One of the classic investment theory analysis series: discount rate

1/6. Is the investment experience reliable?

Many investors know an experience. The period of rising interest rates kills valuations, which is especially unfavorable for growth stocks, and has relatively little impact on value stocks, while periods of falling interest rates are the opposite.

As a result, some readers asked: Now that the United States is raising interest rates and my country’s interest rates are falling, is that good for the growth stocks of A-shares, or is it good for value stocks?

This question is a good question. The so-called investment veteran means that he has accumulated a lot of similar experience. For example, this experience may help you recognize the style of this year at the beginning of the year.

However, the difference between an investment veteran and an investment expert is that if you know what it is, you must know why, otherwise, you will not know what will happen to the result of “the United States raises interest rates and China reduces interest rates”?

Stock prices are traded by investors, not defined by investment theory. Theory is just a summary of some investment laws, and these summaries have a premise – either the macro background or the applicability.

For example, in my previous article “The investment experience of successful people is unreliable “, I pointed out that “high ROE is not necessarily a good company” and “judging reasonable valuation with PEG=1 is just a historical phenomenon”, which are all applicable to some famous investment theories. analysis.

From this article, I would like to start a new series of applicability analysis of theories, methodologies, or empirical data that have been propagated in the investment community for a long time.

And “the United States raises interest rates, China cuts interest rates, whoever listens to A shares” is a meaningful opening.

Edit switch to center

Add image comments, no more than 140 words (optional)

2/6, can not only know the theoretical model of the discount rate

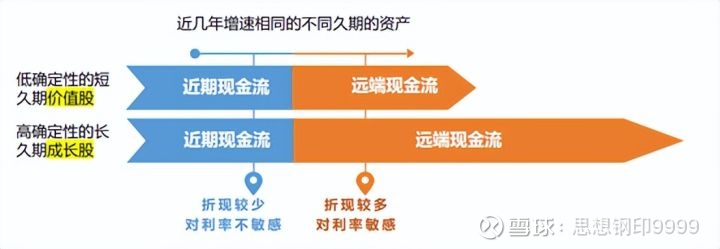

In my article “2022, Seven “cheap” going to Tianshan, I analyzed the impact of interest rate changes on assets of different durations:

If the future of a company is divided into two stages: near-end (within 3 years) and mid-end and far-end (more than 3 years), the reasonable valuation of this company is determined by the discount of “near-end cash flow” and “far-end cash flow”. The discounted cash flow” consists of two parts.

Suppose there are two companies with the same growth rate within three years. Since Company B’s business model and industry space are better than Company A’s, its remote growth rate is also faster than that of Company A, and its duration is also longer than that of Company A. The far-end valuation is also higher than that of Company A. The composition of their reasonable valuation is as follows:

Edit switch to center

Add image comments, no more than 140 words (optional)

Because the closer the cash flow is, the less affected the discount rate change is, and the more distant assets are more affected by the discount rate change. As a result, growth stocks with a large proportion of remote cash flow are more sensitive to changes in interest rates. When the discount rate increases, the valuation difference between the two assets becomes smaller, and when the discount rate decreases, the valuation difference between the two assets becomes larger.

This is the source of the theory that rising interest rates are bad for growth stocks.

But this is a theoretical explanation. In actual investment, few investors will pay attention to the interest rate to buy and sell stocks. Many people only know this relationship after speculating in stocks for several years. When the fundamentals can’t find the reason, the reason for the interest rate is found.

The same is true for researchers. Those who have done valuation DCF models have an experience, that is, first build a financial model to estimate future cash flow, then estimate a reasonable valuation higher than the current market value, and finally calculate a reasonable discount. Rate.

The index is the synthesis of all stock prices, and the index is only directly related to the stock price of individual stocks, so again, the stock price is traded by investors, not calculated by investment theoretical models.

And what is the mechanism by which interest rates usually affect stock prices? Further dismantling of the “discount rate” is required.

3/6, Quantity and Price

The “discount rate” in the DCF model consists of two factors: the risk-free interest rate + the company’s risk consideration, and the mechanisms that affect the stock price are also different.

The risk-free rate

For institutional investors, the risk-free interest rate can be replaced by short-term or long-term treasury bond interest rates. For retail investors, the risk-free interest rate is the income of bank wealth management products, which are all affected by the benchmark interest rate.

As mentioned earlier, investors are not sensitive to changes in interest rates and will not be directly used for pricing. Interest rates mainly affect the allocation of major assets of institutions, affect the willingness of retail investors to enter the market, and affect the “liquidity” of the stock market – interest rates As a result, less money entered the stock market, most companies’ stock prices fell, and the index fell.

2. Risk consideration

The classic pricing theory holds that the risk of an asset relative to government bonds will ultimately be reflected in the transaction price, which is also part of the discount rate. Therefore, Maotai’s risk consideration is low and its valuation is high, while general companies are the opposite.

In actual investment, investors cannot perceive the risk-free interest rate, but they are really worried about the factors of risk consideration.

The period of rising interest rates is generally the high point of corporate profits, but there are always some investors who feel the tightening of monetary policy and the slowing down of the pace of expansion by corporate operators, so they are more cautious in evaluating future growth, resulting in The decline in risk appetite is the leading force in the decline of stock prices.

Risk consideration is a bigger and more direct factor. Those investors and industry researchers who have been tracking companies for a long time are far more sensitive to changes in the margins of business operations than to interest rates.

To sum up, the discount rate affects the stock price of two factors:

One is “quantity”, and the risk-free interest rate affects the liquidity of the stock market through the allocation of major types of assets;

One is “price”, and the risk consideration affects the pricing of specific individual stocks through risk appetite.

Under normal circumstances, volume and price go in the same direction, but in the special environment of different interest rate directions in China and the United States, they go in the opposite direction. This is the key to understanding the question at the beginning.

