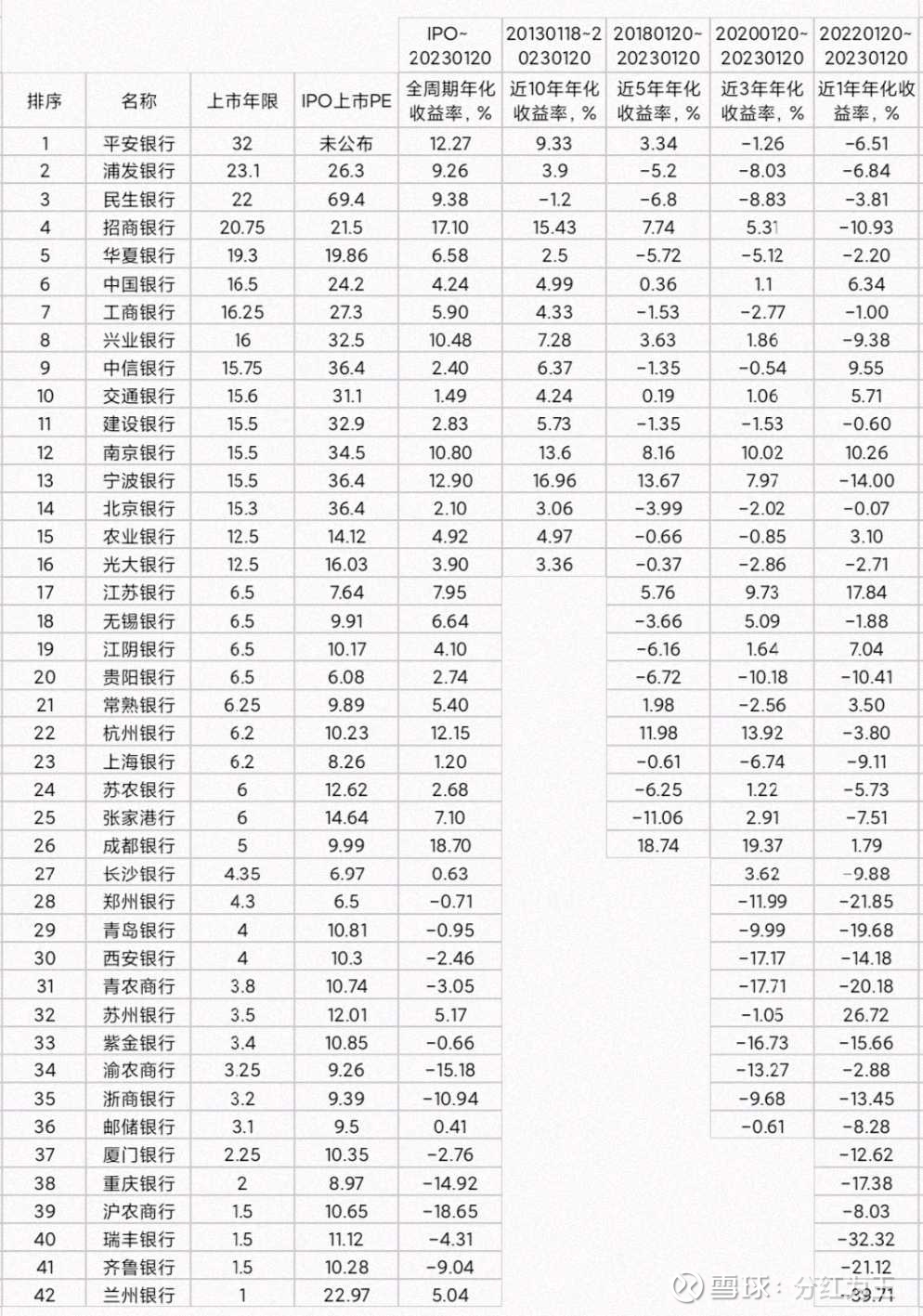

There are a total of 42 listed banks, including 33 in Shanghai and 9 in Shenzhen. Judging from the time of listing, there is a phenomenon of listing together: there is only one Ping An Bank that has been listed for more than 30 years, and has not announced a PE listing; there are 4 companies that have been listed for about 20 years, all of which are national joint-stock banks, Pudong Development, Minsheng, China Merchants, Huaxia, The IPO listing PE is about 20 times, among which Minsheng is special, the IPO listing PE is close to 70 times; there are 9 companies in about 15 years, 4 state-owned large banks, 2 joint-stock banks, 3 city commercial banks, and the IPO listing PE is more than 20 times. 30 times; 2 companies in 12.5 years, IPO listing PE15 times.

