This time, we investigated the 50GW new silicon wafer factory newly built by TCL Zhonghuan in Yinchuan, and the overall degree of automation is very high. Due to confidentiality reasons, the use of mobile phones is prohibited in the internal facilities and during the tour.

one. Factory tour

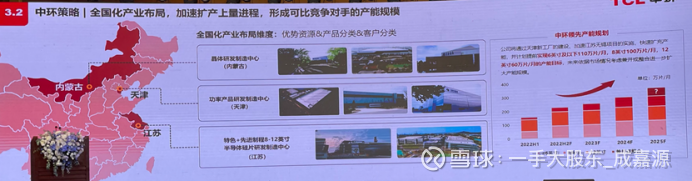

Ningxia Zhonghuan Photovoltaic Materials Co., Ltd. is one of the key projects invested by Tianjin Zhonghuan Semiconductor Co., Ltd. in the country. The total investment of the project is 15 billion yuan. The project is positioned as the world’s leading monocrystalline silicon smart factory and green factory. It is the world’s largest solar monocrystalline silicon material project. After the project is completed, it can have mature G12 solar-grade crystal pulling and silicon wafer cutting technology, which can better meet the needs of the photovoltaic market in the future for new energy materials with “higher conversion efficiency, higher manufacturing efficiency, customized production lines, To meet the needs of “flexible manufacturing”, give full play to the scale advantage and cost advantage in the competition of the new energy material industry, increase the global market share, and consolidate the competitiveness of Zhonghuan Semiconductor in the new energy material industry.

On February 1, 2021, the 50GW (G12) solar-grade monocrystalline silicon material smart factory project of Ningxia Zhonghuan Photovoltaic Materials Company was officially signed in Ningxia. Construction started on March 18 of that year. It only took 56 days from the signing of the contract to the start of construction. In December of that year, the company’s first batch of single crystal furnaces was put into production, achieving the goal of starting and putting into production that year. The project is divided into 4 crystal pulling modules and 2 square cutting modules. The first module of crystal pulling has all the production capacity, the second module has been installed vertically on June 15, the third module is expected to start vertical installation in September, and the fourth module is expected to start vertical installation in November. The 50GW monocrystalline production capacity is expected to be put into production before the end of the year, and through technological upgrading, the actual annual production capacity of the project will reach more than 65GW.

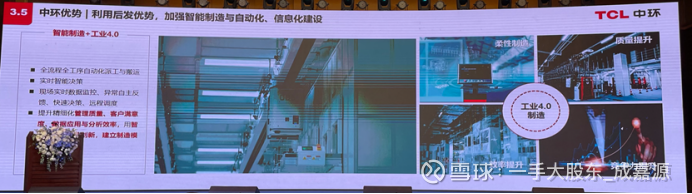

We visited the first crystal pulling module and the first cutting module of the Ningxia Zhonghuan project. The first crystal pulling module has achieved 384 single furnaces, and the comprehensive energy consumption per unit product can be reduced to 22KWH/KG. The operation of the square bar has been unmanned, and the labor is mainly responsible for equipment maintenance and other work. The next step is to target the black light factory. The factory has a high degree of automation, and processes such as material transportation, loading and unloading, and ingot handling have been automated.

two. meeting content

1. Qin Shilong’s interpretation of the company’s mid-year performance

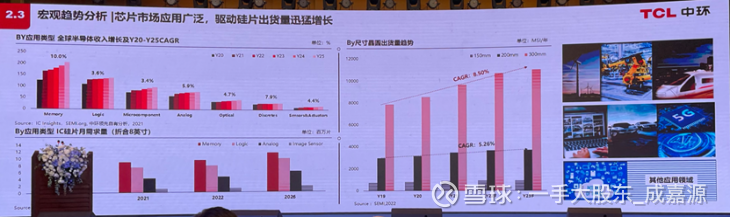

The growth rate of Zhonghuan’s half-year performance is about 80%, and the net profit after deducting non-return to the parent is more than 100%. In the previous 10 years and after the mixed-ownership reform last year, the business operation has maintained a stable state.

From the perspective of the three major business sectors, the shipment volume of photovoltaic materials has increased from 27GW to 34GW. The overall market capacity is increasing, and the market share of Zhonghuan has also increased to 25.3%. Silicon materials were on the upward channel in the first half of the year, but the company did not rely on External factors are profitable, so the quality of earnings is still relatively solid.

The shipment of shingled modules in the first half of the year increased from 1.5GW to 3GW year-on-year, and the market share increased to 3%. As a newcomer to components, the cost of market development is unavoidable. In the first half of the year, the bidding price of Huansheng was lower than that of leading companies. It has a negative impact on company profits. However, in terms of the market, Huansheng has already obtained the white list of central enterprises. In terms of products, shingles are a differentiated product. At present, our focus is to improve the differentiated manufacturing of shingled components, and capacity expansion is not very urgent. We will start to increase production capacity in the third quarter.

In terms of semiconductor materials, revenue in the first half of the year has accounted for 3.4% of the global market share. The company is currently the largest supplier of semiconductor materials in mainland China.

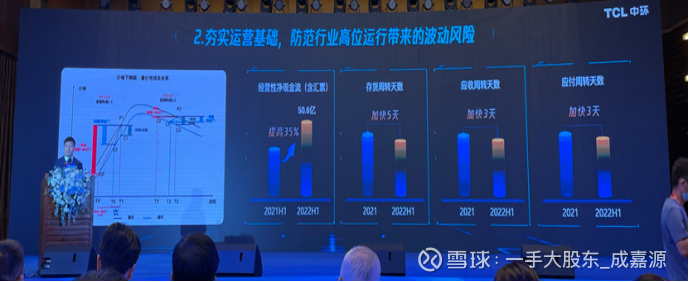

In the first half of 2022, the company’s operating cash flow increased by 35% year-on-year to 5.06 billion yuan, and the inventory turnover, accounts receivable, and accounts payable turnover days were accelerated by 5 days, 3 days, and 3 days, respectively, and operating capabilities were significantly improved. At present, photovoltaics are operating at a high level. To prevent future risks, the company adopts a strategy of high turnover and low inventory.

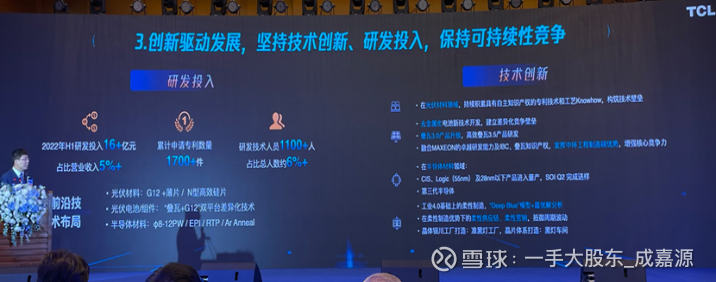

The company attaches great importance to R&D and maintains high-intensity R&D investment in the first half of the year. In 2022H1, the R&D investment amounted to 1.6+ billion yuan, accounting for 5%+ of its revenue. Maintaining a certain amount of R&D investment is a guarantee for the company’s future development.

