(Image from UNsplash)

(Image from UNsplash)Welcome to the WeChat subscription number of “Sina Technology”: techsina

Text | Hernanderz

Source: Value Institute

From the popularity of Amazon’s first-generation Echo to the entry of Google and Microsoft, and then to the domestic Xiaodu, Xiaoai, and Tmall Elf, the smart speaker industry has gone through a glorious growth process, but I didn’t expect it to collide so quickly. Ceiling up.

According to the latest report from IDC, the sales and sales of smart speakers in China both fell sharply in the first half of this year. Extending the time axis can also find that the decline has continued for a period of time.

The reason behind it is actually not complicated: the over-saturated market and unstable quality are all old problems. On the black cat complaint platform, several major smart speaker brands have nearly a thousand complaints, and a large number of users are dissatisfied with the product quality and the brand’s after-sales service.

The reason for such a situation today is that the price war that started in 2019 cannot escape the blame.

Due to the dazzling growth rate of the early market, a large number of start-up brands and R&D teams have emerged in the domestic smart speaker industry in a short period of time. price war. According to media statistics, at the most exaggerated time, in Huaqiangbei, Shenzhen alone, there were more than 200 teams operating the smart speaker business.

However, the result of the price war was cruel, and the small and medium-sized manufacturers who were unable to do so fell down one after another. The smart speaker industry has now entered the “oligarchic era” in which Xiaomi, Ali and Baidu are three-thirds of the world. In order to restore the favor and trust of users, the three giants are leading a transformation movement towards the high-end market.

The success or failure of this transformation may determine the future of the smart speaker industry to a certain extent.

Sales fell 27.1%,

Why can’t smart speakers sell?

In the first half of the year, the development of the technology hardware market was not optimistic. Today, even a number of giants are vying to enter the game, and the once quite prosperous smart speaker market has begun to decline.

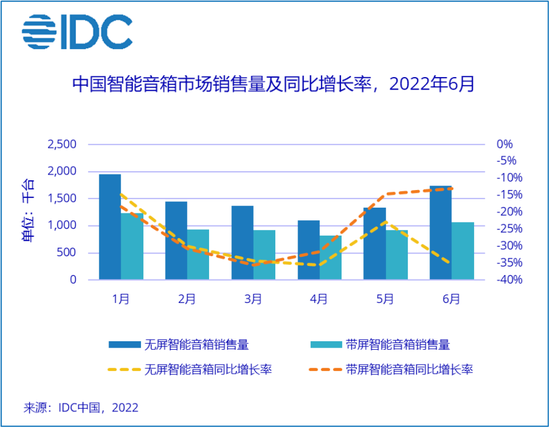

On August 3, the internationally renowned data agency IDC released the latest “Monthly Sales Tracking Report of China’s Smart Speaker Equipment Market”. Data show that in the first half of this year, the sales volume of China’s smart speaker market was 14.83 million units, a year-on-year decrease of 27.1%; the corresponding sales amounted to 4.2 billion yuan, a year-on-year decrease of 16.2%.

(Picture from IDC)

(Picture from IDC)From the growth curve, it can be seen that the decline of the smart speaker market has continued for a period of time, and the decline has become more and more obvious. Historical data shows that in the same period last year, the year-on-year growth rate of domestic smart speaker market sales fell to 0.4%, and the growth basically stagnated. Liu Yun, a senior analyst at IDC China, also bluntly stated in the report, “The demand for China’s smart speaker market is gradually returning to rationality along with the decline of the early adopter boom.”

In terms of the distribution and proportion of channels, the online e-commerce channels that have performed best in the past also began to show fatigue last year. Data shows that domestic smart speaker online channel sales have declined for six consecutive quarters since the fourth quarter of 2020.

Looking at the sales volume of specific products, the sales volume of smart speakers without a screen is still higher than that of smart speakers with a screen, but the growth rate of both is terrible. According to IDC statistics, in the first half of this year, the sales of smart speakers without a screen and with a screen were 8.94 million and 5.89 million, respectively, down 28.9% and 24.3% year-on-year, and the sales ratio was close to six or four.

In the view of the Institute of Value, the trend of smart speakers can be said to come and go quickly.

