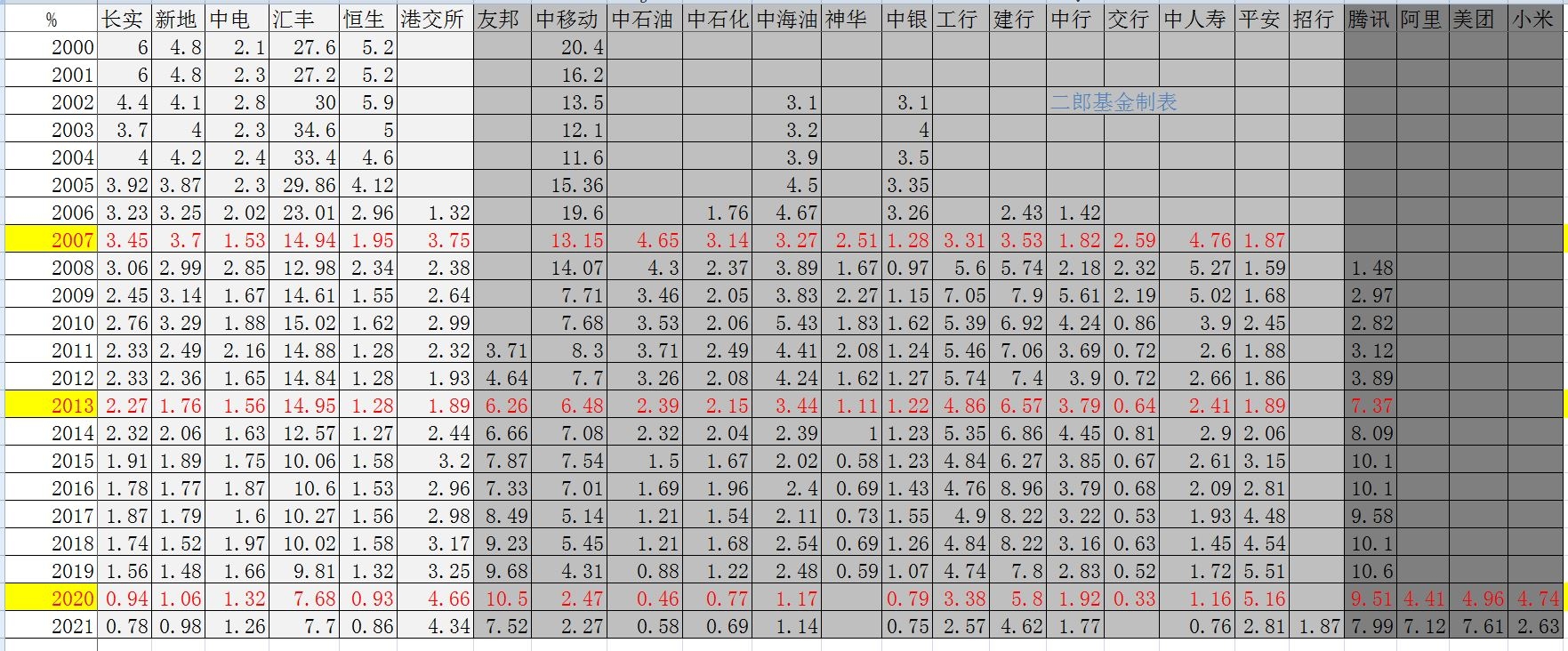

Recently, I have sorted out the changes of important heavyweight stocks in the Hang Seng Index since 2000. It is very interesting, and maybe I can find some investment opportunities from it. In the past 22 years, all kinds of heavyweight stocks have appeared, and each has its own role. Since I could not find the changes in the heavyweight stocks of the Hang Seng Index, I deliberately read the annual reports of Tracker Fund since 2000, and sorted out the data based on the shareholding ratio disclosed in the annual reports. Tracker Fund is a fund that follows the Hang Seng Index, so this deviation will be relatively small and the degree of certainty will be relatively high.