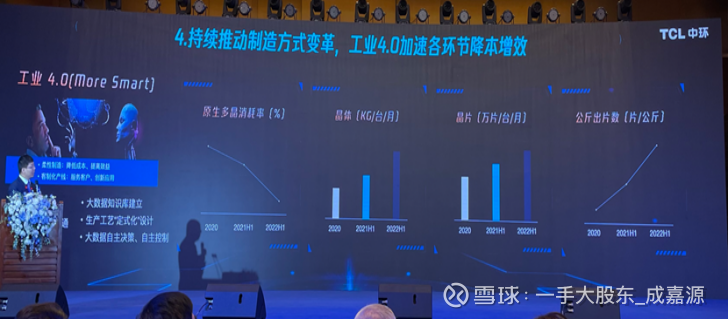

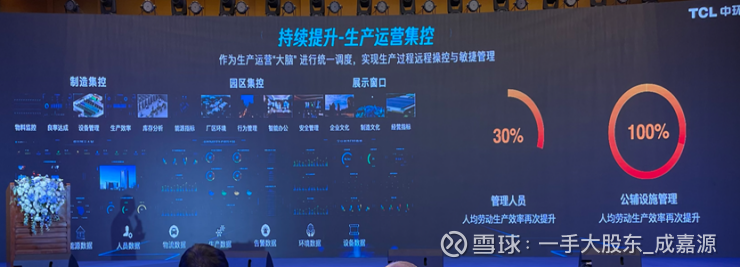

Industry 4.0 promotes the continuous improvement of indicators such as the consumption rate of primary polycrystalline silicon, the monthly output of a single unit, and the number of wafers per kilogram.

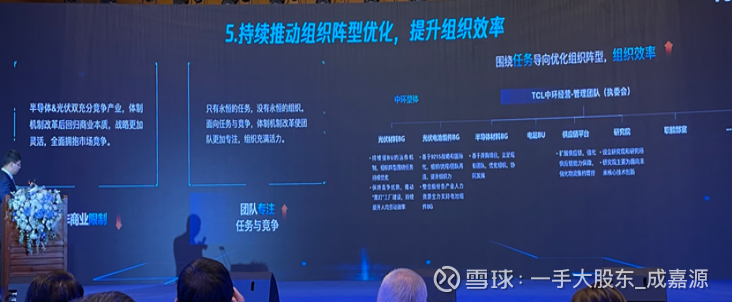

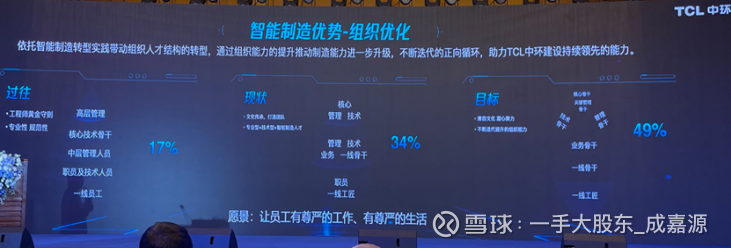

The company has also done a lot of work in the organizational structure after the mixed reform last year, and continued to promote organizational formation and improve organizational efficiency.

2. Shen Haoping, general manager of TCL, talked about the trend, logic and evolution of the photovoltaic industry in “New Photovoltaic Energy Changes the World and Changes the Self of the Practitioners”

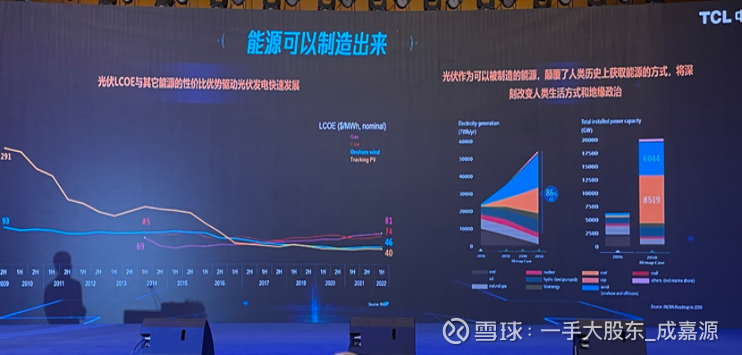

As the price of photovoltaics declines, its cost-effectiveness with other energy sources will continue to emerge. As an energy source that can be manufactured, photovoltaics have subverted the way of obtaining energy in human history, and will profoundly change human lifestyles and geopolitics.

Demand is also increasing with the cost-effectiveness of photovoltaic power generation.

We took advantage of the demographic dividend and the huge tensor of the environment to become a global factory. Looking forward to the new generation of Chinese born after 2000, they will not accept the lifestyle of 20 years ago. We must change the way of manufacturing and learn from the German and Japanese companies of 20 years ago. We need to realize the development of enterprises and the saving of capital under the new environment. In the current international trade environment, we need to understand tariffs. In the context of deglobalization, we have to understand today’s behavior from an individual standpoint.

From the perspective of the relationship between photovoltaic system installers and manufacturers, there is a huge cycle, because it is an energy source, and it depends on the grid, subsidies and the support of the people. In the context of the rapid growth of demand in the photovoltaic industry, it must be accompanied by cycles. The photovoltaic and semiconductor industries share a common physical foundation. The heat of the supply and demand relationship between investors and practitioners is about one to two years, and the government’s industrial policy changes in 2-3 years, including the US restrictions on China that change in half a year to one year. Technological innovation takes three to five years, which objectively strengthens the existence of a certain cycle of the photovoltaic industry in the ecological chain.

Whether the photovoltaic manufacturing industry can achieve lower costs is the core. Our respect for intellectual property rights is a necessary condition, and the selection and deepening of technology paths are the core elements. In terms of manufacturing methods, there have been no new inventions in photovoltaic technology since 2007, but the accumulation of know-how in the process of industrial deepening. After 2000, the change of manufacturing method will be more important than the technical path, because it affects the judgment of ESG of photovoltaic enterprises, as well as the stability of enterprises, and the reliability of product quality. We need to make shareholders understand the new PV manufacturing. On polysilicon, we expect fluidized bed to have a certain share. In the battery, we prefer the IBC path of MAXEON that we have invested in. In the semiconductor, if the 12-inch is still made of precious metals, the mobile phone should not be able to use it now. If photovoltaics use silver all the time, 1000GW cannot be achieved. The increase in line density, combined with changes in metallization, is a very important point for photovoltaic manufacturing outside the technical path in the future.