During the outbreak period from 2018 to 2019, domestic smart speakers recorded a year-on-year sales growth rate of 823.3% and 126.6% respectively, which can almost be said to be a leap to the sky. But in 2020, this figure fell off a cliff to 2.4%, until now it has fallen into negative growth.

Historical experience tells us that if an industry develops too fast, some common problems will definitely occur: immature supporting industry chain, excessively intensified competition in the industry, short-term surge of practitioners, resulting in uneven product quality…

The smart speaker industry naturally cannot escape these laws. When the freshness passed, users’ dissatisfaction with the quality of smart speaker products began to increase.

Searching for Xiaodu speakers, Xiaomi speakers and Tmall Genie on the black cat complaint platform, you can see nearly a thousand customer complaints, most of which are for product quality and after-sales service. Many users expressed doubts about the quality of the above-mentioned products and the service commitments of the manufacturers, and there were even complaints such as “the Tmall Genie cannot be turned on without using it”, and “the so-called smart speaker did not respond to instructions at all”.

(The picture comes from the black cat complaint platform)

(The picture comes from the black cat complaint platform)Objectively speaking, compared with hardware products such as mobile phones, tablets and even smart watches, the development and production of smart speakers is not difficult.

In the development of smart speakers, AI is an important technical difficulty. In 2014, Amazon, the pioneer of the smart speaker track, made a head start with the Echo implanted with intelligent voice interaction technology. However, with the vigorous development of the AI industry in recent years, interactive technology has made great progress, and most of the leading manufacturers have already overcome this difficulty.

According to statistics from the Prospective Industry Research Institute, Baidu, Ali, Xiaomi and other smart speaker manufacturers are among the best in the world in the number of patents and authorizations for artificial intelligence technology. Among them, Baidu’s artificial intelligence patent applications and authorizations reached 9,364 and 2,682 respectively, both of which have reached the top.

Since the core technology is not a problem, why can’t the quality of smart speakers be recognized by consumers?

The problem may lie in the keywords of competition and cost.

After the tuyere broke out around 2018, capital rushed in, a large number of small and medium-sized manufacturers entered the game, and the smart speaker track became crowded instantly. The increase of players will inevitably lead to the deterioration of the competitive environment and quickly consume the original market space. In order to compete for new customers, manufacturers have chosen to expand into the sinking market, setting off a round of smart speaker price wars.

When quality gives way to sales, and when cost performance becomes the number one pursuit, it may not be difficult to understand the aforementioned crisis of word of mouth.

The industry ecology destroyed by the price war,

“Oligarchy era” brings new opportunities?

Looking back at the development of the smart speaker industry, 2019 should be the climax of the price war, but it is also the starting point for quality disputes and soaring negative reviews.

According to data from Canalys, in the first half of that year, China surpassed the United States for the first time in sales of 15.56 million units, becoming the world’s largest smart speaker market. Supporting this explosive growth, in addition to Baidu, Ali, Xiaomi and other giants, there are also hundreds of small and medium-sized businesses and new brands.

According to data from Yiou Think Tank, as of the first quarter of 2019, there were nearly 100 domestic smart speaker brands. What you need to know is that in addition to the data on the surface, there are more “white-brand” products out of the market. According to media statistics, at the most exaggerated time, there were more than 200 teams operating the smart speaker business in Huaqiangbei, Shenzhen alone.

However, it should be noted that although the sales and sales of domestic smart speakers increased significantly at that time, the penetration rate was not high. Data shows that as of the first half of 2019, the penetration rate of smart speaker users was only about 8%, far less than 26% in the United States.

Considering the size and population size of the Chinese market, both the head manufacturers and the players with small waists believe that this track has more potential to be tapped. As for the development focus, they all set their sights on the third-tier and below sinking market.

In August 2019, Jing Kun, vice president of Baidu and now the CEO of Xiaodu Technology, said bluntly in an interview with the media:

“We must lower the threshold for products (smart speakers), and penetrate all the cities from first-tier to sixth-tier cities, so that more people can access these products.”

Like smartphones and other IoT hardware, cost-effectiveness is the top priority if you want to enter the sinking market. In view of this, Baidu Xiaodu, Ali Tmall Genie and Xiaomi’s Xiao Ai have reduced the price. The Dingdong TOP series jointly created by iFLYTEK and JD.com has hit an ultra-low price of 49 yuan.