There are 10 companies listed in 5~6.5 years, 5 companies listed in about 4 years, 5 companies listed in about 4 years, 5 companies listed in about 3 years, 2 companies listed in about 2 years, and 4 companies listed in 1~1.5 years , except for the Postal Savings Bank of China, which is a large state-owned bank, all of them are city commercial banks or rural commercial banks.

Everyone knows that among listed companies, banks have a large total market value and a high proportion of net profit, but their stock prices have been sluggish for a long time. Yindi has a “good reputation” among the three idiots, and the banking sector is the best among the three idiots.

What is the rate of return on investment in listed banks?

Looking at the recent year, only 10 of the 42 banks recorded positive returns and 32 were losing money. The most outstanding performance is Bank of Suzhou, which has been listed for 3.5 years, with a 1-year return rate of 26%. In addition, Bank of Jiangsu and Bank of Nanjing are also good. Others have performed relatively poorly. More than 10 companies have lost more than 10%. Year.

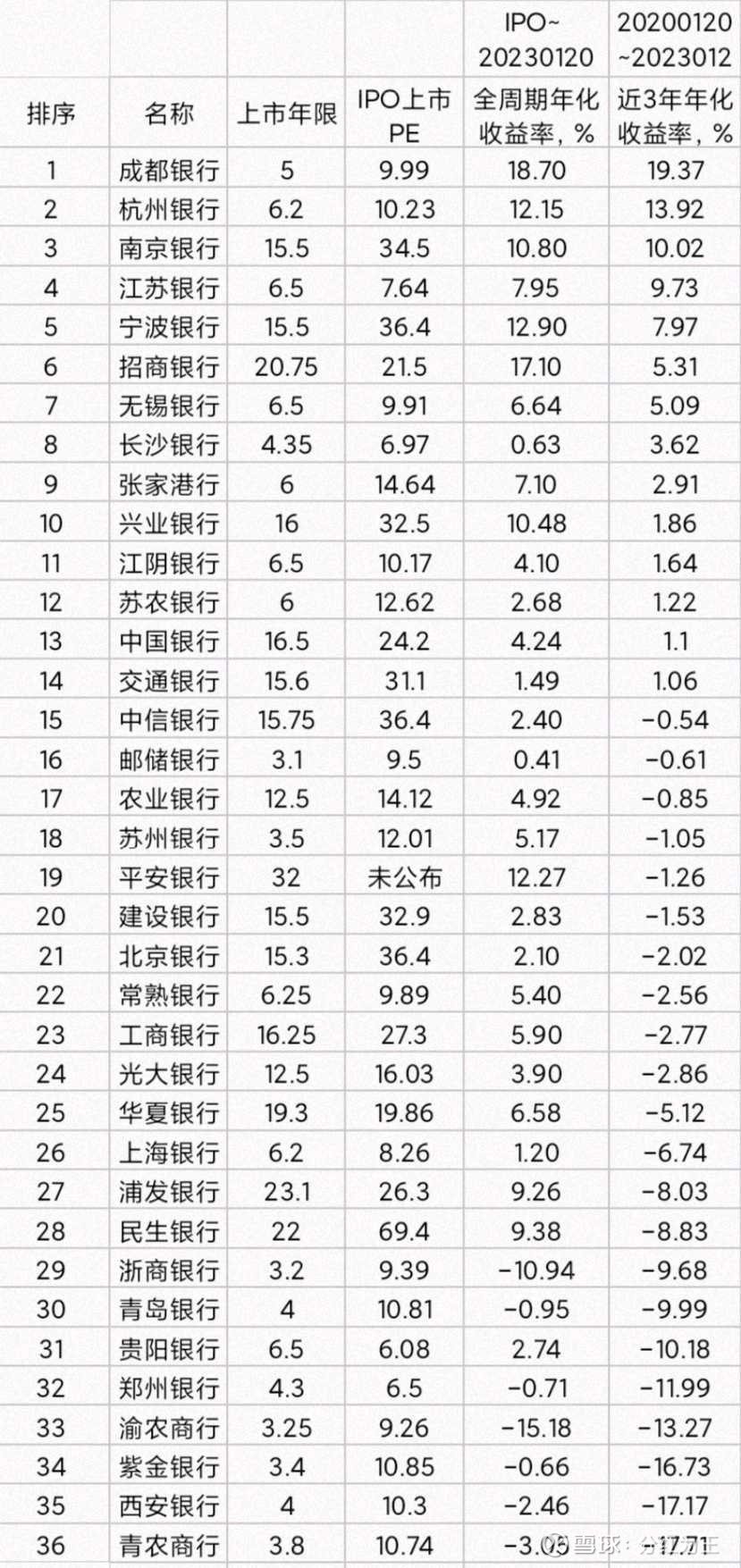

Look at the performance of the last 3 years. Of the 36 companies on the list, only 14 companies recorded positive returns, and most of them lost money. Bank of Chengdu stands out on this list, with an annualized rate of return close to 20%. Banks in Hangzhou, Nanjing, and Jiangsu performed well. On the contrary, on the list of latecomers, there are many people with large losses, of which 12 have an annualized loss of more than 5%. Most of them are sub-new banks that have been listed recently. In addition, Minsheng and Shanghai Pudong Development Bank, which have been listed for more than 20 years, also have an annualized loss of more than 8%, which is particularly eye-catching.

