Welcome to the WeChat subscription number of “Sina Technology”: techsina

Text/Ginkgo Technology

Source/Ginkgo Technology (ID: yinxingcj)

As major mobile phone manufacturers “deliver the papers”, the whistle will sound at the end of the first half of 2022.

According to data from counterpoint, in the fourth quarter of last year, global mobile phone sales fell by 6% year-on-year, and domestic sales fell by 11% year-on-year.

Except for Honor, the market share of all mainstream manufacturers has shrunk to varying degrees. Among them, OPPO and Huawei are relatively serious, losing 4.1% and 2.6% of the market share respectively year-on-year.

The sales crown vivo dropped from 21.1% in the same period last year to 19.8%, a year-on-year decrease of 1.3% of the market share, with the strongest “resistance ability”, followed by Xiaomi, which dropped from 16.6% to 14.9%, a decrease of 1.7%.

In the first half of the year, sales of smartphones in the Chinese market were about 136 million, almost back to the level of seven years ago. However, the general trend is not dominated by manufacturers, and it will be unavoidable for mainframe manufacturers to spend the darkest moment in the search for breakthroughs.

The market enters a period of burnout

The mobile phone market in the first half of the year can be summed up in one sentence: manufacturers compromise and consumers are tired.

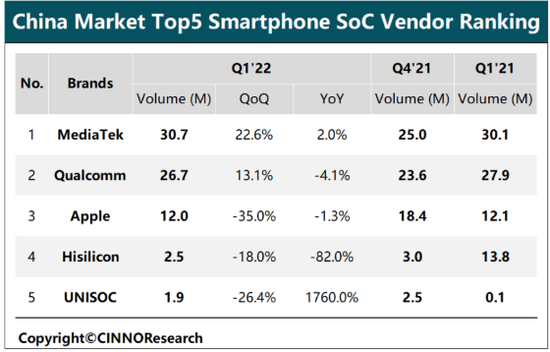

As the core of smart phones, chips have always been the key word in the industry, which has restrained the actions of host manufacturers to a certain extent. Last year, MediaTek accounted for 24% of shipments, and Qualcomm accounted for 34%. In the first half of this year, it became 42% and 35.3%. The structure of the SoC industry has changed, and host manufacturers are still in the adaptation stage.

After the launch of the Dimensity 9000 in March, the Android flagship model adopted a dual-SoC strategy for the first time, but the models equipped with Qualcomm 8 gen 1 are more expensive than the Dimensity 9000 models, and the theoretical performance gap is slightly higher than that of the Dimensity 9000. In actual use, the perception is not strong, and the latter has more advantages in heat control.

However, Qualcomm’s toothpaste squeeze has caused the manufacturer’s pricing to be out of touch with consumers’ perception, affecting the sales of some 8 gen 1 models, and consumers even questioned the manufacturer’s strategy for flagship pricing.

In the mid-end market, the theoretical performance of Qualcomm’s latest 7-series processors is slightly lower than that of its predecessors, and the Dimensity 8100 takes advantage of the situation. Pretty much repeats the story of the flagship line.

The more serious problem is that the actual performance of mid-range SoCs in the first half of the year can meet most of the performance needs of most users, which reduces the attractiveness of high-end SoC flagship phones, which indirectly leads to a drag on Android manufacturers’ branding process.

This year, the flagship products of many mobile phone manufacturers have reached higher price points, and the ensuing diving rate is also greater than in previous years. Taking the official website price of OPPO FIND X5 Pro as an example, it was listed in early March and announced a price reduction of 1,000 yuan in early June.

There are also those whose official website prices remain the same, and e-commerce platforms have small discounts, such as the vivo X80, which was launched in April. The main factor for its price stability is the unique product strength and reasonable pricing, but this kind of situation is rare.

Under the background of the current rare revolutionary innovation, the “premium” of products is a relatively common phenomenon, but the degree is different. Product iterations with no obvious upgrades have become routine, and new consumption stimulation points are difficult to emerge, which is also one of the important factors for consumers to be “tired”.