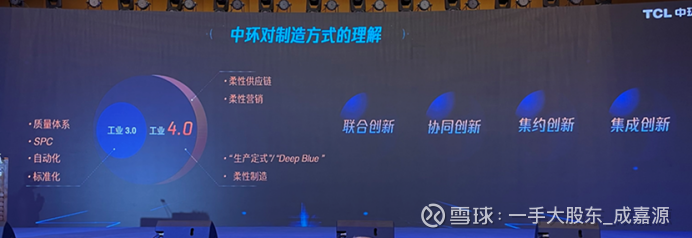

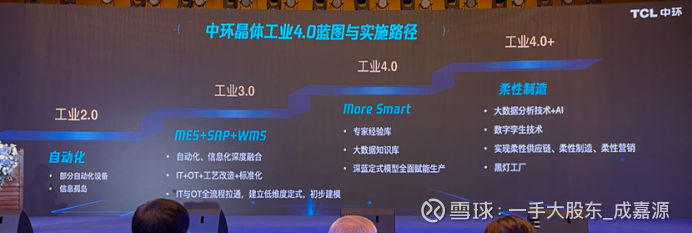

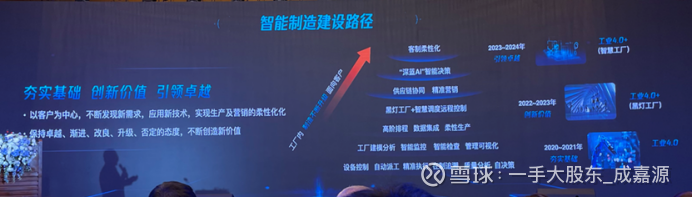

The so-called Industry 1.0 refers to manual labor and stand-alone equipment 100 years ago. Most of China’s industries in the 1950s were, including the semiconductor industry in the 1950s and 1960s. In Industry 2.0, we started to use PLC in large numbers. After the reform and opening up in the 1980s, labor was still used in some relatively large-scale manufacturing. In Industry 3.0, the effects of MES, EAP, and WMS are displayed, and they have obvious advantages in quality tracking and process technology adjustment. Industry 4.0 is based on flexible manufacturing. We consider the polysilicon of factory A and factory B, and we must make a product consistency. We are called Deep Blue internally, and we need deep learning, which may not only be the self-learning of the machine, but the optimal solution obtained by the front-line engineers through the formula.

3. Zhang Haipeng, head of new energy materials BG, talks about photovoltaic market thinking

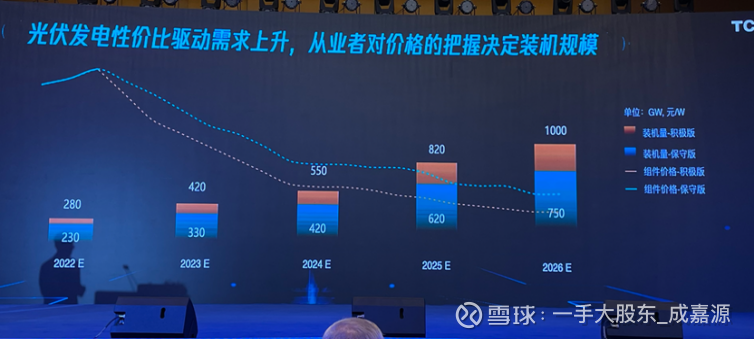

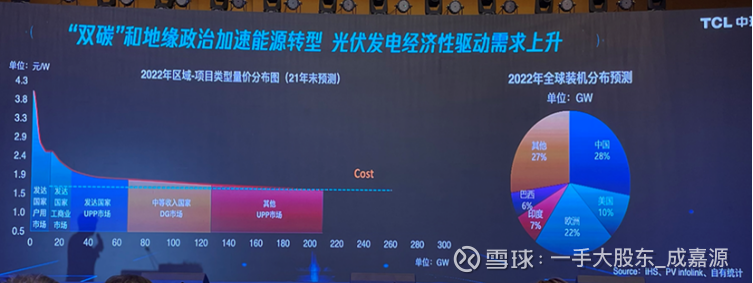

In the expectation at the end of 2021, for the market with high module price acceptance, the blue line is 1.7 yuan/W, which was originally expected to correspond to 220GW of installed capacity.

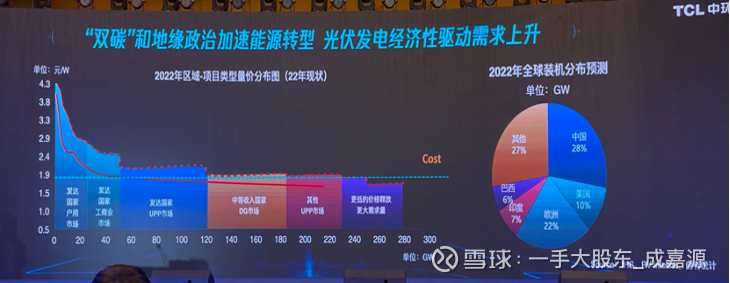

But the actual situation is that the Indian market stocked up in advance in the first quarter, releasing the demand for the whole year in one quarter. At the same time, the growth in Europe this year is also very obvious, and it has raised the price of module ASP. The red dashed line is what is currently seen. The UPP market in developed countries was concluded at 70GW before the high-value range and is currently around 120GW. So the component price has risen from 1.7 to 2 yuan. From the perspective of supply chain output, 270-300GW module output can be achieved, so China and other countries concerned about the IRR project demand still cannot be started. In the future, there will be more demand for ground power stations and more rational prices.

From the perspective of all aspects of the supply chain, the comparison between the supply of silicon material and the single crystal furnace in August is still relatively tight. At the end of the year, the monthly output of silicon material exceeded 110,000 tons, corresponding to an annual production capacity of 400GW, and the demand for single crystal furnaces has already reached an inflection point of supply and demand. If the output is 350GW next year, the silicon material will be 2.3 million tons by the end of next year, corresponding to 600-800GW installed capacity. Under such circumstances, we will definitely see new changes in the expectations of industry practitioners for more demand and the grasp of prices. The pink line is the global quartz sand production and the purple line is the imported sand production. At present, high-purity quartz sand in China is also used in the outer layer of quartz crucibles. If Chinese quartz sand is taken into account, it can meet the single crystal demand of 600-700GW next year. The pink line has a gap for polycrystalline silicon material, which will be newly added by China. Filled with high-purity quartz sand. The proportion of inner sand will drop to 40% next year. Two years ago, Zhonghuan used a collaborative approach, and now it has locked in more than 35% of the global supply of high-purity quartz sand imported from overseas. Zhonghuan can maintain more than 60% of the supply of high-purity quartz sand this year and next year.

Under the circumstance that polysilicon materials are relatively tight, more players use silicon materials to become competitive. Now non-silicon costs only account for 17% of production costs, and non-silicon components account for 59% of costs. But the price of silicon material is gradually returning to rationality. The silicon and non-silicon costs of components, non-silicon costs only account for 59%. After the silicon material returns to rationality in the future, the non-silicon costs of components will exceed 80%. The price of silicon material has risen from 70 to 300, and will also drop from 300 in 1-2 years. Whether it is a silicon wafer or a component manufacturer, if they want to maintain their own business competitiveness for a long time, they should be based on the reduction of their own non-silicon costs. In the future, manufacturers with more advanced manufacturing methods can go through the cycle of silicon material price reduction.

The non-silicon cost of Yinchuan is the lowest in the industry. On the basis of the original non-silicon cost, various parameters should be optimized to increase the monthly production of a single furnace, etc., to reduce the non-silicon cost.

4. The digital director of Gao Runfei New Energy Materials BG Crystal BU explained the prospect of photovoltaic crystal technology

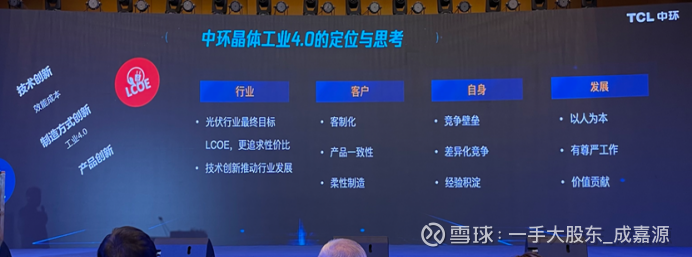

In terms of industry attributes, we have high-tech, asset-heavy, and long-term attributes, and we need to provide customers with customized products. For the customization of customers, we need to use flexible manufacturing methods to meet the customization requirements, which will involve a variety of product structures, as well as more complex product processes, as well as raw and auxiliary materials that match different categories in the production process. How to make these factors effectively achieve a good manufacturing effect, we have achieved flexible manufacturing through years of research and development.