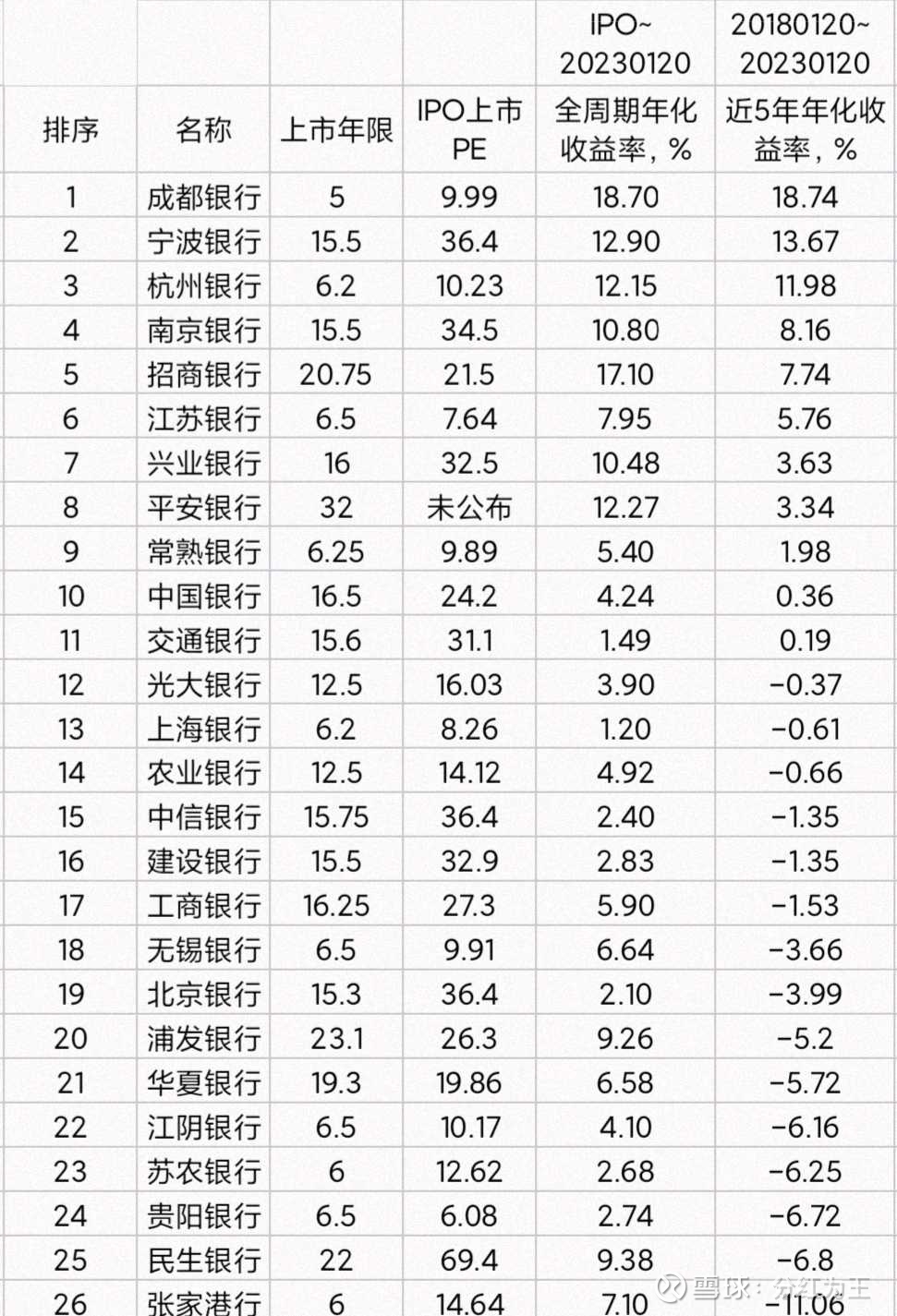

Looking at the situation in five years, there are 26 companies on the list, 11 companies have a positive rate of return, and 15 companies have a negative rate of return. They still lose more and win less. Bank of Chengdu ranked first, with an annualized rate of return of more than 18%, followed by Ningbo, Hangzhou, Nanjing, China Merchants, and Jiangsu. At the bottom of the list are still those banks that have been listed for a relatively short time. Unfortunately, Pudong Development and Minsheng are still behind the list.

Looking at the situation in the past 10 years, among the 16 companies on the list, except for Minsheng Bank, the remaining 15 companies have recorded positive returns. Unfortunately, most of them have relatively low returns, only slightly higher than long-term bank deposits. The champion is Bank of Ningbo, with an annualized rate of return of 17%. Among the ranks of other students, Minsheng is at the bottom with negative income.

To sum up: 1. The rate of return data shows that the overall performance of the bank is unsatisfactory. 3. The theory of bank homogeneity is not established, and the differentiation is still relatively obvious, which is manifested in two aspects: one is that the yield gap is relatively large, and the other is that the excellent performance is always better than the poor performance. Poor, Ningbo and China Merchants Bank have fallen more recently, but in a year’s view, the ranking is not particularly low; 4. The division of large joint-stock banks is particularly obvious. China Merchants, Ping An, and Industrial performed better, while Minsheng and Pudong Development performed poorly; 5. Large