The recent talk show house jokes have brought fire to the stock market again.

Investing in a family of “full-time stocks”, to achieve the ultimate goal of life “buy it for a two-bedroom and one-bedroom”, “annualized rate of return of 46,000%”, “that’s what Buffett is all about”, in just 2 minutes, I almost hit it The core pain point of retail investors.

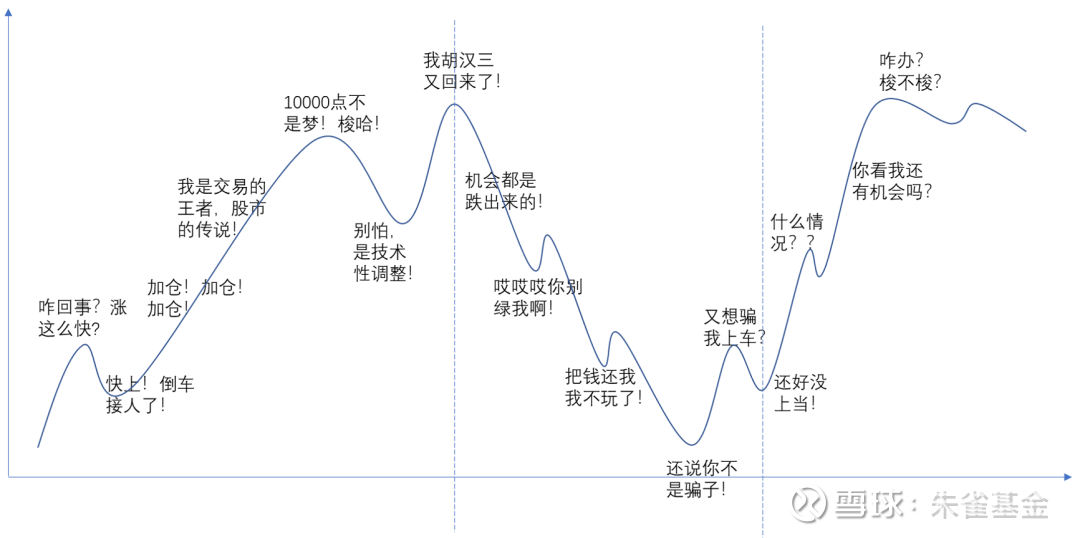

In line with the roller coaster market that fell from a high level, quickly rebounded, and fell again, investors who were caught off guard laughed and burst into tears.

House’s joke accurately describes the mentality of retail investors from skyrocketing to plummeting, from “Buffett is just like that” to “return the money to me, I won’t play anymore”, it may only be 2 months before and after.

Source: Produced by Suzaku Foundation

As many fans as this 2-minute talk show has, there may be as many retail investors as 120,000 to 25,000 behind it. All artistic creations come from life, only retail investors understand the mood of retail investors the most. There is so much sadness behind a joke about turning off the lights and eating noodles.

In fact, the number of Christians has far exceeded the number of shareholders. By the end of 2021, there were more than 197 million individual stock investors in China, and more than 720 million fund investors, of which nearly 700 million were natural person investors in public funds.

However, this does not affect the spread of greed and fear among investors, nor does it affect investors losing money. Jimin’s mental journey is almost the same as that of investors. Studs at high points, meat cuts at low points, hesitating in shocks, changing positions in rotation, never leaving the market, and being repeatedly harvested.

Especially when the market is falling continuously, it is particularly difficult, but the rewards of surviving and even daring to increase positions against the trend are particularly rich. For example, if the market low point in April this year is over, it will soon usher in a rebound of more than 20%.

From the current point of view, the decline in the first quarter is a small wave. Looking at the current wave of decline three months later, it may be the same. Take the photovoltaic new energy industry as an example, the fundamentals have not changed, the global consensus on carbon neutrality still exists, and the short-term demand is still growing rapidly, but the staged overestimation brought about by the group will take some time to digest.

Investors get very nervous once the market starts to fall. From past experience, no matter the time to digest the valuation or the time to rebound from oversold, it is much faster than the market expected. Selling now, it is very likely that it will be too late to increase the position when it rebounds, and then go short, and then chase the high.

If it is determined that the fund managers held are excellent and the fundamentals of the industry have not changed, it may be more important for investors to control the urge to cut meat at low points.

There are two reasons why Christian Democrats lost money. First, they chose the wrong fund. Second, they bought high and sold low.

Choosing the wrong fund is actually a very common reason, similar to stock stepping on thunder. Under the long-term investor education of the entire industry, some Christian Democrats have accepted the concept of long-term investment. But if you are unfortunate enough to buy the worst-performing fund at a high level, you may still lose money if you hold it for a long time.

In terms of probability, most investors choose a fund that has a much greater chance of winning. The professionalism of fund managers and the diversification of investments also reduce the risk of stepping on thunder. This is also the reason for the rapid expansion of public funds.

It is difficult for investors to know the income of a fund after buying it. This year’s champion fund may be at the bottom next year, and this year’s bottom base may become the champion next year. Short-term performance cannot reflect the level of fund managers.

Some indicators can help investors understand fund managers, such as how long the fund manager has investment experience, whether it has crossed the bull and bear market, whether it has its own investment framework, whether the annualized return for more than 3 years is ahead of its peers, and whether there is a return that exceeds the market. Whether the retracement is well controlled, whether there is a high professional ethics, and whether it will prompt risks at a high point.