We divide the main heavyweights into three categories: imperial grandsons, nobles and beggars. The grandson category mainly refers to companies that have been rooted in Hong Kong for a long time and are of great significance to the local economy of Hong Kong and the historical development of Hong Kong. The sample selected Cheung Kong Holdings 00001, Sun Hung Kai Properties 00016, CLP Holdings 00002, Hong Kong Stock Exchange 00388, HSBC Holdings 00005 , Hang Seng Bank 00011. Aristocratic stocks mainly refer to central SOEs that have made great contributions to China’s national economy, have stable profits and stable dividends. The sample selected ICBC 01398, China Construction Bank 00939, Bank of China 03988, Bank of China Hong Kong 02388, Bank of Communications 03328, China Merchants Bank 03968, China Shenhua 01088 , PetroChina 00857, Sinopec 00386, CNOOC 00883, China Mobile 00941, China Life 02628; also include some individual private or foreign companies, such as China Ping An 02318, AIA 01299. Beggar gangs mainly refer to some so-called new economic companies. These companies basically do not have stable profits or dividends, and the returns to investors are unstable. They mainly rely on burning money to cut leeks for a living. The samples selected Tencent Holdings 00700, Alibaba 09988, US Group takeaway 03690, Xiaomi Group 01810.

The evolution of the heavyweight class since 2000, we find that it can be divided into four stages.

The first stage is the Emperor Sun Tianxia (2000-2006). This stage is basically the world of the emperor’s grandson, and the nobles are temporarily showing their prominence. HSBC Holdings has maintained a weight of around 20-30% for a long time, with a group of younger brothers Hang Seng Bank, etc., and has long dominated the pricing power of the Hang Seng Index. At this time, the nobles have a single seedling China Mobile, and the weight is not small, it has always been between 10-20%, and there are fluctuations in between. In this period, the Hang Seng Index can be said to be controlled by HSBC Holdings and China Mobile as an accomplice, forming a situation of two swords. The two heavyweight stocks joined forces to lead the Hang Seng Index out of the 1997 financial crisis and the haze after the burst of the Internet bubble in 2000, and regained its upward trend.

The second stage is the rise of the nobility (2007-2012). Due to the successive listing of central enterprises from 2002 to 2008, the shares of state-owned enterprises in the Hong Kong market increased. These state-owned enterprises are China’s core assets with high profits and high dividends. Therefore, in 2007, the Hang Seng Index included many companies on a large scale. PetroChina, Sinopec, CNOOC, China Construction Bank, ICBC, Bank of China, Shenhua, Bank of Communications, China Life, and Ping An were included in the Hang Seng Index in 2006 and 2007. To this end, in 2007, HSBC Holdings, the elder brother of the royal family, was forced to cut its weight by nearly half, giving way to the aristocrats of central enterprises. Until the end of 2019, the central SOEs represented CCB with a high weight of around 8%. In the meantime, China Mobile also began to be forced to downgrade its weight in 2009, giving way to the brothers of other central enterprises. The central enterprise sector contributed to the ups and downs of stock prices in the post-crisis era in 2008 and 2009.

The third stage is internal and external collusion, and the rise of beggar gangs (2013 to 2019). At this time, Tencent Holdings, the leader of the beggar gang, was born. In 2013, the weight was suddenly doubled to 7.37%, and the weight rose all the way to 10.6% in 2019 in the next few years, defeating the grandson and nobles in one fell swoop. They have become the largest heavyweight in the Hang Seng Index. On the other side, AIA of the US Empire has also increased its weight all the way at this time. In contrast, the aristocratic group has been eclipsed, and central enterprises such as China Mobile have been downgraded. The biggest victim is China Mobile. In 2019, under the blow of the US imperialist delisting, the stock price plummeted, and the weight also plummeted. The leader of the beggar gang, Tencent, with the cooperation of American Empire AIA, took advantage of the opportunity of Hong Kong Stock Connect to promote the Hang Seng Index to rise steadily during this period (although there was a stock market crash in the middle).

