(The picture comes from the official Weibo of Tuya Smart)

(The picture comes from the official Weibo of Tuya Smart)Welcome to the WeChat subscription number of “Sina Technology”: techsina

Text | Hernanderz

Source: Value Institute

The revenue declined year-on-year, but the loss continued to narrow and the gross profit margin also improved. Tuya Smart delivered a transcript that was not perfect but not lacking in bright spots in the second quarter.

As far as the data of the second quarter is concerned, SaaS and other businesses have made the greatest progress, but the performance of the main IoT PaaS business is not satisfactory, which is also the main reason for the year-on-year decline in revenue. The narrowing of losses and the improvement of gross profit were mainly due to better cost control.

In general, Tuya Smart’s performance in the second quarter was unsatisfactory. The main reason is that the market environment is not bad, and both the entire IoT industry and the PaaS track are in a state of rapid growth. The platform itself must bear a lot of responsibility for the decline in revenue.

Taking the cost-effective route, through low-cost modules and huge distribution channels and marketing activities, Tuya Smart has been questioned by the lack of technical barriers for a long time. This is also directly reflected in the reliance on third-party suppliers and public cloud platforms. As smart home manufacturers accelerate their cloud adoption, the growth potential of Tuya Smart is certainly worth looking forward to, but there will be more and more competitors.

Just over a year after the listing, the market value has evaporated by 90%. Tuya Smart has no way out now, but can only face the difficulties.

Tuya Smart Q2 financial report released

Losses narrowed as the biggest bright spot

Taking advantage of the trend of smart home, the development prospect of “the first share of IoT cloud platform” Tuya Intelligence was once optimistic. After landing on the US stock market in March last year, the market value once soared to a peak of more than 10 billion US dollars. But now, its market value and stock price have fallen by more than 90% from the peak, and the severe losses have deeply worried its investors and analysts.

After the U.S. stock market closed on August 30, Beijing time, Tuya Smart released its second quarter financial report for fiscal 2022 as scheduled. Data shows that Tuya Smart’s revenue in the second quarter saw a year-on-year decline, and overseas business was still affected by unfavorable factors such as the epidemic and inflation. But the good news is that losses continued to narrow in the quarter and gross margins improved, and overall it was a mixed bag.

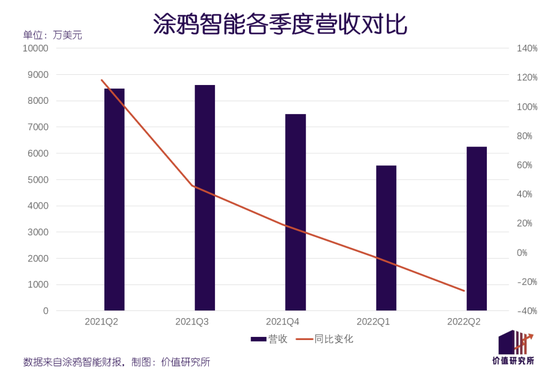

Let’s look at revenue first. Data shows that Tuya Smart’s total revenue in the second quarter was US$62.5 million, down 26.1% year-on-year. It should be noted that this is the second consecutive quarter of Tuya Smart’s revenue decline, and the decline is significantly larger than that in the first quarter.

In the first quarter of this year, Tuya Smart’s revenue was US$55.32 million, a year-on-year decrease of 2.72%, which was the first year-on-year decline since its listing. I had hoped that Tuya Smart could make a turnaround in the second quarter, but who knew the situation would get worse.

Tuya Smart’s revenue mainly comes from three segments, namely IoT PaaS services, smart device distribution business, and SaaS and other value-added services. As far as the data of the second quarter is concerned, the biggest improvement is in SaaS and other businesses, but the performance of the main IoT PaaS business is not satisfactory.

According to the financial report data, the revenue of Tuya Smart IoT PaaS business in the second quarter was 47.6 million US dollars, a year-on-year decrease of 38.1%, and the revenue ratio remained above 80%. As for SaaS services, although it recorded a year-on-year growth of 114.3%, the revenue achieved was only US$7.2 million, which was still a drop in the bucket for the entire company.

