Source: Zhitong Finance

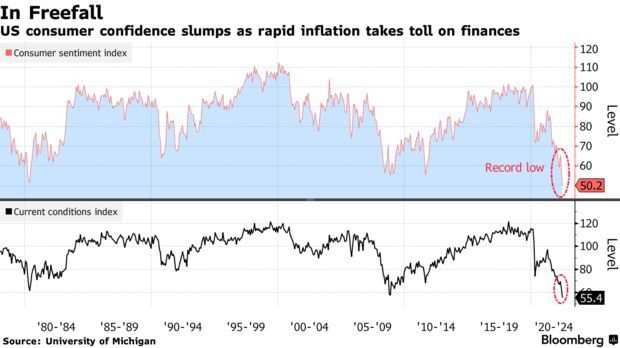

At a time when inflation is hitting another 40-year high, Fed Chairman Jerome Powell is facing an increasingly dire consideration: He may have to push the economy into recession to get inflation back under control.

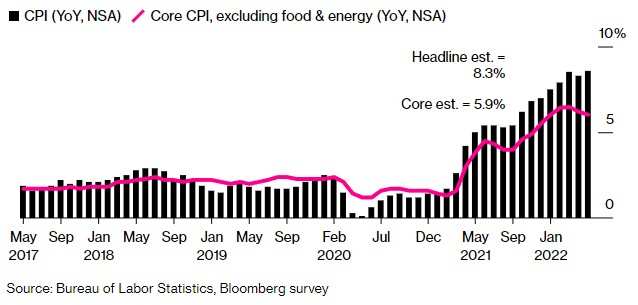

Zhitong Finance APP was informed that last Friday, data released by the U.S. Bureau of Labor Statistics showed that the U.S. CPI rose 8.6% year-on-year in May, further accelerating from 8.3% in the previous month, hitting a new high since December 1981, higher than market expectations. 8.3%; May CPI rose 1% month-on-month, higher than market expectations of 0.7% and the previous month’s 0.3%. In addition, the core CPI, excluding food and energy, increased by 6.0% year-on-year and 0.6% month-on-month, both higher than expected.

U.S. headline CPI and core CPI both beat expectations in May

U.S. recession risk rises

Rampant inflation has put Fed Chairman Jerome Powell at the forefront. Powell, who for much of last year looked a bit like the inflation-tolerant ex-Fed Chairman Arthur Burns, is increasingly playing a Paul Volcker-like role these days. The role of the “inflation killer”.

So far, Powell has not commented on the possibility of more aggressive monetary policy or a severe recession. Four decades ago, Volcker beat inflation after implementing aggressive monetary tightening at the cost of two recessions. Powell has recently acknowledged that it may take some pain to control inflation and that unemployment could even rise, but he has avoided talking about a recession.

That’s perhaps understandable, especially ahead of the US midterm elections in November. “Powell doesn’t want to say the word ‘recession’ in a positive way, like ‘we need a recession,'” said Alan Blinder, former vice chairman of the Federal Reserve. “But he’s going to use a lot of euphemisms in place of it. .”

A growing number of economists, including Alan Blinder, say a contraction in the economy and rising unemployment may be needed to bring inflation down to a more tolerable level, let alone back to the Fed’s 2 percent target.

A survey of economists showed a one-in-four chance of a recession this year and a three-in-four chance next year. “A recession in 2022 is unlikely, but a recession in 2023 will be hard to avoid,” they said.

“I’m becoming more pessimistic about the chances of stabilizing inflation at acceptable levels without a recession,” said Bruce Kasman, chief economist at JPMorgan Chase & Co. He believes that a prolonged period of high inflation and a tight labor market will lead to wage demands Rising and business costs are rising, this is a dynamic development trend.

Inflation at the highest level in 40 years sent Treasury yields soaring on Friday while U.S. stocks tumbled. Investors worried that the Fed would step up monetary policy tightening, raising bets for a 50-basis-point rate hike at the Fed’s July and September meetings. Some economists believe a 75 basis point rate hike is already on the table.

Could Fed inflation target rise to 3%?

The path and destination of interest rates in the coming months will depend in part on how quickly and how much policymakers want inflation to cool, and how much pain they are willing to inflict on the economy to get there.

Ethan Harris, head of global economics research at Bank of America, said the Fed may be willing to compromise, accept stabilizing inflation at 3 percent and consider gradually addressing overshoots over time, which would allow it to avoid pushing the U.S. economy into recession .

Olivier Blanchard, a former chief economist at the International Monetary Fund (IMF) and now a senior fellow at the Peterson Institute for International Economics, bluntly said the Fed had “blundered” and caused inflation to spiral out of control. He said the Fed should stop tightening monetary policy and make it the new inflation target when inflation falls to 3%, rather than risk a recession by cutting it to 2%.

However, the longer inflation remains high, the more likely it is to become entrenched in the economy. That’s what happened when Burns was Fed chairman in the 1970s, and it’s the main reason Volcker later had to put the economy through such a big test to bring down inflation.

Alan Blinder said there are also dangers in taking overly aggressive action against persistent inflation, which could tip the economy into a very deep recession and send unemployment soaring. He said the Fed must balance the risks between controlling inflation and a recession.

However, Deutsche Bank economist Peter Hooper believes that if the Fed abandons its 2% inflation target, it would be a “Burnsian” mistake, and Powell does not want to make such a mistake. Powell, at least for now, has what Burns doesn’t have, the political support he needs to act against inflation, he said.

edit/somer

This article is reprinted from: https://news.futunn.com/post/16356430?src=3&report_type=market&report_id=207941&futusource=news_headline_list

This site is for inclusion only, and the copyright belongs to the original author.