These are clichés that are easier said than done. Some investors take a month to buy a house, but it may only take a minute to buy a fund, which is a large part of the reason for the loss. Therefore, it is important to have a checklist of investments and add due diligence to the list.

Excluding some very bad funds, on the whole, public funds are actually very good leverage. Leverage can be roughly divided into three categories, the first is capital, the second is manpower, and the third is the influence of the Internet. The biggest lever that ordinary people can use in the past is to take out a loan to buy a house, but they ignore that public fund managers are also a kind of leverage.

The fund manager has thousands of troops and horses to cross the single-plank bridge. He has been studying hard for more than ten years in the cold window. He is the king of the paper among his peers. However, investors only need to pay 1,500 yuan to buy 100,000 yuan of funds, which is 125 yuan a month. Money, buy 200M broadband for 180 a month. Few investors may have noticed that many products managed by private equity bigwigs have bought public funds.

On the contrary, some things that look cheap are actually very expensive, such as stocks. The commission for stock trading is 2.5/10,000, which seems to be very cheap, but the proportion of investors who lose money may be very high. As in the house’s joke, it is not uncommon for 120,000 to 25,000.

Buying at the highs and cutting at the lows is another reason to lose money. At this time, the old guys who have experienced the battle have to be moved out of the town. Charlie Munger said that we make money when we buy. Buying cheap enough is the key to profitability, and sometimes it has nothing to do with mentality.

Take a simple example, buy a stock for 10 yuan, rise to 20 yuan, and then drop to 15 yuan, still floating profit of 50%, and the mentality is very stable. If you buy a stock for 20 yuan, and then drop to 15 yuan, you will lose 25% when you enter the market, and your mentality may collapse directly. It may be the same person who made these two investments, and his personality has not changed before and after, but the margin of safety has affected his mentality.

Risks come up and opportunities come down. Therefore, don’t be nervous when the market falls, and when the market continues to rise rapidly, it may be the time to worry.

Buffett once said that our self-confidence comes not only from our own past experience, but also from our clear understanding of society. The best way to reduce risk is to think.

Many investors believe that if you want to buy cheap, then of course you have to choose the time. This is very difficult for investors. Even the best fund managers can only roughly know their position in the market and choose the timing of some large positions when the macro economy changes. The exact timing cannot be selected.

Even Keynes, the grandfather of macroeconomics, admits he can’t do it well. Keynes once said, don’t try to grasp the operation of the whole market, try to find the company you understand. This emotion stems from his own painful lessons.

In the 1920s, when Keynes started investing, he preferred to judge market trends by predicting the macro economy. On the eve of the Great Depression in 1928, when global markets began to reverse and prices fell, Keynes was still buying long contracts on rubber, wheat, cotton, tin and more. After the stock market crashed in 1929, Keynes nearly went bankrupt with a net loss of 80%.

Investment approaches that have attempted to predict economic trends and link forecasts to currency and commodity trading have largely failed. Since then, Keynes’s investment philosophy has switched from top-down to bottom-up, from short-term speculation to long-term investment based on company fundamental analysis, buying stocks of companies that, in his opinion, will survive the crash and holding them for the long term. Have.

Although it is difficult for good managers to grasp the secret of timing, good managers will prompt risks when the market is high, or when the scale exceeds their management capabilities, such as suspending the subscription and opening the subscription when the market is low. Help Christians buy cheap.

Therefore, for the Christian Democrats, it may be more useful to think about whether the managers have sufficient investment ability and whether they are considering the interests of the Christian Democrats, rather than where the market is now.

Only deep understanding can bring deep trust, and deep trust can bring about mental stability, and then obtain long-term benefits.

Similarly, as far as managers are concerned, investor education is not about pouring chicken soup when the market falls, but through the communication of long-term investment ideas and analysis of investment methods, to popularize investment knowledge to investors and attract suitable investors. investor.

It may be more meaningful for managers to make people who like us like us more than to make more people like us.

The interests of investors and managers are highly bound. In the long run, only by earning money for investors can they win the trust of investors, and then have the opportunity to continue to manage assets for investors.

There are already more than 140 public fund companies and more than 3,000 public fund managers in the A-share market. There are not a few fund managers who have passed through the bulls and bears, and the new generation and the Mesozoic are not necessarily inferior to the veterans.

In an era when fund managers are no longer scarce, making money for investors is the core competitiveness, which is also the original intention of the development of public funds.

The market has reached a difficult period again. Only investors and managers who understand each other and trust each other can go through the most difficult period together.

Note: This document is not a fund promotion and promotion material, and is only one of the customer service matters of the company’s funds.

Any information provided in this document is for readers’ reference only, and does not constitute an inevitable basis for future investment decisions of funds managed by the company, nor does it constitute any substantive investment advice or commitment to readers or investors. The company does not guarantee the accuracy and completeness of the text and data contained in this document, and does not assume legal responsibility for any third-party investment consequences arising therefrom. Funds are risky and investment should be cautious.

The opinions contained in this article are only opinions and judgments on the date of this article. At different times, Suzaku Foundation may issue opinions that are inconsistent with those contained in this article. Without the written permission of Suzaku Foundation, no institution or individual may forward, reproduce, reproduce, publish, publish or quote all or any part of this article in any form.

This topic has 5 discussions in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/2344429401/230814807

This site is for inclusion only, and the copyright belongs to the original author.