It’s been a long time since I wrote an article about $Wide Wine (SH600702)$ , but it’s not a transformation of an emotional blogger, but the principle of speaking less if the results are too bad . After all, the stock market has always talked about results. And I did make a lot of mistakes. The fans who followed me saw it. I made the mistake of chasing high at the wrong time, so I won’t go into details . Although I didn’t write a long article about Shede Wine Industry, I have been tracking the channel data all the time, showing both the good and the bad to everyone. Consumption during that time is not good. You know the reason, and you can’t write a flower. You can only continue to track the payment situation and find beliefs from the perspective of fundamentals.

22Q2 performance outlook

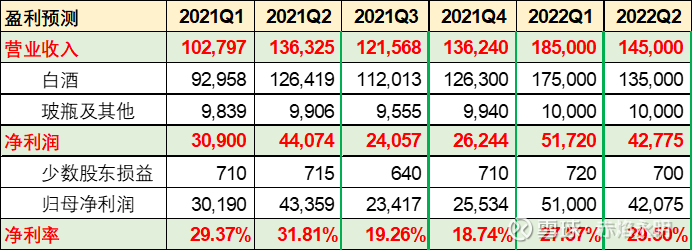

From what we know so far, the 22H1 repayment is 3.5-4 billion yuan, deducting 13% value-added tax; in addition, the contract liabilities (accounts received in advance) are about 400 million yuan, and there is not much room for adjustment of this part of the reservoir. Under normal circumstances There are 200-300 million in the bottom, and the part that can be adjusted to the income is about 1-200 million. Taken together, the revenue that can be recognized in the first half of the year is about 3.3-3.4 billion, then the revenue in 22Q2 is about 1.4 billion, a slight increase year-on-year, and if you work harder, the growth will be within 10% . The net profit should be about the same, maybe a little bit worse . The second quarterly report has overcome the difficulties together, making a lot of profits to the dealers, and the sales expenses will increase faster.

The worst time is over . Although the situation in the second quarter was not good, it was not due to the company or the industry. It was caused by the general environment. Even if the performance was unsatisfactory, it was also the fundamentals of the past. Investing is always looking forward, and stocks are always pricing the future . With the coming of summer, the influence of YQ is getting weaker and weaker. The consumption scenarios of liquor such as wedding banquets and college entrance banquets are returning. The peak season of liquor in the third quarter is coming, and the company’s fundamentals will fundamentally improve. You must know that even if the situation in the second quarter is not good, willing to not press the goods to the dealers, and the channel inventory is kept within 2 months , which greatly reserves the distribution space for Q3, and the revenue of 2021Q3 is only 1.2 billion. Don’t be surprised when net profit grows by 3 digits. The so-called “the way of heaven, the excess is lost and the deficiency is made up” . If there is less Q2, there will be more Q3; compared with 2021, there will be more Q2 and less Q3.

The second-high-end liquor has entered the knockout round. This wave of national expansion requires both brand appeal and channel control, otherwise it will fall behind. Willing to maintain strategic focus at present, not aggressive for short-term achievements, nor rash for long-term goals, such as reluctance. I am willing to walk steadily on two legs. The consumption is downgraded to the “Tuo brand” of the bottled wine. During the YQ period, it sold very well and contributed a lot; the consumption upgrade is the turn of “taste” and “wisdom” , no matter how high it is. There are also “Maoxiang” and “X Zhihu”, replicating the successful example of Fenjiu in 2017-21.

This topic has 21 discussions in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/1614119807/222930927

This site is for inclusion only, and the copyright belongs to the original author.