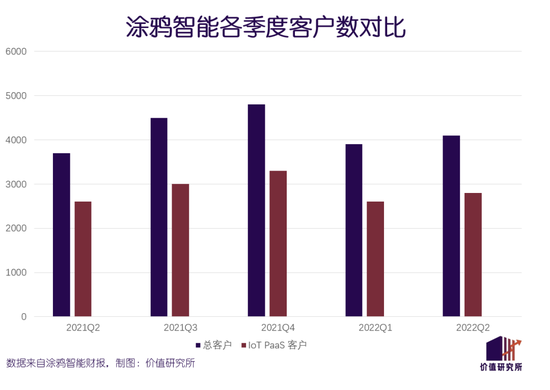

Tuya Smart’s IoT PaaS service revenue comes from fees for providing customers with cloud links, basic IoT and edge computing services. The more devices the customer connects, the more PaaS modules, and the higher the revenue. In the first half of the year, the growth of the customer scale of this business was relatively limited, which was an important reason for the sharp contraction in revenue.

Data shows that by the end of the second quarter of this year, the total number of Tuya smart customers was about 4,100, an increase of only about 400 over the same period last year and an increase of about 200 over the first quarter of this year. Among them, the number of IoT PaaS customers in the second quarter was 2,800, a year-on-year increase of only about 200. To make matters worse, both figures are down significantly from their peaks in the fourth quarter of last year. Data shows that in the fourth quarter of last year, the total number of Tuya Smart customers and IoT PaaS customers were 4,800 and 3,300 respectively.

However, this financial report is not without its bright spots – the most gratifying is undoubtedly the contraction of losses and the improvement of gross profit margins.

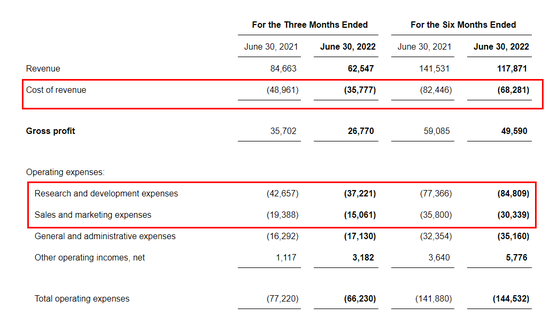

Data shows that Tuya Smart’s operating loss in the second quarter was US$39.5 million, down 5% year-on-year; non-GAAP operating loss was down 15.9% year-on-year to US$22.3 million, and the corresponding non-GAAP loss rate was significantly narrower than the first time. This is the first month-on-month improvement since the third quarter of last year.

In terms of gross profit, the company’s overall gross profit margin increased by 0.6% year-on-year to 42.8% in the second quarter, and the gross profit of each business segment has also been improved to varying degrees. Among them, the gross profit margin of the IoT PaaS business, which experienced a major decline in revenue, also increased slightly to 42.5% from 42.4% in the same period last year.

In the case of declining revenue, gross profit can also achieve significant improvement, mainly due to better cost control.

Looking at the cost structure, it can be found that Tuya Smart’s revenue in the second quarter decreased by 25% from $35.7 million in the same period last year to $26.8 million today, and total operating expenses decreased by 14.2% year-on-year to $66.2 million. Among the expenses, research and development expenses and sales and marketing expenses decreased significantly, and only general and administrative expenses increased slightly.

(The picture comes from Tuya Smart Financial Report)

(The picture comes from Tuya Smart Financial Report)In general, however, the performance of Tuya Smart in the second quarter was difficult to satisfy investors. After all, the demand for smart home cloud services is in the explosive stage, and it stands to reason that Tuya Smart, as a senior player, should be the beneficiary.

According to the report of the Prospective Value Research Institute, the scale of China’s Internet of Things industry has exceeded 500 billion yuan, and it has maintained a compound annual growth rate of nearly 40% in the past five years. As for the IoT PaaS business of Tuya Smart Betting, according to CIC data, the scale will be US$94.6 billion in 2021, and it is expected to reach US$194.8 billion in 2026, with a compound annual growth rate of about 15.5% in the next five years. A track with high growth and high potential.

The market environment is not bad, and the platform itself must bear a great responsibility for finally handing over such a mixed transcript.