As a concentrated consumption node, the domestic mobile phone sales of 618 dropped by 10% this year, still failing to reverse the overall trend of the industry, and consumers’ willingness to purchase phones has dropped significantly.

The most direct impact of the increasing downward pressure on the global economy is the decline in consumer purchasing power. In April, the global inflation rate reached 7.8%. The IMF data pointed out that the inflation rate of 112 countries in the world is higher than 6%. The weak consumer side is difficult to achieve in the short term. Change.

As of the end of June, domestic 4G users still accounted for 73.2%. In practice, 4G can meet the needs of most scenarios. However, the actual advantages of 5G cannot be realized in the short term. machine target.

According to data from counterpoint, the average replacement cycle of users was 22 months in 2018 and 18 months in 2016, and has now risen to 31 months. The extension of the replacement cycle directly affects the overall sales of the mobile phone market, while the number of products sold more serious injuries.

The economy is down, the market is saturated, consumer demand is slowing, and there is no new stimulus on the supply side. To survive this unprecedented severe winter, mainframe manufacturers can only take the initiative.

Differentiation is still the core muscles

In 2007, the global mobile phone shipments reached 1.12 billion units. With the introduction of the iPhone 3G and HTC G1 successively, the era of smartphones has come. In 2010, the global mobile phone shipments rose to 1.6 billion units. Substantial product innovation has an immediate effect on the market.

Since entering the era of smartphones, manufacturers have focused on regular upgrades such as the supply chain CPU, screen material, and iteration of camera sensor components, and the differentiation of each brand has gradually blurred.

This does not cause too serious consequences in the incremental market, but it obviously does not work in the stock market.

In the first half of the year, mobile phone manufacturers were hindered by a series of subjective and objective factors, but the fact that the stock market was limited cannot be changed. Expanding the high-end market share is still a long-term goal, and differentiation has become the decisive factor.

From the past, Huawei has teamed up with Leica and self-developed Kirin to achieve the ultimate brand differentiation, and has eaten the high-end market cake before other domestic manufacturers. After Huawei took over the baton of vivo, its long-term emphasis on innovation has released good results.

In the first half of the year, vivo launched the X80 series, which is equipped with the self-developed new-generation independent image chip V1+ and micro-cloud platform. It became the most popular model in the 3500-5000 price range in the second month after its launch;

iQOO launched the 9 series, equipped with a new generation of full-sensing operating system, which is clearly differentiated from competing products, and the online sales exceeded 100 million yuan in 10 seconds.

Honor also tasted the sweetness. By inheriting Huawei’s imaging strength and Hongmeng system, Honor mobile phone also absorbed certain product differentiation and became the only domestic mobile phone brand that expanded its market share in the first half of the year.

This year, efforts in a single field cannot alleviate the anxiety of manufacturers, and fast charging is still a battleground for various players. The charging attack rate of the domestic flagship phone is almost over 80W. Xiaomi put 120W on the 12Pro, and iQOO, a sub-brand of vivo, has made the same attack rate standard for the 9 series, and even launched 200W on the latest iQOO 10 Pro. Super fast flash charge.

Half an hour from empty to full power has become the basic configuration of the flagship machine, and most of the low-end models are upgraded to 40-60W. In the first half of the year, the competition in the field of mobile phone fast charging was fierce. In the second half of the year, with the launch of vivo’s 200W ultra-fast flash charging, mobile phone charging officially entered the 10-minute era.

There is no doubt that the new differentiated track is unfolded by the folding screen. Last year, some folding screen products began to appear. However, the supply chain technology is not mature enough. Most of the products that are rushed to the market have common problems such as obvious creases, disparity in internal and external screen parameters, and insufficient durability. The significance of the manufacturer’s position is greater than the actual product strength.

With the technological iteration and the improvement of manufacturers’ own designs, the folding screen models that debuted in the first half of this year have substantially improved the previous common problems in the industry, and sales have ushered in a qualitative change.