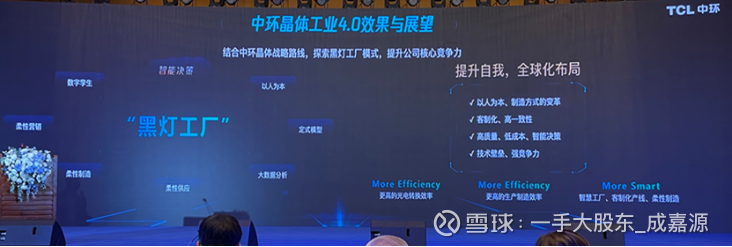

How to form competitive barriers? We have weakened the influence of people on production quality, including that the load-bearing transportation can no longer be carried out by people. Under this model, the output and consistency of our production will be very good, making us cheaper and more competitive. The model of Industry 4.0 is the only way for the development of the industry. From a long-term perspective, to achieve the effect of Industry 4.0, the integration of automation and informatization must be required to achieve a competitive Industry 4.0 model. In the future, we are also exploring the realization of the black light factory.

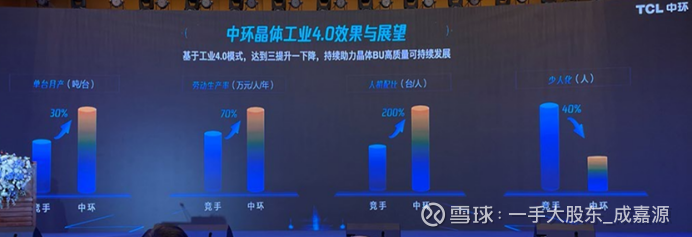

At present, the monthly production of a single unit in Zhonghuan is 30% ahead of its competitors, which can be reflected in the cost reduction, and the labor productivity is also 70% higher than the industry. It can save 1,000 people. According to the annual salary of 150,000 per person, the annual labor cost can be saved by 150 million. The production model is very competitive.

The black light factory model enhances the company’s core competitiveness.

5. Wei Chen, Deputy General Manager of New Energy Materials BG Wafer BU, introduced lean manufacturing, the vane of silicon wafer technology

The current production capacity of wafers is 100GW, in Tianjin, Wuxi, and Hohhot. The follow-up plan is 180GW, of which 170GW is advanced production capacity. In the past, Zhonghuan had several key time points in the slicing process. In 2002, multi-wire cutting technology was introduced. In 2008, diamond wire research and development began. In 2012, the first diamond wire factory was established. Before the establishment of the first factory in 2012, the research on informatization and automation was done. We have developed fully automatic processing equipment, which has also promoted the development of thinning and thinning in the industry.

Chip processing is labor-intensive and high-precision, so we must build a fully automated production line at the production level to replace high-intensity labor and reduce manual intervention.

The Yinchuan factory has been fully automated, and some areas have been blackened. End-to-end integration of production, supply and marketing, as well as quick decision-making and agile management. Through application scenarios, the per capita labor productivity is increased by 200%, and the machine production efficiency is increased by 150%. The black light factory will realize the pilot of the new factory by the end of the year, and the smart factory will be realized by the end of 2024.

6. Semiconductor Industry Report by Wang Yanjun, General Manager of Semiconductor Materials BG

Zhonghuan is a very old company that manufactures semiconductor materials. It started in 1958. We are one of the earliest dry semiconductor materials companies in China. The market economy began in the 1980s, and at that stage we also experienced the helplessness brought about by market shocks. The third stage is the corporate restructuring in 2000. There are problems in the company’s development, and the industry is in a downward cycle. During this period, it is more to accumulate its own culture and make a lot of money.

In the past few decades of development, the proportion of localization centered on manufacturing has reached 40%-50%, and the chip is a relatively weak link. The 14th Five-Year Plan hopes to reach 20%-25% by 2025. Around 2020, we support the manufacture of 40%-50% of the world’s applied products, but the raw materials are only 5%-8%, so it is a very good opportunity for the industry at present.

In the next five years, 12-inch will still maintain a compound annual growth rate of 8.5%.

From the perspective of the pattern, the transfer of the United States to Japan has experienced a relatively large reshuffle, and it will begin to transfer to China after 2020. Each stage represents technological advancement as well as integration. In 2020, the share of international silicon wafer factories will account for 90%, and in 2025, Chinese enterprises will be able to achieve a share of 15%-20%.

We started with 1-inch, 2-inch, and now 12-inch. In the next two years, we will continue to catch up with advanced processes. FZ is a product that opens up the situation of globalization, and it is necessary to catch up with the advanced support below 54nm. This year began to plan more advanced manufacturing such as silicon carbide.

Three, executives face to face

[Mr. Shen]: Everyone is the company’s loyal media reporters. Every time we talk a little bit more openly, we speak freely.

[Question]: Let me ask one first. My surname is Li. I’m from Qingdao. It’s a pleasure to meet you. I admire your professionalism. Many professionals don’t understand it. Have some ideas. The first one is that your competitor can be said to be LONGi, can you talk about that? The second is that this and LONGi can be said to have formed an oligopoly competition ending? Or will more competitors come in or become bigger in this industry? LONGi issued 7 billion convertible bonds for about half a year. Do you have any comments or feelings about his 7 billion trends including some of his industry trends?

[Mr. Shen]: First of all, from the relationship between us and LONGi, we had an excellent relationship before 2010. The three leaders of LONGi and I are all alumni, and I am also Lanzhou University. I graduated a few years earlier than them. Historically, we have The relationship is good, both personal and even corporate. Later, after the capital market opened up, I felt that it was not good to see us online, but we were still good in private, including last year we were doing some things together, and we had very similar views on some cognitions about the industry. As everyone makes silicon wafers, Zhonghuan has the characteristics of Zhonghuan, and LONGi has the characteristics of LONGi. Each of them is trying to make good use of their own strengths and avoid their own weaknesses. It should be understood in this way. In the future, we are still thinking about whether LONGi can become our customer when Zhonghuan makes silicon wafers one day, and if it accidentally does better than LONGi.

This industry is huge. After all, there are not many industries in which China’s capital can be invested in the future. There are two or three relatively clear tracks, such as lithium batteries and photovoltaics, including us. The more certainty is photovoltaics, and there is a lot of room for growth. Some people shout 150G. In today’s report, I am also saying that everyone may view technology too simply, and think that I choose HJT to be technology. I think that or what we are showing today is also an attempt to show everyone that a manufacturing method may be at this stage or at this stage. In the future or 5-6 years or even more than ten years, the manufacturing method will be tracked for half a year, and there will be no new technology path after 2007.

[Question]: The investment of billions of dollars in the manufacturing method is a barrier to capital, right?