However, the player team is inherently uneven, and the excessive pursuit of cost performance and high sales will definitely sacrifice the quality of the product to some extent. Thinking of the word-of-mouth crisis mentioned above, the negative impact of this price war on the industry may be beyond our imagination.

Of course, a large number of small and medium-sized brands with limited strength are unsustainable and defeated in the price war, which is not necessarily a bad thing for the long-term development of the industry.

The RUNTO report pointed out that in 2021, the number of brands of smart speakers sold in China will decrease from 44 in the previous year to 34, and the survival of the fittest within the industry continues. After going through rounds of big waves, the competition pattern of the smart speaker market has become more stable now, and the dominance of top brands has become difficult to shake.

Although Huawei and other brands are still working hard, in the domestic smart speaker market, the pattern of Baidu, Alibaba and Xiaomi’s melee has basically been determined. The same data from IDC shows that Alibaba and Baidu occupy the top two with 34.96% and 33.4% of the smart speaker market, respectively, while Xiaomi ranks third with 27.2%, and the total share of other brands does not exceed 5%. , it is difficult to become a climate at all.

The situation abroad is similar. A report from another data agency Omdia shows that the global smart speaker market in 2021 will be about 13 billion US dollars, and the total annual shipment will be about 190 million units. Ali, Baidu and Xiaomi have a combined market share of 52%. It topped the list with 42 million units.

In the first quarter of this year, the total share of the top six smart speaker manufacturers exceeded 85%. In addition, in CNPP’s brand data research, the brand index of Xiaodu, Tmall Genie and Xiaoai also swept the top three, and even stepped on Apple’s HomePod.

Objectively speaking, the three giants of Ali, Xiaomi and Baidu have completely brought the domestic smart speaker market into the “oligarchic era”.

In order to compete for market share and develop sinking markets, leading manufacturers sacrificed quality to fight price wars, which indeed pushed up the overall sales of smart speakers in a short period of time. However, with the market penetration rate peaking and users’ requirements for product quality increasing, this expansion strategy with obvious flaws no longer meets the requirements of the times.

For a period of time in the future, the transformation to high-end, and restoring user reputation through high-quality products may be the key to reversing the decline of the smart speaker industry.

High-end transformation into mainstream

Leading manufacturers have their own tricks

After the early popularity, users’ attitudes towards smart speakers are changing, and they are no longer in the early adopter stage, and cost performance is not the only factor they consider.

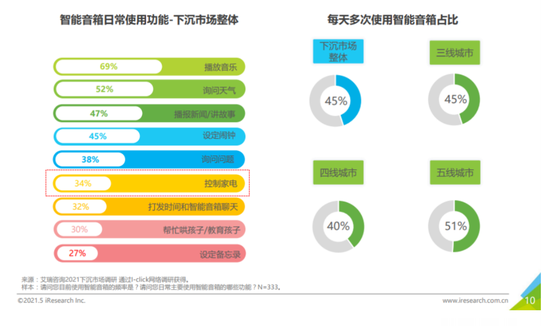

According to statistics from iResearch, more than 40% of consumers in the sinking market said that the primary purpose of purchasing smart speakers is to experience high-tech technology, which is much higher than 18% of choosing cost-effective. In third-tier cities and fifth-tier cities, technological factors and functions have surpassed early adopters and become the primary purpose of consumers purchasing smart speakers.

Enlarging the survey respondents to all markets, the top three user requirements for smart speakers are rich in functions, accurate speech recognition and good sound quality, accounting for 38%, 35% and 33% respectively, far higher than appearance and price. and other options. In addition to the simplest music playback, weather forecasting, setting alarm clocks, controlling other smart home appliances, searching for problems, and even coaxing children are all functions that users want smart speakers to have.

(Picture from iResearch)

(Picture from iResearch)All of the above data are enough to show that smart speakers want to capture the favor of consumers, and improving quality is the last word. As for the specific approach, the three giants Ali, Xiaomi and Baidu gave their own answers respectively.

In addition to playing the ecological card as always, Xiaomi strives to strengthen the linkage between smart speakers and other IoT products, but also regards sound quality as an important selling point.