After comprehensively deconstructing Tuya Smart’s revenue model and growth experience, the Institute of Value (ID: jiazhiyanjiusuo) believes that the crux of all problems has been laid down very early.

Lack of technical barriers

The biggest life gate of graffiti intelligence

Just over a year after its listing in the United States, Tuya Smart landed on the Hong Kong Stock Exchange on July 5 this year in the form of dual main listings, becoming one of the Chinese stocks with the shortest time between listings.

Two listings in a short period of time, many people attribute the reason to the extreme pressure of the US SEC and the multiple rounds of plummeting stocks listed in the US in the first half of this year. But another unavoidable fact is that Tuya Smart has continued to decline in performance since the second half of last year.

As mentioned above, IoT PaaS is Tuya Smart’s most important revenue pillar, and the ups and downs of its performance are naturally largely linked to the development of the business. The biggest problem with this main business is that it has been accustomed to extensive growth and a long-term route of small profits but quick turnover, and has never blocked the gap in the technical link.

Since its inception, Tuya Smart’s IoT PaaS business has taken a cost-effective route, using low-cost modules, huge distribution channels and marketing campaigns. In 2017, Tuya Smart co-founder and COO Yang Yi once told the media that what Tuya Smart wants to do is to “popularize smart homes”.

“The popularity of the smart home market depends on a number of factors, one of which is the price breaking a tipping point.”

At that time, the three international giants of Amazon, Google and Apple were the rulers of the smart home industry, and the domestic market was still in its infancy, and there was no scale effect. Tuya Smart IoT PaaS service is aimed at small and medium-sized manufacturers at home and abroad, providing low-cost acquisition modules and cloud services, with certain advantages in price. It was not until it continued to grow and developed that it won a few large customers such as Philips and Calex.

In the years when the valuation was rising, the number of Tuya Smart customers and the number of IoT PaaS devices supplied were in a state of explosive growth. In 2019, the number of IoT PaaS devices deployed by Tuya Smart reached 60.1 million units, and the number soared by 94% to 117 million units in the following year, the scale of which is second to none in the industry.

However, relying on the sales scale to drive marketing and the main strategy of focusing on market promotion and ignoring technology research and development have made Tuya Smart suffer from long-term doubts about the lack of technical barriers. The technical defects of Tuya Smart are directly reflected in the dependence on third-party suppliers and public cloud platforms.

On the one hand, it can be seen in the prospectus and the financial reports of the past two years that the production of Tuya Smart IoT PaaS modules is mainly entrusted to third-party suppliers. These modules can only function properly by embedding IoT PaaS edge computing functions in the modules through third-party suppliers, and Tuya Smart itself does not have the ability to produce independently. From this perspective, Tuya Smart is closer to the role of an OEM.

In its annual report for the last fiscal year, Tuya Smart admitted that the shortage of chips has had a serious impact on its business. The reason for this is that it still lacks upstream bargaining power and technological competitiveness, and both core components and production links are very dependent on external cooperation.

On the other hand, from the early days of Amazon AWS to the now joined Microsoft Azuer and Tencent Cloud, Tuya Smart IoT PaaS cloud service infrastructure has always been hosted by third-party public cloud vendors. In addition, the SaaS business, which has been vigorously developed in the past two years, also relies on public cloud service providers to provide underlying technical services.

It should be noted that due to the gradual saturation of the IaaS public cloud market, the SaaS track is too fragmented, and it is difficult to form a head effect. Many cloud service companies will focus on the PaaS platform service for the next stage of expansion. For example, Huawei, which launched the Whole House Intelligence 2.0 version earlier this year, is a new and heavy player in the IoT PaaS track.

For Tuya Smart, the intervention of these manufacturers is not only equivalent to bringing new competitors, but also more likely to affect the cooperation between the two parties in public cloud services.

At present, Tuya Smart has no way out. It seems that only by making up for the shortcomings in technology and building up our own competitive barriers can we fundamentally solve the troubles of growth.

Smart home manufacturers accelerate cloud adoption

Opportunities and challenges of Tuya Intelligence

On August 25, Tuya Smart released the latest version of the Matter solution, providing customers with the world’s first services and products that support the Matter protocol.