state-owned banks have low returns, but they are relatively stable, and their rankings are always in the middle; 6. Some city commercial banks have outstanding performance. Ningbo and Nanjing have been listed for more than 15 years, and their full-cycle and 10-year returns are among the best among all banks. Short-term The performance is also good, but the Bank of Beijing, which was listed at about the same time, did not perform well, indicating that the phenomenon of differentiation does exist. In the past five years, Chengdu and Hangzhou banks have also taken the lead, and their performances are very impressive. 7. Most of the urban commercial banks and rural commercial banks that have been listed for a relatively short period of time, especially less than 4 years, perform very poorly, and the annualized losses are shocking. Lanzhou Bank has a loss of 40% in one year, Ruifeng Bank has more than 30%, and the three-year annualized loss exceeds or Nearly 10% reached as many as 8 companies. Even Zhangjiagang Bank, which has performed well recently, has an annualized loss of more than 10% in 5 years. Think about the inner feelings of investors who hold these banks. Among them, there is one that has performed quite well. Bank of Suzhou has only been listed for 4 years, ranked relatively high in the past three years, and rushed to the top of the list in the past year. 8. Crisis breeds opportunities. For example, Sunong, Jiangyin, Wuxi and Zhangjiagang, which have a very poor annualized rate in 5 years, have recently shown signs of a dark horse flying into the sky. Guiyang, Xi’an, Zhengzhou, and Qingdao banks performed poorly, which once again verified the serious differentiation of banks.

