This article is submitted for “Snowball Reference”, the deadline for the manuscript is June 22, and all the data in the article is before this date.

I usually pay more attention to the consumer industry, so I also pay attention to the product of Yongying Consumer Theme A. At present, the market value of A shares is about 80 trillion yuan, and the consumer industry is about 12 trillion yuan. There are countless related fund products. However, I am concerned about the product of Yongying Consumer A, which is mainly stable and enterprising, balanced and focused. features that piqued my interest.

performance

Compared with the CSI 300 Index, it has obvious yield advantages. The first trading day of the product listing was November 6, 2018. As of June 21 this year, the cumulative income was 215%, and the annualized rate of return was 37%. During this period, the cumulative yield of CSI 300 was 32%.

Compared with the CSI Wine Index, which is betting on the star track of the consumer industry, the yield is almost the same, but the stability and drawdown are greatly reduced. The cumulative decline was -8%, while the Yongying consumer theme A had a positive return of 0.14% in the same period. And the volatility and retracement are all due to the CSI Wine Index.

Fund manager investment style

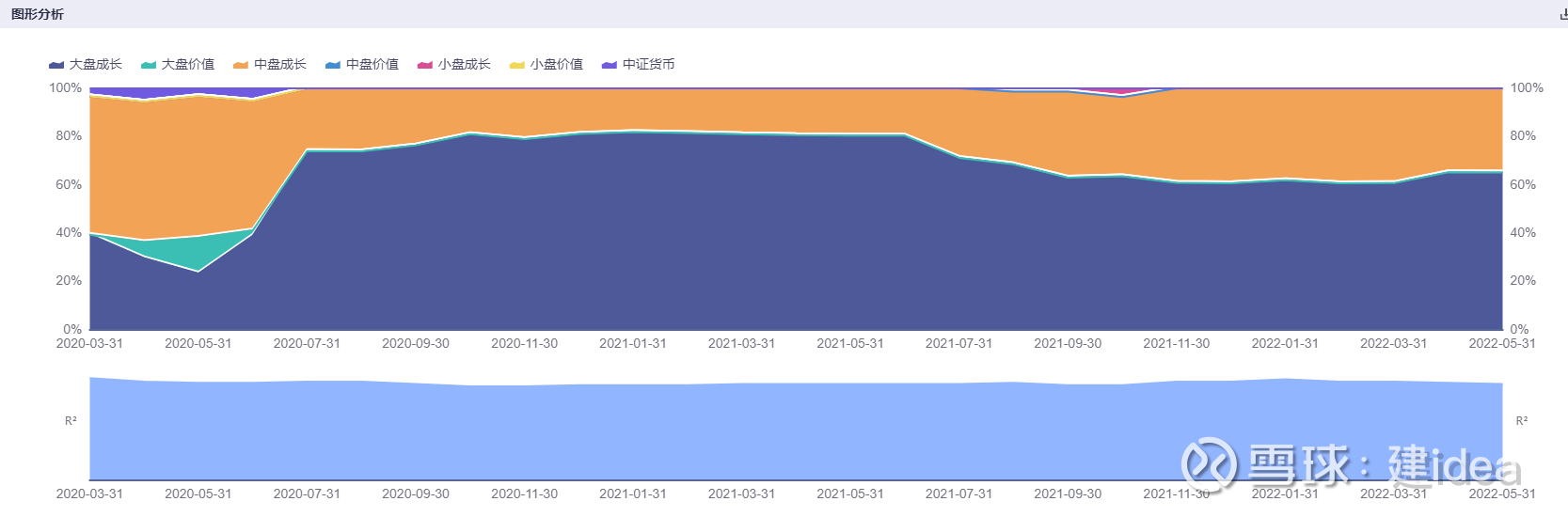

Heavy holding stocks will be adjusted at different investment stages.

For example, in the first quarter of 2021, the top three heavyweight stocks are Sailun Tire, Wuliangye, and LONGi Green Energy. Sailun Tire in the second quarter, Ningde Times, Luzhou Laojiao, Jereh Group, Haid, Luzhou Laojiao in the third quarter, Wuliangye, Yanghe, and Luzhou Laojiao in the fourth quarter, Yanghe in the first quarter of 2022, Luzhou Laojiao, Wuliangye.

Through the changes and changes in these heavily held stocks, it can be seen that fund managers are more inclined to companies with reasonable or low valuations, but with certain growth potential. For example, in the first quarter of 2022, after the rapid market decline, the liquor industry obviously has more reasonable valuations and investment opportunities than before.

The main layout prefers large-cap growth and mid-cap growth stocks.

