Today, I sorted out the bond and bill financing of Yangtze Power, and I also saw a little problem.

Don’t talk, just take the picture first.

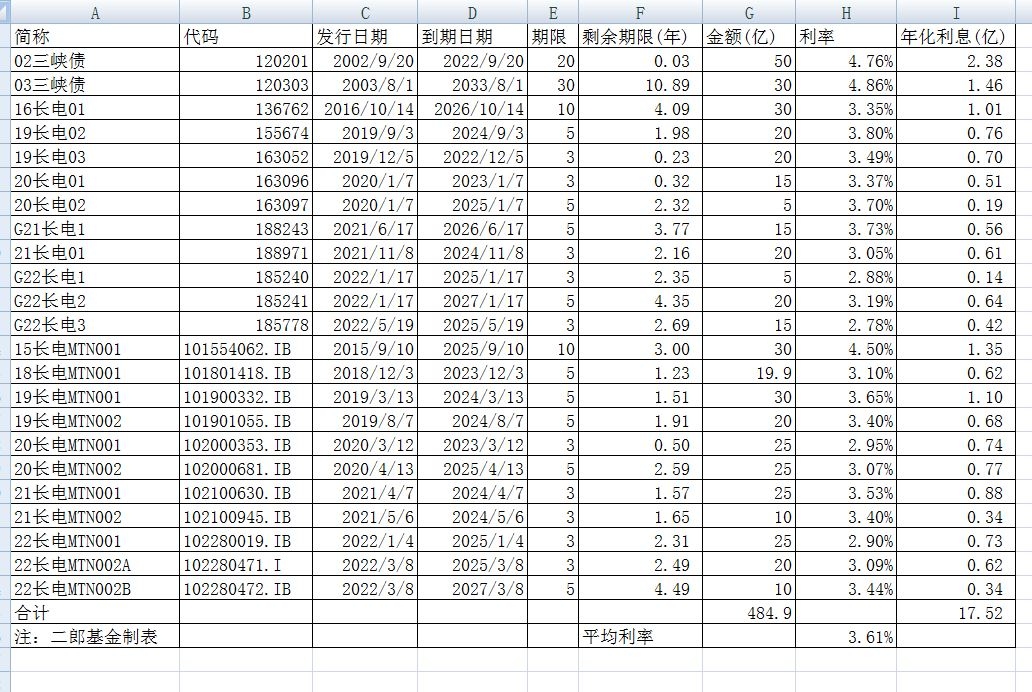

As of the middle of 2002, the financing balance of Yangtze Power’s bonds and bills was 48.49 billion yuan. After deducting the 5 billion yuan due on the 20th of this month, the balance will drop to 43.49 billion yuan. The actual interest rate cost calculated on average according to various financing interest rates and financing amounts is 3.61%. If the 5 billion bonds due this month are deducted, the real interest rate cost falls to 3.48%

From the table, we can see two phenomena: First, in the past three years, Yangtze Power has mainly issued medium-term bonds and notes, with a maturity of less than 3 years and a small amount of 5-year bonds; The remaining maturity of the bonds worth 100 million yuan is beyond 10 years, and the remaining maturity of the remaining bond notes is basically 3 years, or even 2 years. The above two points show that the company is short-term in direct financing.

The advantage of short-termization is that it can continue to enjoy the continuous downward trend of China’s interest rate level in the past three years, so that the cost of debt has fallen year by year. It’s also a clever move by the company to take advantage of the interest rate trend environment over the past three years.

However, as the world enters the interest rate hike cycle, China’s opposite interest rate cut policy has gradually reached the point of exhaustion. The “liquidity trap” seems to have arrived, and with the pressure of RMB depreciation, China may be forced to turn to raising interest rates. In other words, China may stimulate the growth of corporate financing needs by creating expectations of interest rate hikes. Whether it is raising interest rates or creating interest rate hike expectations, it will lead to a rise in bond yields. So, the time window for low interest rates may be running out.

Take another look at what happened to Treasury yields on September 9, 2022. The yield to maturity of the 10-year treasury bond is 2.635%, a decrease of about 19BP compared with 2.8276% six months ago; the yield to maturity of the 20-year treasury bond is 2.9363%, a decrease of 28BP compared with 3.217% six months ago; The yield to maturity of treasury bonds is 2.1779%, a decrease of about 12BP compared with 2.3017% six months ago; the yield to maturity of 5-year treasury bonds is 2.4184%, a decrease of about 12BP compared to 2.5422% six months ago. It can be seen that in the past six months, long-term interest rates have fallen even more .

Assuming that Yangtze Power’s bonds are issued at a premium of 50BP, then the 10-year interest rate is only 3.135%, which is far lower than the current company’s 3.48% interest rate cost. The 20-year period is only 3.4363%, which is basically similar to the current interest rate cost.

Long-term interest rates fell more sharply, which is precisely the rare time window for issuing long-term bonds. Therefore, based on the current interest rate environment, I believe that Yangtze Power can properly consider issuing long-term bonds in the next three months, and it happens that the 5 billion 20-year 4.76% bonds due on the 20th of this month are exactly one good replacement opportunity. Therefore, it is recommended that companies not only focus on driving down the cost of short-term interest rates and ignore long-term debt allocation.

At the same time, another advantage of issuing long-term bonds is that if interest rates rise and bond prices fall in the future, you can consider repurchasing bonds and replacing them with short-term bonds. If the interest rate level falls further, you can further consider replacing the current short-term bonds with long-term bonds.

In the past three years, Yangtze Power has adopted the method of replacing long-term debt with short-term debt. In the next one to two years, especially in the next three months, it may be possible to start a cycle of long-term debt to short-term debt.

Therefore, it is recommended that the company consider to seize the current low interest rate environment in the next six months, and gradually increase the issuance of 10-year or even 20-year long-term bonds to help the injection of Wubai assets. @ChangdianJD

There are 15 discussions on this topic in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/8164125924/230498606

This site is for inclusion only, and the copyright belongs to the original author.