At the Xiaomi conference in August last year, Xiaomi Sound, a smart speaker with a starting price of 499 yuan, received a lot of attention, focusing on the design and appearance and the sound effects that exceeded expectations have been well received by the media and users.

According to the evaluation of technology media Lei Technology, the actual playback effect of Xiaomi Sound is not inferior to products of the same level on the market. In particular, the sound pressure can easily cover the music playback in the entire living room. The audio density is not low at medium volume, and the mid and high frequencies are not entangled together, which is quite layered.

(The picture comes from Lei Technology)

(The picture comes from Lei Technology)Baidu combines its technical advantages in the field of AI and strives to improve the intelligent interactive performance of its products.

According to research by Jovester Sullivan, Baidu’s AI technology comprehensive strength and the number of AI projects have been ranked first in China since 2020. Even if we look at the world, it still lags behind a few such as Google, Amazon, Microsoft and IBM. International giant.

According to the data, the R&D personnel of Baidu’s AI technology team account for as high as 61%, which is at the leading level in China. Since the early products in 2018, the interactive functions of Xiaodu smart speakers have been continuously added, such as far-field wake-up, children’s mode, geek mode, etc. are constantly improving.

Of course, Baidu is also trying to empower Xiaodu smart speakers through hardware ecology, but it pays more attention to AI technology attributes in this process.

At the Baidu Developers Conference at the end of last year, Xiaodu Technology CEO Jing Kun told the media, “Xiaodu is not a hardware company, it is still an AI technology company.” This speech not only emphasizes Xiaodu’s AI label again, but also means that Xiaodu will always build its own hardware ecological chain around the theme of AI.

At present, in addition to smart speakers, Xiaodu has successively launched products including fitness mirrors, voice alarm clocks, and large-screen eye protection learning machines. The newly unveiled DuerOS 7.0 at the end of last year will provide more reliable technical support for the linkage of these hardware.

As for Ali’s Tmall Genie, in addition to the same emphasis on intelligent interactive functions, it also hopes to make a fuss about application scenarios – such as launching special products for different scenarios such as in-vehicle, education, and hotels.

As early as 2019, Ali announced that it has reached cooperation with BMW, Volvo, Daimler, etc. Tmall Genie has become a dedicated smart speaker for BMW’s mass-produced luxury models. At the same time, Alibaba’s AutoNavi A+Box in-vehicle system and Zebra Zhixing intelligent in-vehicle system also have Tmall Genie.

In the view of the Value Research Institute, customized products for subdivided scenarios are very promising to open up a new world for the smart speaker industry.

The reports of IDC and iResearch mentioned that in addition to basic functions such as music playback and alarm clock, users have more and more functional requirements for smart speakers, and they want to do crazy things in a small speaker. Addition is not realistic. At this time, products for specific application scenarios become more valuable.

In general, Tmall Genie needs to extend application scenarios and create customized products. Baidu is betting on AI interactive technology, and Xiaomi focuses on hardware ecology and sound quality. The three giants have their own priorities and strengths. As for who wins or loses, it depends on who has the strongest technology.

write at the end

In 2017, Xunlei founder Cheng Hao gave a piece of advice to entrepreneurs in the smart speaker industry in an interview with Titanium Media:

“I have seen a lot of smart speaker startups recently, but overall, this track does not belong to startups.”

In this interview, Cheng Hao mentioned many factors that are unfavorable to startups, such as lower technical barriers, the cost of building a smart hardware ecosystem, etc., which will be fulfilled one by one in the future. Facts have also proved that giants led by Baidu, Ali and Xiaomi are more suitable to serve as the mainstay of the smart speaker market than a group of start-ups.

All in all, after the previous price war and the reshuffle of the competitive landscape, the dominance of Baidu, Ali and Xiaomi cannot be shaken in a short period of time, which also provides sufficient guarantee for them to explore and transform into the high-end market. The success of their high-end exploration is crucial to the development of the entire industry.

Fortunately, the three giants have all found their own direction and are all working hard. The remaining questions are left to time and products to answer.

(Disclaimer: This article only represents the author’s point of view and does not represent the position of Sina.com.)

This article is reproduced from: http://finance.sina.com.cn/tech/csj/2022-08-05/doc-imizirav6913515.shtml

This site is for inclusion only, and the copyright belongs to the original author.