4/6, the Chinese side quantifies, the US side sets the price

The impact of different interest rate directions still needs to be understood in terms of both volume and price.

First, from the perspective of liquidity

The answer is simple – the domestic rate cut cycle is the dominant factor.

A-shares are a closed financial market. The interest rate hike in the United States only affects the flow of foreign capital, so the liquidity of A-shares is mainly affected by domestic monetary policy.

Second, from the perspective of risk appetite

The answer is more complicated. The impact of the U.S. interest rate hike cycle on A shares is greater than we thought. There are three main points.

1. As the core link of the global supply chain in China, most companies are more or less affected by overseas demand. The United States has entered a cycle of interest rate hikes, which will eventually affect the investment preferences of most companies and the risk preferences of most investors. The level of optimism in most research institutions.

2. The interest rate hike in the United States has limited the room for domestic monetary policy to play , leading to discounts on investors’ easing expectations in the future.

3. The valuation system is affected by the valuation of U.S. stocks. The white horse stocks that foreign investors prefer are especially obvious, and the white horse stocks have a greater impact on the index.

Therefore, the conclusion is that the opposite interest rate cycles between China and the United States have different effects. The domestic interest rate cut increases the liquidity of A shares, and the US interest rate hike leads to a decline in the risk appetite of A shares.

A typical impact is the bull market in the convertible bond market, because convertible bonds are small in size and more sensitive to liquidity, and their debt nature makes them less sensitive to risk appetite than A shares.

The two opposing influences are not simply hedging, but the market has different dominant factors in different positions:

Before 4.27, the huge liquidity brought about by interest rate cuts was eyeing on the periphery of the stock market, but due to the decline in risk appetite, they were reluctant to enter the market. Risk was the dominant factor . The point emphasized in the article: When liquidity increases, the stock market does not necessarily rise, and the risk appetite declines, and the stock market must fall.

After 4.27, when it fell below the extremely low level of 3000 points, most of the macro risk factors have been exposed, and the funds that should be liquidated have also been liquidated . There is no room for the decline in risk appetite, and the previously released liquidity factors began to dominate. , leading to a strong rebound in the market.

The reversal of interest rates between China and the United States, in addition to the dislocation of action points and action time, also brings complex plate effects, and it is no longer as simple as “good for value, not good for growth”.

5/6, high growth, or high prosperity?

As mentioned earlier, the particularity of this round of interest rate environment is that risk-free interest rates are falling (affected by the domestic loose money and credit policy) + risk appetite is falling (affected by the United States entering the interest rate hike cycle), another important phenomenon is the value of The rise of stocks.

In a normal interest rate hike cycle, the value style is only relatively resistant to falling, but with loose liquidity, the value style has risen sharply. The most typical sector effect is the continued strength of coal. This is the only sector that kept leading the market before and after 4.27. .

As mentioned earlier, growth stocks are suppressed in the interest rate hike cycle because growth stocks are generally long-term assets, and value stocks are generally short-term assets.

But note the word “generally”.

There is a type of growth stocks that have high industry growth in the past two or three years and future industry sustainability in a special period, with high near-end cash flow and far-end cash flow, that is, high-prosperity growth. share.

Growth/value and prosperity are not a dimensional concept. Take the current example:

Condiments – a low-boom growing industry

Oil – a highly prosperous value industry

Steel – a low-prosperity value industry

Photovoltaic – a growing industry with high prosperity

Therefore, in the stage of rising risk-free interest rates, value stocks do not all rise, but enter the “prosperity pricing model”, that is, on the basis of reasonable valuation, the ups and downs are directly determined by the marginal changes in the prosperity , that is, the investment in the Another experience: “The bull market looks at the pattern, and the bear market looks at the performance” .

A “high-prosperity growth industry” such as photovoltaics, which has both a pattern and a performance, is not guaranteed to make a profit. When the liquidity factor is suppressed and the risk appetite declines, it will also be regarded as a growth stock to kill the valuation; Only when the risk appetite no longer declines and the liquidity factor dominates, does it enter the stage of prosperity pricing —the stock price is given a reasonable valuation, and the subsequent rise and fall is directly determined by the marginal change in the prosperity.

Therefore, before 4.27, the photovoltaic sector killed the discounted cash flow at the far end; now, it is the high growth of the near-end cash flow – not contradictory.

On the contrary, semiconductors are obviously at a high point of prosperity, and most categories are expected to enter a downward inflection point, so the rebound stage is just following the flow.

However, global macro policies affect each other. The current ” US interest rate hike cycle + China interest rate cut cycle” is only a short-term dislocation caused by the disturbance of the epidemic . The interest rate hike in the United States has left A shares with no room for continued interest rate cuts.

Therefore, the current plate effect is only temporary, and huge changes may occur in the second half of the year . To analyze such changes, we must understand from the perspective of the cyclical characteristics of interest rates. ” read in.

6/6. A good investor is like a good doctor

For the theory in investing, many people have two extreme views, and some people never believe these “nonsense”. Others put all phenomena into a theoretical framework.

I remember a doctor friend said that it would be nice if every patient was sick as in medical textbooks.

The theory in investment is like the symptoms of illness in medical textbooks, “1, 2, 3, 4…” is clear, and the phenomenon in actual combat is like the symptoms of a patient can never be combined, and often several diseases are together. .

To make matters worse, investment theory is not yet a pathological theory, but more like a psychological theory, a possible explanation for a phenomenon.

Therefore, a good investor is like a good doctor. He does not pursue medicine to cure the disease. Healing is the means, and saving people is the goal.

There are 12 discussions on this topic in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/9277793488/223044071

This site is for inclusion only, and the copyright belongs to the original author.