Since its establishment, the investment target style has mainly focused on growth stocks, about 60% of large-cap growth stocks and 40% of mid-cap growth stocks. This style may, on the one hand, be consistent with the style of listed companies in the consumer industry. After all, leading companies in the consumer industry have obvious competitive advantages, and companies with large market capitalization still have industry-leading growth.

Attribution analysis of investment performance

It can be found from the CSI 300 table that the excess return contribution of the fund mainly comes from the industry and weight. In terms of industries, long-held food and beverages, electronics, power equipment, automobiles, and mechanical equipment all contributed to excess returns, of which food and beverages accounted for the main contribution. In terms of weight allocation, it is mainly through the over-allocation of these five aspects that more benefits are obtained. The conclusion is that the fund manager chose the right industry and took a position, so it outperformed the CSI 300 index by a large margin.

investment philosophy

In an interview, Chang Yuan, manager of Yongying Consumer Fund, said that making the performance of net worth more in line with human nature. In professional terms, what we pursue is not the maximization of investment returns, but the maximization of risk-adjusted returns, which is the goal that professional institutional investors should pursue. In fact, in David Swenson’s “The Road to Innovation for Institutional Investors”, it has already been made more clear. The net worth curve we hope to make has better risk-reward ratio characteristics. A relatively smooth curve will be more in line with the human nature of most people. There is no shortage of investors who pursue high volatility and flexibility in this market, but the products we hope to make meet the requirements of most people.

The above statement can be fully verified from the performance of the product since its establishment, the investment style of the fund manager, and the attribution of performance. Since 2019, investment opportunities in the consumer industry have emerged one after another. The market prefers new consumption and high-certainty fields, giving a huge valuation premium and high investment risks. In such an investment environment, it is very rare to be able to adhere to one’s own philosophy and perform well in multiple dimensions such as stability, aggressiveness, risk control, and excess returns.

hold experience

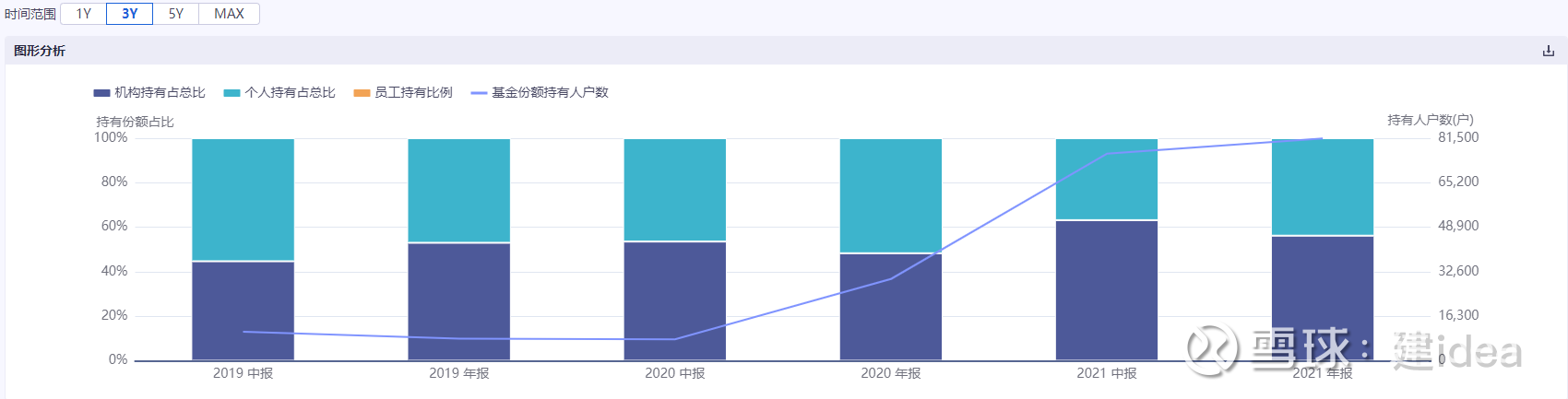

Since the 2019 interim report, the product scale has continued to increase, from 200 million to 1.6 billion, with a maximum of 3.5 billion. During this process, the number of holders has also increased significantly, but we have seen that the structure of holders has not changed much. Basically, 50%-60% of institutional holdings and 50%-40% of individual investors hold positions. Overall, the holder structure is relatively stable, and long-term investors will still feel relatively stable in combination with the net value of the product and the drawdown. $Yong Win Consumer Theme A$

This topic has 0 discussions in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/7808414143/223555129

This site is for inclusion only, and the copyright belongs to the original author.