[Mr. Shen]: There are no financial barriers, and the manufacturing method is yours to choose. The core of today’s report is that Zhonghuan is talking about Industry 4.0. Regarding the issue of LONGi’s convertible bonds, it seems that this is not the case. In addition, we can honestly say that it is difficult to evaluate the use of his funds. LONGi is a good company.

[Question]: For the first question, I am still more concerned about technology. President Shen also introduced Zhonghuan’s understanding of technology today.

[Mr. Shen]: The words of a family.

[Question]: If we look at this industry from the past, whether it is a larger development opportunity in the industry or an investment opportunity from an investment perspective, it is a typical feature of technology-driven.

[Mr. Shen]: This is the case. The four richest people in China have fallen in front of photovoltaics, and they all stepped on the wrong technical route.

[Question]: From the perspective of our investors, we would like to know whether there will be an epoch-making technology like single crystal that will bring us investment opportunities or industrial development opportunities in the future? It is more likely to appear in the field of components or in the field of silicon wafers or silicon materials, or the field of improvement of the entire process?

[Mr. Shen]: I still want to tell you, I don’t think there will be a chance to go public, and there will be no idea. At the technical level, especially in Chinese companies, someone has a mysterious killer, no, now whether it is in the industry How to say, don’t believe anyone will make super awesome technology, it won’t be like this, super awesome technology is blocked by patents, this is my point of view. There is no new technology after 2007. You may pay more attention to what his engineering capabilities are. It may be more important to evolve a basic technical principle into engineering and into products. Otherwise, the other focuses on battery technology, silicon wafer technology, and more What kind of technology is basically a liar, I will say responsibly, whoever thinks I am wrong can come and file a lawsuit with me. This is indeed the case. The Chinese never dare to say what kind of technology they have made. Technology is all ready-made, just turn it into a craft. If I said what you just said in English, assuming it is called science, there is still a lot of room for technology to be done. It is probably like this, I don’t know what to say. right.

[Question]: I have a second question. You also mentioned Mr. Shen just now. The theme of today’s exchange is to cross the cycle. The silicon wafer field has made the most advanced processes in terms of cost, efficiency and quality. I will deal with the following changes in price reductions or price increases.

[Mr. Shen]: Regardless of price increases or price cuts.

[Question]: But we also see that in today’s industry, among competing companies of silicon wafers, for example, after 30GW is completed, it will issue bonds to make 40GW. It is an upward integration of silicon materials. According to him, there are also From the silicon wafer, I want to extend down to the integration of components. I agree with what Mr. Shen said. This may be the business environment in China. If Zhonghuan chooses neither upward nor downward, does it mean the future? Will the commercialization environment of the photovoltaic industry change? Or how do we understand this problem?

[Mr. Shen]: This is how I look at this matter. Frankly speaking, the logic of this round of integration has nothing to do with companies. People are like this now, but the environment of China’s capital market has also contributed to this environment. The drive of capital is still very heavy. I can’t evaluate the logic of any enterprise integration. I don’t know if you still remember Pence, special Trump’s vice president, there is a speech, he said that China is the most powerful place for state capitalism, Trump said that China is revisionism and so on, this is their envy, jealousy and hatred, but when the general secretary said last year, he should Limiting the disorderly expansion of capitalism, these things destroy China’s industry, these assumptions are all chaos with basic business logic and things that damage the international environment and society, I think China has come this far, especially after 00. In the future, if you think about the dream of 20 years, it will still be a bit wait-and-see or beg for fish. In fact, it is difficult for you to explain it, but it exists, which is probably the case. If you love to fight, you will win, but you may not win. If the four richest people die, there are not many richest people in China. The four richest people are all dead. How can a miracle happen? It’s impossible to pass on my experience, because I’m not a boss, so it’s a bit sour.

[Question]: Hello, Mr. Shen, I would like to ask, in terms of 210, what is the situation of the company’s competitors in this area?

[Mr. Shen]: There are still two, three, three or four companies in the crystal direction of 210. I think they have a gap of at least 24 months with us in the single crystal direction. He didn’t know if he didn’t enter certain doors.

[Question]: Originally made a small size, if it is changed, what is the investment cost?

[Mr. Shen]: It has nothing to do with the investment cost. In other words, if you buy a complete set of equipment in Zhonghuan, you still can’t do it. Of course you can do it, but the yield rate is very low.

[Question]: Another question, I think the TOPCON segment in the industry has been pushed faster this year, and I think the focus of the company is on the IBC segment.

[Mr. Shen]: No, IBC started in Zhonghuan in 2007, and Zhonghuan was trying to become IBC in 2007, so we will not do it in terms of our relationship with SunPower. Now a major company in which Zhonghuan has a stake is doing IBC.

[Question]: Mr. Shen, how do you view the life cycle of TOPCON in terms of technology?

[Mr. Shen]: It has nothing to do with Central, just my personal opinions. Frankly speaking, the reason why TOPCON is up now is that people are more interested in it. It is compatible with existing assets, and it may still be used after changing it. I would like to talk about TOPCON in history. LG has done the best. So far, among all the companies in China, LG has done TOPCON in 2013. The best thing he has done is that TOPCON has achieved 24.7, mass production, probably in 2016. I don’t know if the domestic production has reached this number?

【Guest】: It’s almost the same in China. It’s almost 24.6 and 24.8.

[Mr. Shen]: When the mass production data reaches 24.6, his distribution is very large and wide, which causes a lot of trouble for the components. If you divide the inefficient and efficient electronic chips together, it is equivalent to dividing the used electronic chips. The properties of a one-hour battery and a new battery are the same, and the new battery will be wasted, or it will cause difficulties in the manufacture of components, and the silicon mirror is not good. This is a relatively big problem for TOPCON. The second big problem is in principle. TOPCON is boron expansion, generally at 1050-1100. Depending on the process, it will cause a big problem. The demand for silicon wafers is very high, because so At high temperature, the diffusion time of TOPCON is long, and it is easy to form rings. So far, I know that the proportion of rings in silicon wafers is generally 7% and 8% in China. A company that is close to it may achieve 10%. In the middle ring, we can do it ourselves. To less than 1%, but these all mean the cost, if you want to make rings, the battery will be unlucky. Or 26, but at what price do you do it, how do you do it for one piece and ten thousand pieces, my opinion is this.

[Question]: Last year, I went to Tianjin to attend a conference. The new National Exhibition Center is very large. The roof used seems to be the components of Central Huansheng, which was equivalent to a demonstration project of BIPV. I would like to ask the company whether it will use shingles in the future Components do more BIPV applications?

[Mr. Shen]: To be precise, Huansheng’s module is a product authorized by Maxeon to be used by Huansheng in mainland China. The essence of this product is that it has a huge advantage in anti-masking, especially in urban environments. The general components inside will not be able to generate electricity if you are covered by 1/3, but this is a common phenomenon in the urban environment. Since Huansheng is a parallel circuit, it is said that the ability to resist blocking, anti-shadow and anti-hot spot is very good. Strong, other components are more common in urban environments. If you pull it up, there will be hot spots, and shingled components will generally resist these things. The technology of shingling itself was originally distributed, and Zhonghuan tried to do it. If it is done in China, we believe that the theoretical cost of shingling should be lower than that of traditional modules, so we also try to use it in photovoltaic power plants. , Maxeon has a few interesting products, the first one is Maxeon L, you have to do BIPV is very good, we have shown this product, the thickness of this product is 3% of the existing module thickness, the weight is the existing Component, if I remember correctly, it seems to be 50%.

