Recently, China’s rights and interests continued to adjust, and the market sentiment was generally pessimistic. From the following dimensions, it is still necessary for everyone to remain rational, and to attach great importance to and review the allocation opportunities of China’s equity assets.

1. Macro Trends

1) Economic growth trend: At present, the asset-liability structure of US residents is better than before the epidemic, and the US real estate is in a state of high prosperity. However, the global economic inflation pressure is high, and the trend of tightening monetary policies by the Federal Reserve and central banks of various countries remains unchanged. The main global economic growth is still in the recovery trend, but the marginal growth rate may slow down in the future. Affected by the disturbance of the Omikojon epidemic in the first quarter, China’s economic growth performance was weak in the first quarter, but the policy of stabilizing growth will run throughout the year, and in order to achieve the annual policy target of 5.5%, the policy may be strengthened. It is expected that China’s economic growth will perform better in the next 2-3 quarters. Whether it is the “four trillion” after 2008, the rescue after the stock market crash in 2015, as well as supply-side reform, and “dynamic clearing”, historical experience tells us that at any time, never underestimate the determination of the Chinese government!

2) Inflation trend: The overseas economy dominated by the United States is currently recovering well, and the phenomenon of economic overheating is obvious. However, there is a significant gap in the supply of goods, the inventory is generally low, and the continued geopolitical disturbances such as the Russian-Ukrainian war have led to increased regional differences in commodities. Global inflation trends show signs of accelerating deterioration. However, in order to deal with inflationary pressures, the Fed and central banks will mainly respond with tight monetary policies. At present, China’s core inflation is not high, and it is mainly faced with imported inflation pressure due to high commodity and raw material prices, which restricts the easing range of China’s monetary policy to a certain extent. China’s overall inflation is under certain pressure, but the trend is more stable.

2. Asset value

1) Overseas: Under the pressure of high inflation and the tightening of the Fed’s monetary policy, the US debt is bearish, the valuation of US stocks is high, and the stage is cautious.

2) China:

Bonds: Driven by the expectation of the policy of “wide credit and stable growth”, there is pressure to adjust the yields of long-term bonds, but against the background of loose liquidity, the yields of short-term bonds tend to stabilize. There is room for a steepening of the yield curve.

Equity: China’s equity assets are not expensive, and their relative value is better than bonds. Further additions may be considered.

3) Commodities: The global commodity supply side and demand side have not seen fundamental changes, and driven by China’s steady growth policy, infrastructure investment continues to make efforts. In addition, the geopolitics of Russia and Ukraine may enter into a long-term consumption, and the supply of agricultural products, mainly corn and wheat, may deteriorate in winter, and the commodities are generally more cautious.

3. Risk Appetite

1) Overseas economic growth in the first quarter Due to domestic and overseas inflation expectations, there are signs of further deterioration, and the upstream and downstream transmission time of China’s inflation may be longer. Combined with the Fed’s interest rate hike, Russia and Ukraine’s geopolitics and other factors, investors’ overall risk appetite is low .

2) From the perspective of transaction congestion, the current transaction congestion of U.S. bond shorts and commodity longs is relatively high, and asset prices fluctuate greatly.

4. Latent Variables

1) The main ones with strong certainty are:

The Fed is raising interest rates, the marginal recovery of economic growth has slowed, and inflation has deteriorated further than expected. Driven by China’s stable growth policy, loose monetary and fiscal policies, it is only a matter of time before the economy stabilizes.

Populism and rising protectionism have triggered a trend of instability in the international political environment.

2) The main doubts about certainty are:

With the Fed raising interest rates and the cyclical disturbance of the epidemic in the global economy, can the slowdown of the economic demand side effectively curb inflation?

Will the commodity supply gap and geopolitics further worsen inflation expectations?

Although the direction of China’s monetary policy easing has not changed, due to the constraints of inflation, the interest rate gap between China and the United States has narrowed, and the scope of easing may be limited.

There is uncertainty as to whether China’s early-stage industry control policies focusing on real estate and the Internet have substantially slowed down and whether they can be implemented.

The development of Russia and Ukraine. And will the international political environment deteriorate further?

Finally, let’s take a look at the value of China’s equity assets:

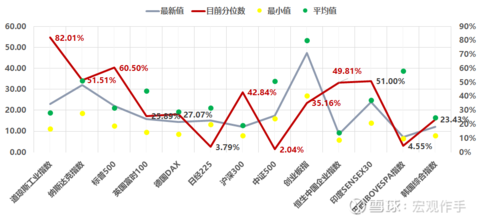

1) Compared with bonds, the equity value has a prominent advantage. Under a specific interest rate environment, the CSI 300 is basically close to the historically low valuation level in 2015 and 2018.

2) Compared with overseas equity assets, China’s equity assets have obvious advantages in valuation. The margin of safety is outstanding!

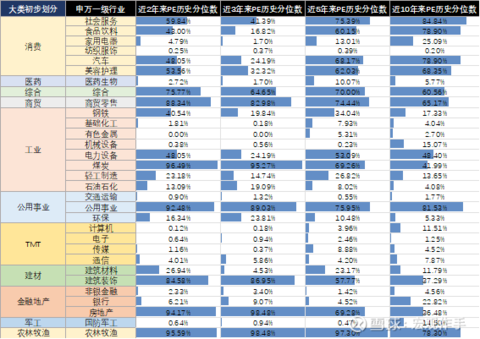

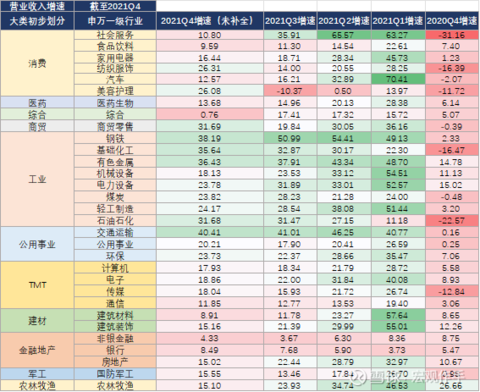

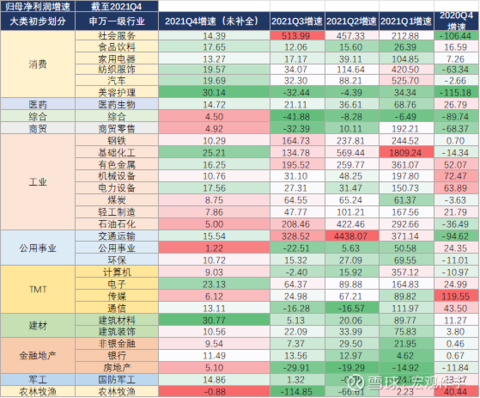

3) From the perspective of the A-share industry structure, more and more industries are close to historically low valuations, but corporate profits are not bad.

In addition, for the specific valuation of equity, you can also refer to:

The Rational Judgment Perspective of CSI 300 Valuation and Performance

In the end, what I want to say is that “pessimists are right in the short term, and optimists win the future.” Please view the market rationally.

This topic has 40 discussions in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/1686401828/218099321

This site is for inclusion only, and the copyright belongs to the original author.