The fourth stage is to worship foreigners and fascinate foreigners, and beggars help the world (from 2020 to the present). In 2020, the beggar gang leader Tencent Holdings led a group of beggar gang brothers to fully occupy the heavyweight stocks of the Hang Seng Index. In addition to Tencent’s 9.51% weight, Ali, Meituan, and Xiaomi exceeded 4% of the weight as soon as they came up, and the four beggar weights The total has exceeded 24%. You must know that two of these four companies are not profitable for a long time, three are not paying dividends for a long time, and only one is occasionally donating a few cents every year for everyone to buy snacks. American Empire’s AIA Holdings also has a 10% weight in 2020. As for the representative of the aristocratic group, the weight of China Mobile has been reduced to about 2%, which is negligible; Shenhua was even expelled from the game; the weight of three barrels of oil is even more negligible, and the aristocratic group has suffered an unprecedented blow. In 2021, with the dismissal of Bank of Communications, it will reach a freezing point. The weight of the US Emperor AIA Holdings and the four beggars is close to 40%, and even the former representative of the imperial grandson of HSBC Holdings has only about 7% of the weight. Internal and external collusion, the beggar gang brothers won an overall victory. Unfortunately, the Hang Seng Index, led by the beggar gang, has fallen horribly in the past two years.

From the above four stages, we can probably see several problems:

First, the adjustment of heavyweight stocks in the Hang Seng Index is developed in response to market changes. The 2002-2008 listing tide of central enterprises created the conditions for central enterprises to be included in the Hang Seng Index. In 2013, the Hong Kong Stock Connect is ready to open. Tencent Holdings, as an Internet industry company that is missing in the cancer stock market, will surely be highly sought after by mainland funds after the opening. Beginning in 2019, a large number of non-profit new economy companies have been listed in Hong Kong stocks, creating the Hang Seng Index among the four beggars of the Beggar Gang. Therefore, on the surface, every major exchange of heavyweight stocks is a response to the market by the Hong Kong Stock Exchange.

Second, is it really beneficial to be included in the heavyweight stocks? the answer is negative! In 2007, the central enterprise group was included in the Hang Seng Index and dominated the list. The direct result was the 2008 financial crisis, and the major central enterprise stocks were almost included in the index at a high level. Also in 2020, when the four major beggars dominated the Hang Seng Index, it was precisely the high point of the stock prices of these companies. On the contrary, China Mobile, which was downgraded again in 2020, China Shenhua, which was expelled in 2020, and Bank of Communications, which was expelled in 2021, saw their stock prices bottomed out and walked out of Slow Bull soon.

Third, index funds frequently take over at high levels, conspiracy or conspiracy? I can’t draw conclusions on this one, but there are a few details worth thinking about. 1) From 2002 to 2007, there was a wave of central SOEs going public. Many foreign capitals (mainly U.S. imperialists) were important strategic investors during or before the IPO. In the bull market environment, by the way, a package of central enterprises is directly thrown into the Hang Seng Index, and many of them are not low in weight, and then everyone knows. 2) In 2020, China Mobile was hit by the US imperialists, and it directly halved its weight from more than 4%, which was not high, and used this to severely suppress the stock price. 3) From 2020 to 2021, when the stock price of Internet companies has risen sharply, the weight of the four beggars will be increased by a large proportion. And the major shareholders behind the four beggars are foreign capital, and everyone has seen what happened next. Index funds have repeatedly taken over the market at high levels. Is it a conspiracy or a conspiracy?

From the above questions, we may be able to draw some investment suggestions or judge some future trends.

1) Newly included companies or companies with a high proportion of weight will become doomsday sooner or later unless they have sustainable development and long-term reasonable dividend returns (such as HSBC Holdings).

2) For companies that have been expelled or have their weights significantly reduced, if their profits are stable and their dividends are long-term and reasonable, it may be a long-term entry point. Such as China Shenhua and China Mobile in 2020.

3) At present, the aristocratic group of state-owned enterprises has been suppressed for ten years, and there is not much weight left, but these enterprises have stable profits, large net profits and generous dividends, and may be able to regenerate in the next 1-2 years. Both the stock price and the weight may rise sharply; for the beggar gang group, because there is no continuous profit and dividend, the stock price is inflated and the weight is heavy, and the stock price and weight will face huge downward pressure in the future.

Therefore, blessings and misfortunes depend on, and misfortunes depend on fortunes. Dominating the list is not a good thing, and being fired is not a bad thing. All things in heaven and earth, again and again. Next year, the environment that has suppressed central SOEs for ten years may change.

This topic has 10 discussions in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/8164125924/231453433

This site is for inclusion only, and the copyright belongs to the original author.