Returning to Snowball after two years, I will record some investment thoughts next. This time, the role has changed a bit. In the future, I will mainly talk about macro, industry and investment methods, and try to avoid individual stocks. Maybe individual stocks in the US stock market can be mentioned as an example. Let’s briefly talk about recent opinions.

1. The current macro environment and stock market stage.

Recently, a grand narrative has become popular. This is basically the same at present, and nothing new can be said. For details, see the latest articles by Zoltan and Stanley Druckenmiller ( web link , web link ). We just need to understand and follow this narrative. The ten-year narrative will not determine the market in the next one or two years (recall that everyone’s zz worry about the fall in 2018 will be fulfilled, but it has not affected the bull market in 2019 and 2020).

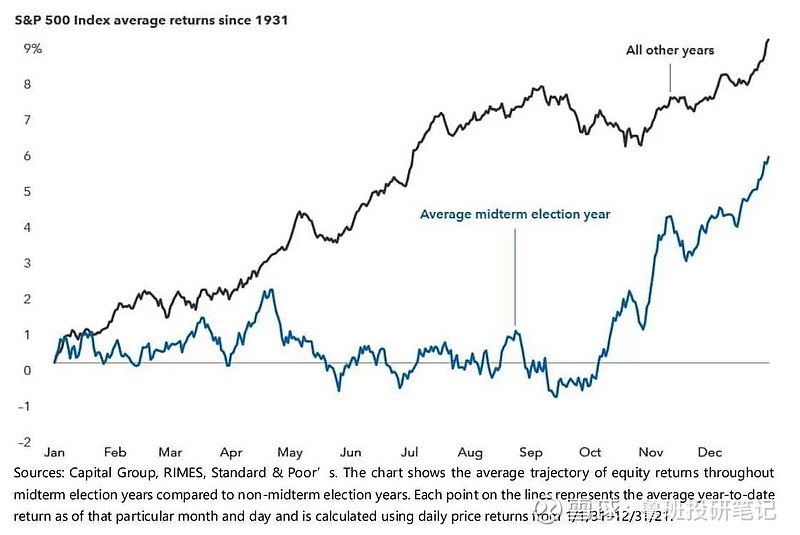

From the three perspectives of EPS, liquidity and risk appetite, A-shares have poor EPS, and the probability of continuing to be poor in the next six months is high, and the liquidity is moderate. Risk appetite is poor before the important meeting next month, and is likely to improve after that; The EPS here is poor, the liquidity is poor, and the risk appetite is poor; the EPS here in the US stock market is slightly worse, and the decline rate is not too fast. For now, just keep a low position and wait and see. Different ghost stories are fermenting on both sides, and everyone is avoiding uncertainty. It is expected that around the middle of the fourth quarter of this year, the world will have a good opportunity to participate (is it the ultimate outsole? When the time comes), the political uncertainty will drop significantly, the Fed’s attitude will be a little clearer, the market position will be more cost-effective, and the very high cash position ratio of major funds will be converted into the driving force for going long. (The picture below is the statistical law of the performance of US stocks in the mid-term election year, just for comfort)

2. We are optimistic about the opportunity.

Opportunities for US stocks are mainly in new energy. The unprecedented stimulus policy of US$369 billion has been introduced. The measures will be gradually implemented in the fourth quarter of this year, and will be stronger next year. The penetration rate is very low, the growth rate is quite high, and the valuation is not expensive (PEG is generally in 1), the combined odds are very good. The targets are concentrated in photovoltaics, hydrogen energy, energy storage, electric vehicles, Sic and other directions. If the Fed’s interest rate hike attitude begins to ease at some point in the next year, then bonds have a good opportunity (there are some bond ETFs in the stock market to choose from), and high-value growth stocks represented by SaaS will have a wave of valuation repairs.

We will continue to pay attention to the opportunities of A-shares. The overall penetration rate of new energy is high, but the penetration rate in some places is not high. For example, the intelligentization of automobiles still has the story of domestic replacement of parts and the increase of new technology penetration. The long-term value of coal has risen, and it is worth participating in the fall. Oil transportation in the cycle is a better direction. If Apple releases MR products as scheduled and becomes a hit in the first half of next year, then the VR direction is very good, and we will see when there is news on this product. The other is to keep paying attention to real estate, and leading real estate companies will interpret the logic of increasing concentration. If the economy stabilizes, many high-quality home furnishing, building materials and other companies in the supply-side reform will have obvious opportunities for reversal.

The opportunities for Hong Kong stocks are currently mainly in some high-dividend assets, and high dividends have a guarantee for the bottom. The trading volume of small and medium-sized bills in Hong Kong stocks has shrunk too much, and it is difficult to discuss reasonable pricing of assets with extremely low liquidity. Hong Kong stock EPS depends on China’s economy, liquidity depends on the pace of Fed rate hikes, and risk appetite depends on Sino-US relations, so the improvement is estimated at the latest, but the improvement will be very concentrated, and the magnitude of those concentrated votes will be exaggerated. There are one or two leading companies in the Internet and automobiles. Their long-term stories and recent growth are not bad. After the market improves, they should perform very well. There are several new energy parts companies in the Hong Kong stock market, which is also a period of explosive performance. It is estimated that they also have a good chance after the big votes.

_______

The public products managed by Da Chun Luban No. 1 A (P000887)$ are not very long, more than three years, but there are many tests during the period, the market style has changed several times, and there are also many black swans (during the epidemic, the U.S. stock market was blown out, Russia-Ukraine conflict, Internet anti-monopoly, etc.), fortunately, it has achieved a good rate of return and good drawdown control. For specific rankings, you can see the performance of Snowball Wind and Private Equity in the same period.

Attribution is mainly from two aspects: income creation and control drawdown. As I said in the previous roadshow, there are mainly four types of models for income creation. What we have done in the past year or two is to continue to improve this model. David of growth stocks The double-click model, the fermentation model of grand stories, the cycle-reversal model of simple variables, and the one-time shock dip-buying model of outstanding companies. Our revenue sources are different every year. From the perspective of the industries that contribute the most to profits, in 2019, we rely on A-share pork and Hong Kong stock properties; in 2020, we rely on the Internet and tax exemption of Hong Kong and US stocks; in 2021, we rely on lithium ore rare earths and auto parts; New energy and A-share energy storage. Controlling the drawdown is not a method in essence, but a character and attitude. The character is cautious, and it is easy to get nervous when losing money. It is not a bad thing for asset management (although the big guys are all promoting that they are not panic, the more they fall, the more excited they are, but I am not at all about this. agree). There are also some principles in the specific implementation. For example, after the fundamentals step on the thunder, it is found that at least half of the loss will be stopped on the same day (for example, when a chip position encountered the US sanctions last year, we will go out). When the opportunity for repair is reached, the position has also been greatly reduced (for example, on the day of the big drop after Powell’s Jackson hole speech, we think it is the beginning of a new round of decline, and it is also the day when the overall position is reduced).

@@ Call me the village party secretary @ @Ricky @ @linjia510 @@ shenghe@@金年@@无奇一平@ @epic steamed buns @ @陈子艺@@ PaulWu @ @刘志超@@心无Share HK @ @ drunk ink light song

There are 14 discussions on this topic in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/7449241987/230991879

This site is for inclusion only, and the copyright belongs to the original author.