【Guest】: Because there is no glass.

[Mr. Shen]: There is no glass. I think that the existing technology is more suitable for BIPV besides IBC, but also HIT.

【Guest】: HIT is mainly double-sided.

[Mr. Shen]: Now that we can achieve a relatively high-value roof, in the history of the products with the highest bargaining price, there are usually three companies competing. Later, Panasonic withdrew, LG, SunPower, whether Chinese companies or European companies, are not in the highest price. There is value in it, but his technology is not good.

[Question]: Mr. Shen, hello, senior management, to change the topic, the entire Central Ring has developed very fast in the past two years. From the perspective of management, did you have a great influence and impetus on the development of the company after the mixed reform? This is the first question.

[Mr. Shen]: I will answer your question first, otherwise I may not remember it sometimes. There are three dimensions of rapid development of the company. In the first essence, we call accumulation and development. When the photovoltaic industry was developing rapidly, everyone thought that the development of Zhonghuan was slow. At that time, Zhonghuan was the leader of Zhonghuan, which established Yixing in 2017, with an investment of 3 billion yuan. USD, Mr. Wang’s DreamWorks was at that time. In other words, we concentrated a lot of our energy on it. This is a national strategy. You should do it if you make money or not. Suppose we say that China is not ahead of the Central Ring today. , that is troublesome, this is not self-improvement, it is really troublesome, and many things cannot be done. The second is that we started Industry 4.0 in 2016. We did not expect such a hot market today. We are trying our best to reduce the size of the factory and reduce labor. Our ultimate goal is to reduce the equivalent of 2017 and 2016. 1/8 of the staff, I am going to do this now. We have almost no new investment factories and no competition for production capacity. Obviously, by 2019 and 2020, these projects have basically been completed. It is true that the mixed-ownership reform has played a great role. TCL, as the holding company of Zhonghuan, from everyone’s point of view, has changed its decision-making efficiency and focus, which has played a great role. Objectively speaking, TCL still brings new ideas to Zhonghuan, such as more aggressive policies, such as equity incentives to benefit everyone, which has played a great role. In the past, when we were in the SASAC, he had a very absurd incentive method. My impression was that a salary of 40 million yuan, 80 million yuan, and capped at 200 million yuan. In other words, 200 million and 2 billion enterprises, 10 billion yuan. Enterprise is a concept, but it will happen again. For example, if I made 1 billion, you can grow every year, but over the years you will fall back from 400 million to 200 million. You are not as good as that 80 million, really It is very absurd. Therefore, our business strategy at that time generally guaranteed absolute annual growth. Zhonghuan has always achieved it. This is a way to deal with the assessment method.

[Question]: Mr. Shen, thank you very much. After the mixed reform, the company executives also mentioned that you are more concerned about the business aspect.

[Mr. Shen]: Focus on competition.

[Question]: My understanding of this industry is not very deep, but I generally feel that this industry is capital-intensive, technology-intensive, and labor-intensive. The degree of improvement is very large, and we are also quite shocked. In the next few years, what will the company think will be your biggest difficulties and challenges? Open-ended questions.

[Mr. Shen]: Internationalization, because of your difficulties, people in different quadrants will recognize that they are all in the same industry, but the pursuits are different, and the difficulties are different. We believe that internationalization is the biggest challenge. First of all, you need to make people feel that you are not for money. We say that you need to be culturally confident, to transcend ideology, and to transcend race. Yesterday, when I opened a global board of directors, I also mentioned that the guy who does ESG, I said you are racist and nationalist, you must solve this problem first, don’t think that you sell cheap things and others should be justified Buying is the most common problem for Chinese companies. The second is to respect people’s way of life. When I was in Spain in 2006 and 2007, he said that you are still working on Saturdays and Sundays, which is illegal in Europe. But you use your Saturday and Sunday work to sell products to me. I can’t beat you. The anti-China photovoltaic products are not the first ones that the United States has opposed. As we all know, it was initiated by Europe first, but now Europeans are being beaten. When he got down on the ground, he couldn’t calm down. Europeans are more hateful than Americans. In other words, internationalization is still a challenge in the future. This is the case for all Chinese companies, because what I did Cheap, I sell lighters all over the world. If there is such a concept, there may be a problem, I think.

I am very worried about my 180G, if my internationalization is not good, will China’s production capacity be limited, not to say don’t think it is anti-Xinjiang, you can always be anti-Henan, anti-Tianjin, just a Just saying, the worst thing is countervailing. Zhonghuan has the least government subsidies in the whole industry. Without these government subsidies, Chinese photovoltaic companies can beat others? If you name a leading enterprise, I will tell you how much government subsidy he has, and how many of a leading photovoltaic enterprise violates the “Labor Law” and has a 40-hour work week. You can’t take it for granted. Said, but these principles are easy to understand in our country, but you compete and at the same time turn others over, I really can’t say this, we need the industry to change ourselves, you can’t say that I can make small rules , you are a fool if you don’t foul, you can’t talk like that, that’s how it is.

[Question]: I also asked one by one. When we visited this factory today, I think we were talking about an asset-light model of agency construction, leasing and repurchase.

[Mr. Shen]: That’s what I learned when I first learned, indeed.

[Question]: I don’t know this, can you explain it to us?

[Mr. Shen]: When we were in the era of state-owned enterprises, Zhonghuan never used a penny from the government. In the era of state-owned enterprises, you had to sign a long-term agreement with the government. We are an enterprise led by the State-owned Assets Supervision and Administration Commission. Go in, can I do it? It is very difficult for state-owned enterprises to use these measures. Now this is only done using common methods in the industry. The government provides some kind of support. We speed up investment and do it in a modern way that even surpasses the industry for two or three generations.

[Question]: Second question, I suddenly remembered the internationalization part just now. Is there any connection between your mixed reform and the internationalization part?

[Mr. Shen]: No, we spent a long time with SunPower because he has IBC, and the IBC patent is difficult to break through, and the shingle patent is also his. We tried to do XBC here in 2007. In 2007, we were I also tried to dry the IGBT, but it didn’t work well, there are patent restrictions.

【提问】:第三个问题,我想问几个关于你们上游的问题,我知道你们也是属于最早尝试使用像颗粒硅这种新技术的企业。

【沈总】:颗粒硅不行,1998年我就在用。

【提问】:你们首先尝试这个的初衷是什么?因为它的价格跟棒状硅也差不多。

【沈总】:这个时点里掉在地上的料子跟棒状硅卖一个价,真的是这样,历史上的颗粒硅不是这样,颗粒硅回到它的本质的时候,我跟你吹个牛,2001年到2004年我是中国最大的多晶硅料贩子,谁都没我多晶硅多,你可以问那个行当里面的人,换句话说,甚至到2007年中环拿的多晶硅也比全国的弟兄们多,我是最大的料贩子,颗粒硅的原理如果走通,它确实成本低一些,但是它没做好,就跟刚才我说TOPCON一样,你没做好,并不能说是颗粒硅错了。

【提问】:现在像颗粒硅跟CCZ对话,你们的尝试或者你们的进展大概是怎么样?

【沈总】:TCL投了40%,好像公告是这个数,怎么今年也得开建了。

【提问】:从这个意义上来说,你们也挺看好这个?

