Life is a practice, and so is financial management. The transformation of bulls and bears has its own destiny, which is beyond the decision of us mortals. We are eager to inflection points and bottoms. In hindsight, it is mostly a waste of effort. How many heroes and celebrities are allowed to compete in the market. “Bending down”, it is better to do a good job of dealing with it, and make the things that you can decide to the extreme, which is the foundation. This article is for those who are still holding on in a bear market, those who have raised their hands in surrender, and those who are ready to enter the market.

I have been obsessed with using data and code to objectively analyze and mine some valuable things, and hope to give you some reference. When I turned it from an idea in my head into a reality, I was still surprised! In a word, it is very beautiful and harmonious! I hope that when the market is not good and confused, it can cause some thinking in another dimension, it is worth it!

what is this?

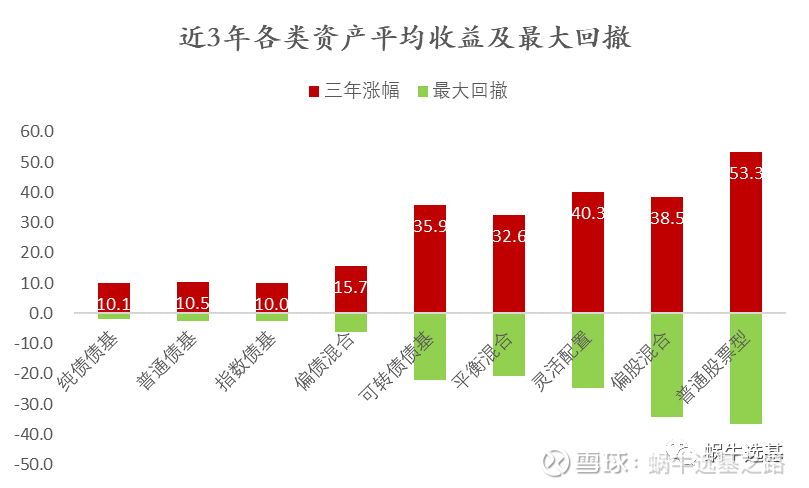

To be precise, this is a map of the broad categories of public funds in the whole market. Its core function is to let us clearly and accurately recognize the classification of public funds for the first time , and the long-term and short-term returns and risk profiles in an average sense, especially In terms of risk, we need to be clear about what kind of adverse changes will happen to the fund assets in our hands under extreme circumstances, and can we bear it? What is the maximum drawdown for an equity fund? How much is the debt base? For our wealth to grow steadily and our bodies to be healthy and long-lived, we must have a full understanding of the “nutrients” and “calorie” of various ingredients. Who makes us live in such an increasingly sophisticated world?

If you don’t understand or grasp the essence of financial management, buy after the hot spots, buy for high yields, think about buying at the bottom, buy a lot at a time, and only think about making quick money in the short term, the side effects are still obvious, especially when the market fluctuates more. When you are older, it is easy to lead to “fund emotional disorders” such as “indigestion, bad temper, mood swings”, etc. These situations are very common in Tieba. Ups and downs, many people buy dozens of funds without knowing the actual risk of their overall positions.

I believe that after figuring out the connotation of the above chart, most of the above problems should be solved.

What’s the point of life?

Without it, the risks and benefits are absolutely equal!