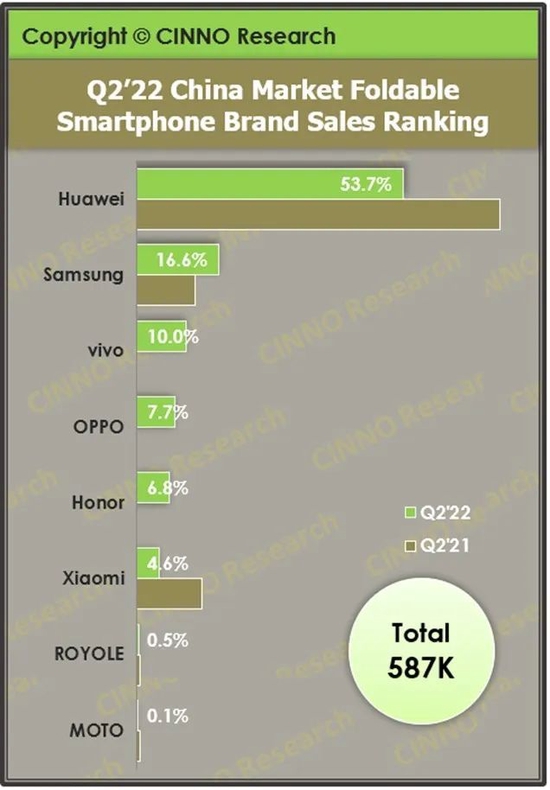

According to data from CINNO Research, the cumulative sales volume of domestic folding screen mobile phones in the first half of the year was 1.3 million units, exceeding the 1.16 million units in 2021, and the year-on-year growth rate in Q2 was 132.4%.

Although the overall sales of folding screens did not take off completely in the first half of the year, it is worth paying attention to the “independent thinking” of manufacturers outside the technical iteration of the supply chain.

Following Samsung’s idea of using traditional flip phones to eliminate the discomfort that may be caused by entering the era of folding screens as much as possible, OPPO FIND N can also maintain a relatively small product form after being unfolded. ‘s first shot.

Compared with other manufacturers that brought folding screen products to the market last year, vivo, which was full of innovation in the past, did not launch its first folding screen mobile phone X Fold until mid-April this year.

Its price is controlled within 10,000 yuan, which not only brings hinge innovation, consistent internal and external screen parameters, but also maintains the same Zeiss image configuration of the X80 series. Vivo explained the reason for “lateness” with its product strength, and also led the folding screen mobile phone to the 2.0 era.

Counterpoint expects that the sales of folding screen mobile phones in the Chinese market will be 2.7 million this year. The folding screen market will heat up rapidly, and the opportunity will be reserved for those who have a calm thinking about the market.

In the first half of the year, there were many bright spots in the overall decline in the mobile phone market. Various manufacturers have increased their efforts to build brand differentiation. Although the degrees are different, they have demonstrated their determination to change in the gradually deteriorating market environment.

Who will stand out in the second half

In the first half of the year, the best sales of domestic high-end models were the iPhone 13 series, and Apple, which regularly releases new models in September, will make the battle for the high-end market in the second half of the year more intense.

The folding screen is now a mature product. In the second half of the year, domestic mainstream manufacturers will continue to use the current dual flagship strategy: candy bar + folding screen to counter the impact of iPhone iterations on the market.

Although vivo and oppo introduced folding screen products to the price of 8,000 or 9,000 in the first half of the year, which has dropped significantly compared to last year’s mainstream products, the newly released Xiaomi MIX Fold is still at a similar price and has not lowered the price further. .

In addition to not threatening its own candy bar flagship sales, it also released two signals: first, the supply chain cost of Q3 folding screen products will not be significantly reduced, and second, manufacturers give up price wars and pay more attention to brand image.

Manufacturers need to seek another breakthrough in product strength, so that software and hardware can keep up with new product forms, and outside the supply chain, find the foundation of their own folding screen products.