【沈总】:我刚才在会上的时候讲过,中环投内蒙多晶硅,第一是受政府之托,第二中环要解决1万吨中国制造的半导体料,但是如果中环光去投这1万吨的半导体料,这1万吨的半导体料挣不了钱,1万吨的半导体料配上10万吨的光伏,它的规模化就出来了,它就可能挣钱。

【提问】:投颗粒硅的品质能达到电子级?

【沈总】:不是,它们共用了公辅设施,动力、水电气。

【提问】:你们要用电子硅料的时候不是用颗粒硅的料?

【沈总】:不会,电子硅料好像没有安排颗粒硅,但是买来颗粒硅技术的本质就是用在半导体,我1998年用的时候也用在半导体。

【提问】:你们现在对颗粒硅和CCZ联合起来,你们自己有没有做这个验证,研发到什么阶段?能不能解决?

【沈总】:现在颗粒硅一直是我用,好像没用到CCZ,我从来不用CCZ技术。

【提问】:因为他现在希望这个技术突破以后你们硅片还是有这种机会。

【沈总】:我觉得你的消息可能不太准,CCZ跟颗粒硅没必然关系,颗粒硅比较适合CCZ,大概是这样,它不是充分必要条件,不能划等号。

【提问】:最后一个问题问的稍微大一点,现在如果我们把光伏看成一个整体的话,比如光伏整个产业链挣10块钱,现在很多人在分析各个环节,因为环节比较多,有时候这个产能过剩,有时候那个卡脖子,所以大家总在想要划分出来哪个环节的价值量最大,因为这两年可能是硅料环节的产能利润、价值量相对来说大一点,比如说你一共挣10块钱,硅料挣四五块钱。

【沈总】:硅料好像分走7块钱,8块钱好像都分走了。

【提问】:我举个例子,这么多分析师、做业务的大家问很多问题,包括很多企业的问题都是想分析这一段期间哪个环节会占到最大的价值量,因为你们各个环节都在扩产,都在发展,有一个逻辑说如果长期来看,扩产最慢的这个环节跟最难的这个环节相对来说哪个更有价值量?我不知道您对这个观点怎么看?

【沈总】:你这个理论是投机理论,本质里价值的分享应该是跟投资的强度和产值,换句话说投几见几发生关系,正常的时候应该大多是这个思维,这是第一。第二再发生的关系很显然应该不是这种情况,很多人不知道多晶硅价格真不算高,我炒料的时候,20美元炒来,我能400美元卖出去,这算什么,这是真事,这是炒作,你不要用炒作的原理来思考,用供需的理论来讲这个东西,商业的本质里面投资多的人该得到更多的回报,技术门槛高的应该得到回报,而不是说炒作得到回报,应该是这样。在一个成熟的经济体里面很少听说像中国这么炒作的,老外看到我们也晕,瓦克今年挣了一把钱,现在买瓦克一公斤难求的东西,但是我拿走了瓦克的一半产能,没说瓦克给我涨了价,中国的商业原理,如果是中国光伏还想用全球的计算量来计算自己,真的不该这么干,有一天被收拾的时候,前面倒下四位了,后面再倒了几位也不奇怪。

【提问】:我来自赛维所在的那个城市,现在行业很景气,但是你们还是要考虑风险,想问一下后续你看这个行业可能会存在哪些风险,或者说你们有哪些应对?

【沈总】:刚才海鹏总描述了一个短期现象,我自己认为到2023的时候,从现在到2023,毕竟上游产出了这么多,我先从市场角度来讲,印度市场对我们关闭了,大家都知道,欧洲市场美国佬试图made in US,这个很清晰,印度市场也要made in 印度,欧洲市场现在会敞开要咱们任何东西,你只要卖他就敢买,你自己也挺美的,你挣到欧元,欧洲没办法了,被打烂了,所以说我们展望2023的市场里面,可能会这么来理解,欧洲人会持续的买咱们的东西,只要不是不让干的话,欧洲人愿意买咱们的东西。印度人的逻辑和美国人的逻辑,美国人的逻辑是一定要持续反应,一边买一边打,至于打到谁了,就看谁命不好,他肯定是这段时间打ABC,过两天打DEF,他一定是这么干的。2018年当时我们和SunPower一起差点儿把(38:30英文)给收了,你知道美国的SEMA怎么补贴的吗?就是收各位的税源,主要的资金来源,当时SunPower拿这个钱拿了不少,美国人这种特别的关税收来了以后留在那儿,不是揣到你们的口袋里,就是这么来补,各个国家国情是不一样的,换句话说,我们来短线看的话,明年我个人认为还是不错,从市场看是不错,但是供应侧会来的更多一些,因为凭什么就你能做多晶硅,你挣300%的东西,我也要挣这个钱,中国市场里面多晶硅过剩,如果是这样,我认为行业比较看好的温柔的降下去,市场比较好,供应开始抬升,价格开始下降,大家有计划的温温柔柔的下去,但是如果组件价格不下来,还挺着两块钱,别断崖,一断崖集体躺下,这是两种极限的情况。

我们来说第一种情况,价格温柔的这么下去,同时市场供和需这两块的平衡线相对好一些,中环可能会受很大的影响,毛利率上升,稼动率上来,乘2的关系,会得到这样的好处。还有一种是因为我毛利高,硅耗低,谁也不敢往那儿伸,过去中环说自己硅耗低,很多人要说两句我硅耗比他还低,那你证明,这一块我的状态会比较舒服,稼动率高了,利润也高了,客户市场占有率也上来了,我三个都得到了,如果发生刚才后面那种情况,断崖,我弟兄们断现金,我不亏损或者挣利润,弟兄们有成本,我还保有利润,但是我挣不了大钱,这是我的算账法,不知道我说清楚了没有。两种情况,第一种我赢,第二种我不输,本质里是来自于我自己的竞争力,张海鹏刚才告诉你们的,硅料一下来,非硅成本扮演重要的作用,我的非硅比你牛,大概是这样。

【提问】:我问一个叠瓦组件的问题,因为我没有查历史资料,叠瓦组件是收购过来的还是?

【沈总】:不是,叠瓦组件是我们和法国道达尔一起控股的,历史上SunPower无条件授予中环使用的一个专利,所以说任何侵权行为我们两家都有责任维护专利的有效性和合法性。

【提问】:我想问一下这个叠瓦组件的应用场景有没有说特别适用于某一种场景?还是说跟其他的组件一样的,各个场景都适用的?

【沈总】:它比较抗遮挡,它比较抗干扰,不管是阴影遮挡还是风压,叠瓦组件是这个东西,这是一个独特的专利,我们行业里面好几家公司,头部的都想说我给中环代工费,你们做贴牌,但是中环坦率的说自己也不能完整的决定这件事,还要跟Maxeon商量,这是第一点。第二点,中环是一个做硅片的公司,至少在当前阶段或者说可预期的未来里面中环还是一个以硅片为核心的公司,并不想把组件做的很大,跟自己的客户大大的打一架,中环要做180GW的硅片,你可以算一下,高斯分布那些你不喜欢的东西我都会去做成组件。

【提问】:我有一个问题想请教您一下,目前来看不管是TOPCON或者是HIT,它们发展的很好,也有很多投资者在投,但是目前看都是有各种各样的问题,您觉得下一代的电池技术您更看好哪一种?