Since banks as a whole have performed poorly in different cycles in the past, how should we look at investment opportunities in the banking sector? How to choose the target company that suits you? The following is my immature opinion, a judgment made by using common sense. As a non-professional, let alone a banker, my opinion is for reference only and must not be used as a basis for investment.

1. Today, the total market value of China Securities Bank is 9.42 trillion, and the total market value of China Securities All Index is 90.51 trillion, accounting for only 9.42/90.51=10.4%, but the proportion of net profit is as high as 1.59/4.25=37.4%. That is to say, the bank’s 1/PE (usually considered to be the company’s return to shareholders) is 3.6 times that of all listed companies. More importantly, the dividend rate of the banking sector is as high as 5.8%, while the dividend rate of the CSI All Index is only 2.28%, and the bank is more than 2.5 times that of the All Index. What is the concept of 2.5? Resolving it in 5 years means that the annualized rate is 20%, and the growth rate is 20% higher than that of banks. How difficult it is! Even if it takes 10 years to resolve, the growth rate needs to be 9.6% higher than that of the bank. Do you have the patience? Is the subject matter easy to choose? Therefore, the conclusion is very simple. Compared with all-finger, banks must be a good choice! 2. When is the right time to buy a bank? Obviously not. The backtest results of multiple cycles in the past were unsatisfactory, which shows that it was not suitable in the past, or most of the banks in the past were not suitable. But now it is different. It has fallen to the current level. The overall dividend rate of the banking sector has reached 5.8%. The backing effect of dividends has become stronger. Now is obviously a good time. It is the right time to be greedy when others are fearful. 3. Since the banks are severely differentiated, there is no difference in choice, and it is unrealistic to win if you lie flat. How many years will it take for Bank of Lanzhou to make up for the sharp decline in the past year? You must be cautious and prudent, control your greed, and it is also very important to control greed in greed! 3. It is relatively easy to do multiple-choice questions from companies that have performed well in the past, especially in different cycles. 4. After the excellent ones are selected, it is also very important to wait for a good price to see if they are undervalued. Only excellent + low prices can fall less and rise much more. 5. The low price means that the dividend rate may be relatively high. Note that what I said is possible. The situation of different banks is different. You must look carefully, and you must not be sloppy. 6. Dividends can be used to support the bottom line. High growth alone does not guarantee a certain profit, it depends on the sentiment of the market. And dividend + growth is the key to 100% winning. This issue cannot be viewed mechanically. What we are pursuing is high profitability in a certain period of time in the future. Compared with the current high dividend rate + low growth rate, and the current low dividend rate + high growth rate, we need to calculate which is better. The sum of dividends in a certain period of time, or the amount of dividends in each year in the future is taken into consideration. Some people blindly pursue high dividends and cannot guarantee satisfactory returns, while others only look at the growth rate, which is one-sided. 7. There are four parameters that affect the rate of return: base value and its changes, lifespan, current dividend rate, and future growth rate. The base value and the current dividend rate are known conditions, the number of years can be freely controlled, and only the future growth rate needs to be estimated. Roe, profit margin, provision coverage ratio, bad debt ratio, interest rate spread, capital adequacy ratio, loan-to-appropriation ratio, write-off, etc., must all be transformed into growth rates to work. The so-called growth rate here is more inclined to use the dividend growth rate as the standard of consideration. Estimating the growth rate is a winning skill that requires long-term practice. I belong to the rookie level, so I adopt the conservative method, and I would rather underestimate it than be too radical. It is very easy to deceive yourself, and you need to be very cautious. 8. If you are still not at ease, I have another big move, take your time! No matter how good the opportunity is, or no matter how optimistic you are, don’t just stud, divide the funds into several shares, have a bottom warehouse, a reserve team, and an ambulance team. It is nothing more than earning less, quitting greed, getting rich slowly, and losing at one time If you drop, you will lose the qualification for the game, and you are guaranteed to be present at any time.