Readers familiar with the trends in the smart home field should know that the Matter protocol is an application-layer connection protocol jointly initiated by Tuya Smart, CSA Connection Standards Alliance, Google, Amazon, and Apple and other leading companies. It aims to break the ecological barriers in the smart home field and achieve different The seamless connection of brands and different types of smart devices creates a real smart ecosystem.

The interconnection of the smart home industry is undoubtedly a brand new opportunity for cloud service providers such as Tuya Smart. Because behind it, there is a general trend of smart home manufacturers going to the cloud in an all-round way and accelerating the transformation to scale and platform.

From 2012 to 2019, it was the outbreak period of the domestic smart home industry. The number of registered companies increased from 6,000 to more than 60,000, a tenfold increase. However, after a round of big waves, the industry has gradually entered a mature stage, and enterprises above designated size have become the protagonists.

After the pattern stabilizes, it becomes difficult to widen the boundaries of competition externally, and internal interconnection becomes the growth driver for manufacturers. In December last year, the “Technical Requirements for Cross-Platform Access and Authentication of Smart Home Systems” jointly formulated and released by the China Household Electrical Appliances Association and the China Communications Standards Association will confirm this trend.

Nowadays, smart home products between different brands urgently need to break through ecological limitations and become interconnected, and migrating to the cloud is the most direct option. Taking smart security products as an example, CSHIA statistics show that more than 92% of smart security products in China have cloud requirements to realize seamless connection of smart door locks, cameras and other products. In this process, Tuya Smart-based PaaS/SaaS service providers are the communication bridges that smart home manufacturers need to rely on.

It is undeniable that Tuya Smart has its own advantages in the main track of IoT PaaS.

Officially disclosed data shows that since 2020, the number of newly connected devices and the year-on-year growth rate of Tuya Smart IoT PaaS services have ranked first in the industry. Although it is not technically outstanding, the development platform with strong compatibility is enough to connect the systems of various basic cloud platforms, which is attractive to developers who need to migrate products frequently and smart home manufacturers who are eager to connect across platforms.

Of course, if the outbreak of market demand is an opportunity for Tuya Smart, then with the expansion of the industry and the increasing number of competitors, it will bring new challenges to it.

The aforementioned Huawei is the most worthy competitor of Tuya Smart.

Huawei’s smart home business started out as a PaaS platform service, and is still deploying around its HiLink developer platform. In the newly released Whole House Intelligence 2.0, Huawei’s HiLink solution can provide interconnection among IoT products such as mobile phones, tablets, and smart wearables, and break down barriers to third-party IoT connections. For example, Huawei’s open API interface can realize the interconnection with Midea M-Smart and other systems/devices.

On Xiaomi’s side, although the willingness to open the IoT ecological chain to third-party manufacturers is not strong, it is also working hard to strengthen the developer team within Xiaomi’s smart ecosystem. All in all, it is not easy for Tuya Smart to cut a bloody path among the powerful enemies. Whether it can be successful or not, perhaps only time will tell us the answer.

write at the end

After successfully listing in the United States, Chen Liaohan, CEO of Tuya Smart, confessed to the media about his tortuous experience at the beginning of his business and his inner suffering.

“It took a year and a half to get our first customer, and we had doubts about ourselves at the time: Did we choose the wrong direction? Did we enter the track too early?”

Facts tell us that Tuya Smart’s path is not wrong, and the time of admission is correct. On the contrary, as early as 2014, Amazon and Google bet on the smart home track. The former’s Alexa smart speaker and the latter’s Google Home series products were both born during this period, and they also planted the seeds of an explosion in the smart home market. . Looking back now, Tuya Smart chose to bet on the IoT cloud service track, which also perfectly caters to the development trend of the smart home industry.

The market growth and potential of IoT cloud services are trustworthy, and the benign market environment has not collapsed due to objective factors such as the epidemic. What we need to see now is whether Tuya Smart can withstand the pressure of competition, strengthen its shortcomings, and maintain the share advantage that it has finally saved.

(Disclaimer: This article only represents the author’s point of view and does not represent the position of Sina.com.)

This article is reproduced from: http://finance.sina.com.cn/tech/csj/2022-08-30/doc-imiziraw0373109.shtml

This site is for inclusion only, and the copyright belongs to the original author.