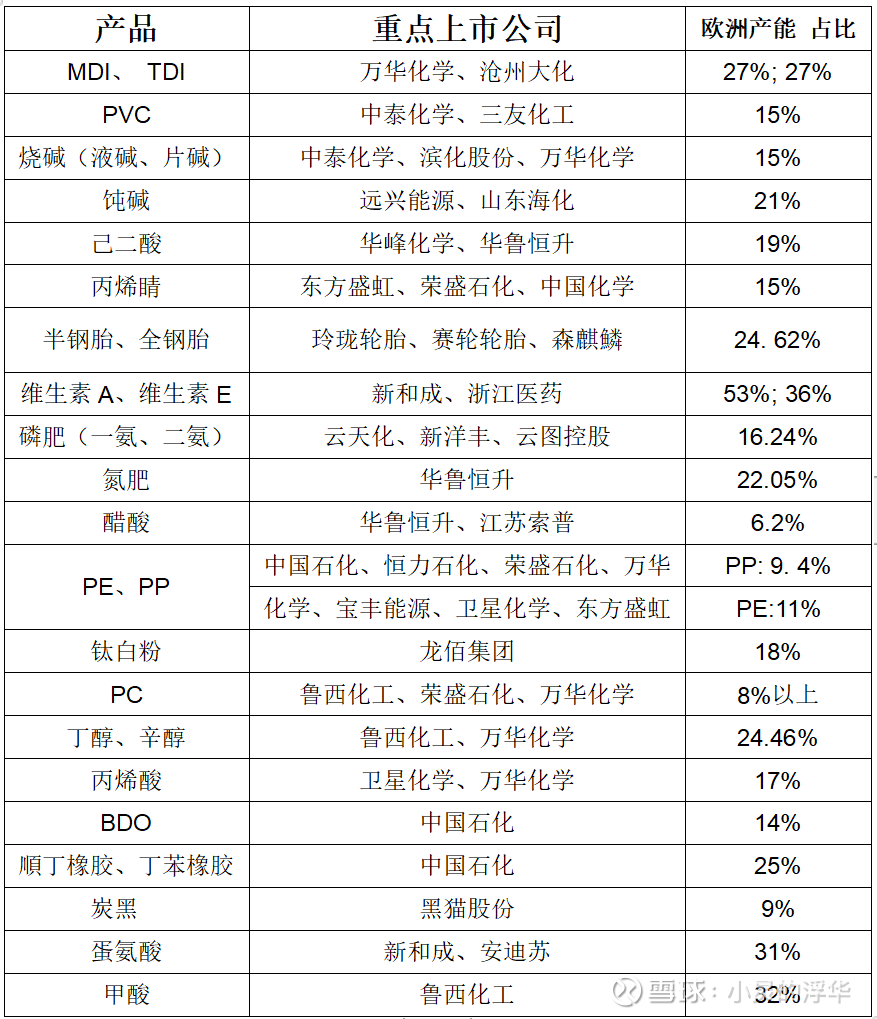

At present, Europe has a relatively high proportion of global production capacity including vitamin A/E, methionine, MDI/TDI, etc.

1. Vitamins

The global production capacity of vitamin A and vitamin E in Europe accounts for 50% and 30% respectively, and the rest are occupied by domestic manufacturers. Compared with Europe, there is a price difference of nearly 200 yuan/kg.

The price elasticity of vitamins is very large. At present, due to the weak demand due to the epidemic, the overall market is relatively sluggish. Once the subsequent industry enters the peak season and the production in Europe is superimposed, the elasticity may be relatively large under the double-click.

2. MDI/TDI

The global production capacity of European MDI/TDI accounts for about 27%, and China’s 40%. Due to rising natural gas prices in Europe, production costs have been pushed up substantially. At this stage, the cost of electricity and natural gas for European factories is 5 to 8 times that of Chinese factories, and the export volume has continued to rise in recent years. If production is stopped again, domestic MDI and TDI exports will continue to benefit.

In addition, chemical fertilizers and pesticides also have a certain quantity and price logic, which can be paid attention to.

Three, dry goods

Finally, a summary table was collected for everyone, which was compiled from public data.

$Wanhua Chemical(SH600309)$ $Cangzhou Dahua(SH600230)$ $Xinhecheng(SZ002001)$

This topic has 1 discussion in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/4193167292/230942598

This site is for inclusion only, and the copyright belongs to the original author.