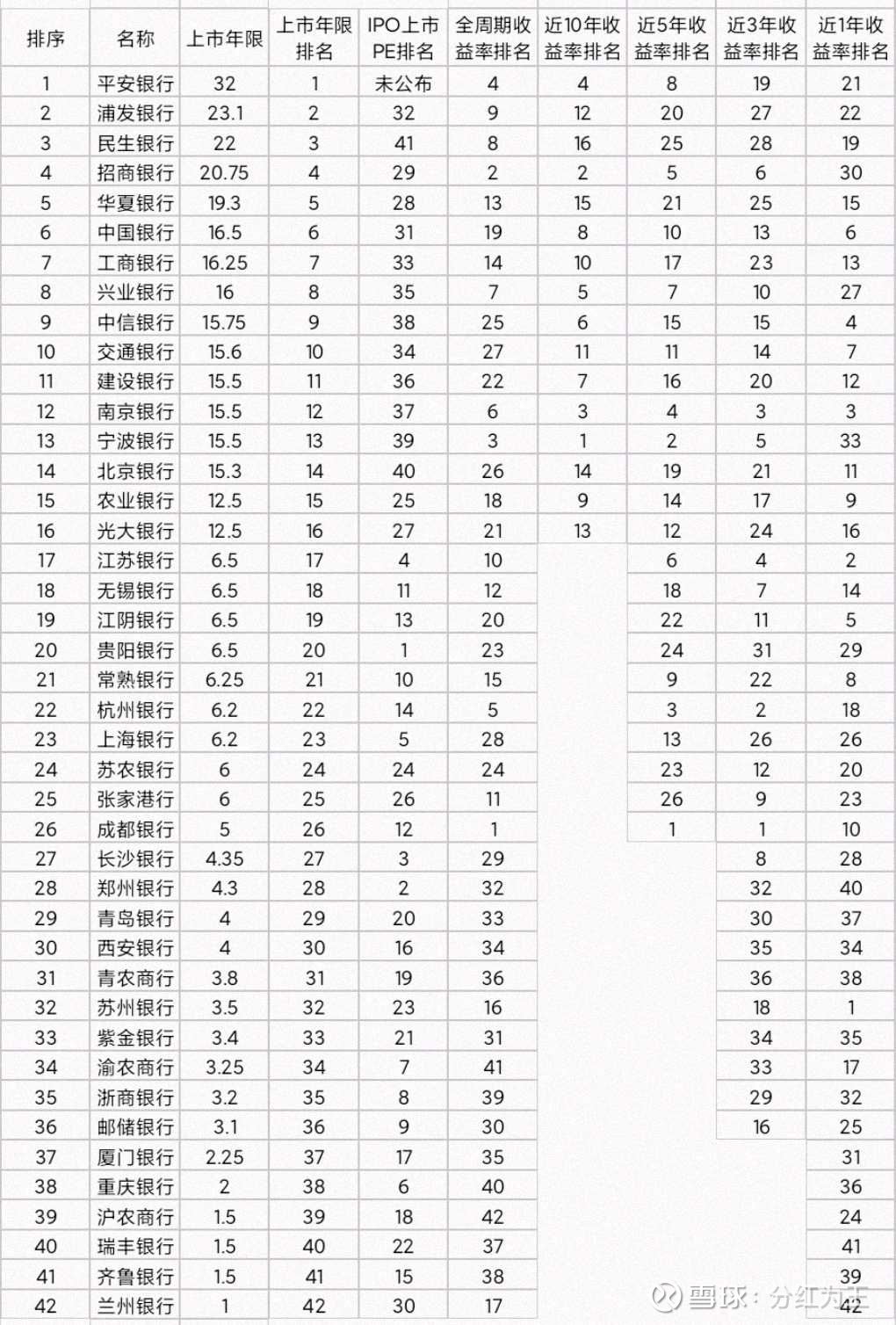

Put another picture, I express the performance of 42 banks in different periods with serial numbers, small serial numbers represent the top rankings, and more small serial numbers indicate excellent and stable performance, for reference by myself and my friends.

There are 21 discussions on this topic in Xueqiu, click to view.

Snowball is an investor social network where smart investors are all here.

Click to download Xueqiu mobile client http://xueqiu.com/xz ]]>

This article is transferred from: http://xueqiu.com/8713641876/241210646

This site is only for collection, and the copyright belongs to the original author.