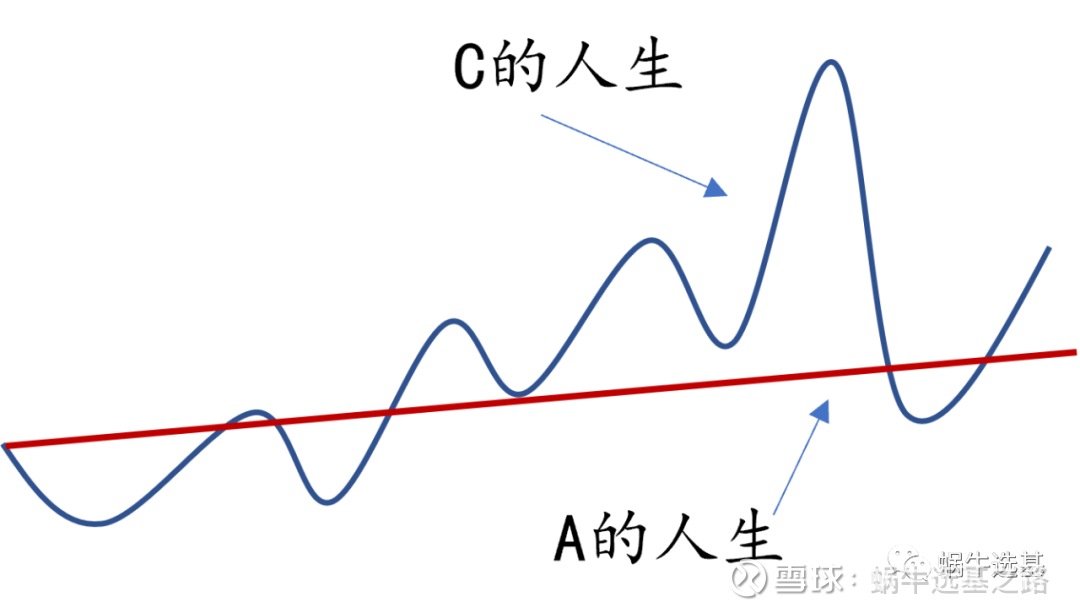

If you want to achieve a magnificent life, you must be able to withstand the baptism of strong winds and waves. The debt base seeks stability, and the stock base is tossing. The yield of the debt base in the past three years is only about 10 points, and the stock base is 40-50 points. , watching the latter is more brilliant (this is nothing, higher at the peak), but then let you bear a -30%-50% decline, many people tend to raise their hands and surrender at the bottom of the valley, and experience the bright moment, In the end, it fell miserably to the bottom of the valley. This is the last thing we want to see. In other words, an ordinary, meaningful and valuable life, even if it is ordinary, is there anything wrong?

Before buying a fund, we should learn “fortune-telling” for ourselves, see what we lack in the five elements, and carefully look at the maximum drawdown of various funds in the table above. In terms of configuration, my honey, other arsenic, and millet porridge may be better than abalone and sea cucumber.

Several alternatives can be made:

A 100% pure debt

B 80% pure debt + 20% partial debt mixed

C 70% pure debt + 20% partial debt mixed + 10% convertible debt

D 60% pure debt + 40% common stock fund

Needless to say, plan C is a more aggressive and fluctuating life than plan A, which involves crying and laughing, ups and downs, such as this:

However, before the D plan, the C plan is still pediatrics. We can compare the C and D schemes in this way.

Comparing the table at the beginning of the article, let’s talk about income first,

Plan C

=70%*10.1+20%*15.7+10%*35.9= 13.8%

Plan D=60%*10.1+40%*53.3= 27.38%

Including stocks is not the same, earning more, the income of D plan is twice that of C plan, which is really enviable, let’s take a look at the maximum drawdown during the holding period:

Plan C

=70%*(-2)+20%*(-6.3)+10%*(-21.9)= -4.85%

Scheme D=60%*(-2)+40%*(-36.59)= -15.96%

Obviously, the D plan is more volatile than the C plan, and the maximum decline is 3 times that of the latter. When choosing between the two plans, you must seriously consider how much you have, and you can’t only focus on high returns. Otherwise, the tragedy has quietly planted the seeds.

So, when, or in what life scenario, can the D plan be configured? First, there is still enough time in life, second, a stable source of income, third, optimistic and positive, strong psychological endurance.

Writing here, I remembered the last sentence Mingyue said in “Things in the Ming Dynasty”, which roughly means, don’t envy princes and nobles, there is no standard of success in life, the best success may be according to the one that suits you. Way, live this life indifferently, what can you do to be an ordinary person? The tragic end of Zhang Juzheng, the most important minister of the Ming Dynasty, could not be clearer.

ABCD four options, or in other words, four kinds of life, or plain, or steady, or aggressive, there is no right or wrong, only suitable or not, it is meaningless to envy the brilliance of others, work hard in your own way, that is The most fulfilling and happy.

How to customize your own configuration plan?

I developed the above process into a calculator, as follows, you can adjust the allocation ratio of each type of asset by yourself to see which plan is more suitable for your life. In this difficult time of the bear market, more rational and valuable Thinking, it will be very helpful for the future life.

This small tool is used for the configuration trial calculation of large-scale assets, which is very convenient.

Some people will say, I know so much, but I still haven’t lived my life well, I haven’t made money, there are thousands of funds in the market, how to choose? Are there funds with better price-performance ratios for each major asset class?

This is the content that follows. You can’t eat a fat man in one bite. Let me analyze it for you slowly. Next time, I will talk about pure debt.

It’s not easy to be original. If you like it, like it, and it’s best to share it with forwarding. If you forward it, give me a screenshot too, so that I can feel your support. At some point, there will be surprises.

This topic has 0 discussions in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/9469509062/231076126

This site is for inclusion only, and the copyright belongs to the original author.