【沈总】:我肯定看好IBC,我个人来说更看好IBC,非常简单,你如果感兴趣的话,你认真去研究它的半导体结构,这个结构是最可控的,它有一个缺点是供应步骤比较差。HIT在这儿说有点吹牛,1982年我就做HIT,我上大学以后,你们能查毕业论文,上过电子学报,那个结构是很难解决的,我现在看到所有做HIT的人,它跟40年的东西也是一样的,不要说我是HIT专家,你可能是HIT的设备专家,这个我赞成,但是某个做电池的哥们说我有独特的HIT技术,那真的不要说,30年前解决了,40年前就在忙活了,你把HIT的设备解决的非常好,一次性做的非常好,这真了不起,HIT是一个非常好的结构,但是它就是难做,工艺难做。

【提问】:实验室更容易,但是量产可能会出现比较大的问题、困难。

【沈总】:工业化是非常难的问题,光伏不是半导体,一个小时要几万片、几十万片下去,关键是做HIT结构的时候你是用抛光片来做的,你拉了一个绒面做的,你在这样一个起起伏伏的面里面要均匀的覆盖两纳米或者说几十纳米,这个事听起来就很难。

【提问】:想了解一下硅片最近的涨价。

【沈总】:我们今天好像涨价了,昨天多晶硅又涨价了,好像是昨天涨了我们就响应了,响应多晶硅涨价。

【提问】:石英坩埚的供应紧张会不会影响到后面,因为二季度液晶的产量是6GW到7GW左右,会不会影响到下半年产能的放量?我前两天听了一个专家的会议,现在市场根本没有说石英坩埚长单的说法,中环到底有这个文没有?

【沈总】:造谣,我给你负责任的说,准确的统计,35%石英量在中环。

【提问】:有一个石英股份。

【沈总】:让他涨去吧。

【嘉宾】:石英砂是这样的,先说进口的高质石英砂,五个9的高质石英砂,尤尼明、TQC这两家,大概每个月的3万到3.1万,沈总刚才讲的,这里面进口砂35%在我们手里,这一部分砂打坩埚大概300GW,加上中国国产的高质石英砂,四个9的。

【沈总】:这个地方我要补一下,矿美国这个地方真的是上帝给的,他的石英是活象的,咱们的石英矿羟基杂质多,他的石英矿真的很奇特,咱们的石英量要比美国大,但是美国偏偏有一个半活象的,这就是上帝给的,所以说美国佬真的是很牛逼,做页岩气也比咱们牛。

【嘉宾】:从总量上来看,一般来讲内层都用高质的,进口的,大概50%-60%的比例,外层用国产砂,包括用混合砂都有,大概明年的产量里进口砂会到3.7万,这样增长不大,整个来看明年整体平均的占比,进口砂会占到整体的40%,会减到40%,但是我们因为锁了海外的这部分35%。

【沈总】:也不叫锁,中环还是一个十几年来很讲规矩的公司,当年把尤尼明害死的,咱不说谁了,人家投产了,那个哥们告诉他说我没这个需求,这就把尤尼明给破产了,现在接手过来了。我跟瓦克为什么这么提?2016、2017的时候整个多晶硅卖不掉,因为我跟瓦克有战略合作,他一半我都买过来了,一个公司还是该尊重自己的企业精神,那天你跟我说有一个假专家。

【提问】:行业会缺吗?

【沈总】:行业不是这样缺的,我们昨天还在讨论,说起这个问题,说大家今天可能会关注石英,石英不会缺,绝对数不会缺,你搞出7万吨石英有什么问题,你都用中国的、印度的、巴基斯坦的,巴基斯坦石英矿,但是你用这样的石英矿会造成你的拉金成本上升,产品质量下降,它是这个道理。

【提问】:成本上升、良率下降是吧?

【沈总】:对。

【提问】:我听那个专家会议,他说在印度那边可以找到类似的,但是只能做外层。

【沈总】:做内层又怎么了。

【提问】:因为石英坩埚,总觉得明年硅片价格战担忧打不起来。

【沈总】:我也别说谁,目前挣的硅片钱都是从硅料里面挣来的,你有什么权利明年或者说现在跟人家打架,你跟人家签一个20年长单或者说2年长单,但是这里面你要想想本质里的逻辑是什么,本质里的逻辑是硅料厂太不喜欢中环和隆基了,他一定要有第三势力,但是竞争的逻辑,当硅料没有权利来选择的时候,那是隆基和中环说我更喜欢用谁的料。

【提问】:目前行业大多数认知是硅料片三季度到四季度好像有能见度比较高的产量放出来,但是石英坩埚目前大家还是看不到比较紧缺?

【沈总】:我不这么认为,我先姑且不说你签的单,一个好的拉金工厂能用好国产砂、印度砂,只不过会增加两块钱,对于一个工程师文化的公司,他不是用不好国产砂。

【提问】:工艺的问题是吧?

【沈总】:什么事都是用什么换什么的,人造砂是他用的,他是全中国最大的用量,他做半导体,他也是唯一能拿到进口石英砂的人,那个肯定是炒作,而且说中环没有石英砂,不可能,这个哥们连姓都不敢说。

【提问】:但是你们今年提价又很有底气,你们以前好像跟着隆基提价,今年你们就是领先市场,是不是跟石英坩埚有一定的关系?

【沈总】:不是,跟这个一点关系都没有,因为隆基更多的一体化,中环是一个卖硅片的人,隆基提价有什么好处?提给自己组件厂还是提给自己电池厂,中环的专注度更高,所以说中环来表态是合理的。

【提问】:是不是你们目前对组件业务的发展诉求还不太强烈?

【沈总】:如果中环差异化制造证明了自己在组件的差异化能力,而且是领先的,那就要选择,但是中环还是一个做硅片的公司。

【提问】:你们这边看好IBC电池技术,你们未来会自己规划去做这个电池吗?

【沈总】:Maxeon会,我知道国内做BC的人大概都在Maxeon 3这个层面里面,大家对于BC的理解,不管它叫TBC、EBC、ABC,BC是一个所谓的差值结构,大家对BC的理解很弱,对电极BC的核心包括封装也能力很弱,对BC的了解很差,它不是光一个电池,BC的组件封装跟现有的封装技术完整的联合在一起,我那儿有IBC的很多电池结构,它的封装跟这种封装完全两回事,它背后是铜,铜是不好焊的,铜是无法焊接的,铜跟锡是焊不到一起的,我不知道国内现在有很多做BC的人封装怎么解决的。

【提问】:你们怎么看友商的HPBC技术?

【沈总】:先把BC的专利过了再说,你随便做,你随便测试,你要一量产,侵犯到中环合法的知识产权权益,对不起,可能要打官司,不管是什么友商,不管是哥们还是天王老子也要打,那肯定的,除非你绕过这个专利,但是我认为干了30年的IBC居然让人家干了两年把专利绕过去了,美国佬是猪,中环也是猪。

【提问】:耐性硅片对硅料的要求。

【沈总】:国产料可以的。

$TCL中环(SZ002129)$ #雪球调研团走进TCL中环# $隆基绿能(SH601012)$

本话题在雪球有55条讨论,点击查看。

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

本文转自: http://xueqiu.com/8126729077/226888938

This site is for inclusion only, and the copyright belongs to the original author.