This is actually a competition of R&D and innovation capabilities. Although domestic mainstream manufacturers have attached great importance to this aspect in recent years, the top ones are still Huawei and vivo, which focused on this earlier.

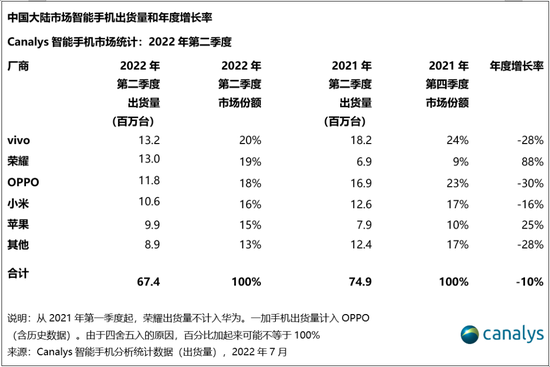

Huawei self-developed Kirin and Hongmeng, and has won and lost with Apple and Samsung all year round. Huawei, which is experiencing a low ebb, only got a 6.9% market share in Q2. The reasons are well known, but its R&D and innovation achievements have not been left out by the market: Honor’s market share in Q2 was 18.3%, second only to vivo, which was 19.8%.

The vivo APEX concept machine has introduced smartphones into the era of full-screen display. In recent years, innovative technologies have been launched continuously, such as V1+ independent image chip, micro-cloud platform anti-shake, etc., which directly hit the pain points of users. Every time it steps on the air, its innovation seems tricky, because vivo has long chosen to pursue pragmatism with user thinking.

The Central Research Institute, which was established last year, will play a unique role as a “technology beacon” in a market that is paying more and more attention to R&D and innovation strength.

At present, it seems that the major innovation of folding screen products in the second half of the year may not lie in the supply chain, but in the manufacturers themselves. In the head-to-head confrontation with the iPhone 14, vivo is undoubtedly the seed player, and Honor will not be left behind.

The support for manufacturers to hit the high-end is the steady flow of other product lines, and the guarantee lies in both online and offline channels.

Online, almost all mainstream manufacturers cover the main positions. It is difficult to say who has the absolute advantage. Offline, the situation of each manufacturer is different, or it is the decisive factor for their final results in the second half of the year.

The first is the quantity. At present, vivo has the largest number of offline sales outlets in China, with more than 250,000, followed by about 200,000 OPPO, over 30,000 Honor, and both Xiaomi and Huawei over 10,000.

The offline channel ideas of vivo and OPPO are relatively similar, with direct sales and authorized stores running in parallel. This year, the two companies accelerated the pace of their directly-operated stores entering shopping malls, creating more room for growth in high-end sales in the second half of the year.

In addition, the two have a large number of authorized stores distributed in the sinking market, which is an absolute guarantee for the volume of low-end and mid-range models. The offline channel ideas of Honor, Xiaomi and Huawei are as follows: focus on shopping malls and focus on high-end sales.

However, the three channels for the sinking market are relatively sparse, and the volume of mid-to-low-end models is relatively unfavorable. Similarly, in the face of the iPhone 14, the final results of each company will be very different.

At the same time, affected by the overall decline in the mobile phone market and the decline in consumer purchasing power, the overall sales of high-end models in the second half of the year are likely to continue to decline. At this time, the strength of each brand in the sinking market will play a more critical role.

write at the end

The first half of the year has passed. Although the overall trend of the domestic mobile phone market is declining, there are still many bright spots: the folding screen has begun to mature, and the “independent thinking” of manufacturers has increased. In terms of differentiation and innovative R&D, manufacturers generally pay more attention than previous years.

As the international situation stabilizes, the downward pressure on the economy is released, and the purchasing power of consumers recovers, the market will recover again, and manufacturers who can seize more markets by then must be well prepared.

Today’s severe market situation may be the best soil for incubating innovation.

This article is reproduced from: http://finance.sina.com.cn/tech/csj/2022-08-22/doc-imizmscv7280144.shtml

This site is for inclusion only, and the copyright belongs to the original author.