Disclaimer: I never recommend stocks, all articles are for business fundamentals only. Studying a company is a long-term and continuous process, and there is no timing, and the stock price fluctuation of the individual stocks discussed has nothing to do with this article. The market is changing rapidly, and all research and analysis are time-sensitive.

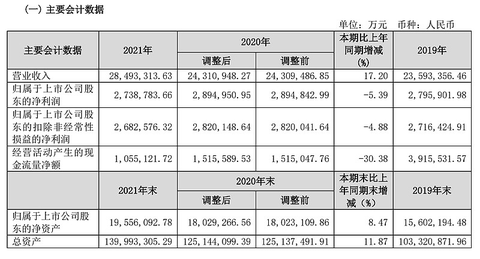

The annual main operating indicators of Poly Development have been announced in January, and the data in the annual report are almost the same: during the reporting period, the company achieved a total operating income of 285.024 billion yuan, a year-on-year increase of 17.19%; net profit of 37.189 billion yuan, a year-on-year decrease of 7.14% %; the net profit attributable to the parent was 27.388 billion yuan, a year-on-year decrease of 5.39%; the basic earnings per share was one penny lower, at 2.29 yuan, a year-on-year decrease of 5.61%. This is already an excellent performance among housing companies with widespread thunderstorms.

Like the entire industry, the company entered the settlement period at a historically high price, increasing revenue but not profit. During the reporting period, the company’s gross profit margin was 26.80%, a year-on-year decrease of 5.79 percentage points, of which the gross profit margin of real estate sales was 27.13%, a decrease of 6.35 percentage points. In 2021, the company’s net profit margin will be 13.05%, a year-on-year decrease of 3.42 percentage points. This is the direct cause of the 5.39% decline in net profit attributable to the parent company against the backdrop of a 17.2% year-on-year increase in operating income.

Even with the gross profit margin after the sharp drop, Poly is still significantly better than its peers, whose gross profit margin is generally lower than 20%. The reason is that “the leading state-owned enterprise is a distinctive brand symbol of the company, which enhances the market’s trust and recognition of the company. This enables the company to have outstanding advantages in diversified land acquisition, cooperative development, low-cost multi-channel financing, and product sales.”

In 2021, Poly Development “achieved a contracted amount of 534.929 billion yuan, a year-on-year increase of 6.38%; the contracted area was 33.3302 million square meters, a year-on-year decrease of 2.23%. The company expanded 145 projects throughout the year, with a new floor area ratio of 27.22 million square meters. The amount was 185.7 billion yuan, down 15% and 21% year-on-year respectively.” “At the same time, the company focuses on improving the quality of expansion and resource control. During the reporting period, the volume of new residential units accounted for 85%, and the expansion equity ratio was 72%.” “The annual land price for the company’s expansion was 6,821 yuan/square meter, down 8% year-on-year.”

At present, the comprehensive financing cost of Poly Development is about 4.46%, down 31 basis points from the end of last year. The scale of the company’s interest-bearing liabilities is 338.2 billion yuan, and all indicators are in line with the “three red lines” medium and green enterprise standards. By the end of the reporting period, the balance of cash and cash equivalents at the end of the Poly Development period was 170.2 billion, an increase of 17.2% over the same period last year, which was the same as the growth rate of operating income, which was not easy compared to its peers.

If in previous years, the above data seemed bland, but after the baptism in the second half of 2021, it is very difficult for real estate companies to maintain their own routine. It can be said that the current real estate companies No fault is good. When many competitors have fallen or retreated, it is an advantage to be able to adhere to their own development rhythm.

In the past few months, I have been emphasizing that the real estate development industry has entered an unprecedented clear pattern, that is, the leading central and state-owned enterprises have occupied an absolute industry leading edge. This is very obvious in Poly. This year’s sales are highly likely, and there is a possibility of further improvement in the future.

Unlike many real estate companies, the net profit attributable to the parent and deducting non-net profit in Poly’s 2021 annual report is only 562 million lower than the net profit attributable to the parent, and there is no significant impairment, so that the overall profit change will be smoother. But it will not be like some real estate companies. The 2022 report data will look better because of the low year-on-year base.

The report clearly pointed out that “in the future, with the continuous implementation of high land price projects, the performance of gross profit margin will still be under pressure”. It is expected that Poly’s annual report data for the next year will not have a high net profit growth rate, but with the high gross profit plots it has acquired since the second half of 2021, it will gradually enter the sales period. Starting from the second half of 2022, Poly is expected to Continuous breakthroughs in sales data. Judging from the annual report, the report data starting in 2024 will usher in an obvious process of accelerated growth of net profit margin, and this process will last for a long time. This is the main investment point of Poly Development at present.

In the report, the most controversial is the dividend. According to the report, “a cash dividend of 0.58 yuan per share (tax included)” is calculated based on the closing price of 18.39 yuan on April 18, which is equivalent to a dividend rate of 3.15%. Calculated, this dividend rate is roughly 25%, which is indeed not high, but this was also clearly announced in last year’s annual report, but the lower limit was taken.

At this time, there are a large number of projects in the market, and the net profit margin can reach more than 10%, and many can even reach 15%, which is more than double the same period last year. It is also understandable that the company is keeping more cash to increase its land bank. In addition, the report also repeatedly emphasized that the current sales environment is generally poor, leaving cash to prevent the market from cooling down further, which is also a necessary precautionary awareness.

Whether you like dividends or pay more attention to the future development of the company depends on the personal preferences of investors. @Today’s topic $ $Poly Development (SH600048)$

There are 22 discussions on this topic in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/6056806984/217371208

This site is for inclusion only, and the copyright belongs to the original author.