On March 25, when the media broke out that Dan Bin was short-selling.

I made a post that caused quite a bit of discussion on Snowball.

The reason is very simple, I think that because of WW3 expectations, the reason for being bearish is not sufficient.

In addition, the high position is full and the low position is cleared, which is not in line with what he often calls “the rose of time”, a typical style drift.

Interestingly, since Shanghai in April did not predict, the market did drop a wave, and there were many voices to praise but Bin got it right.

However, these admirers overlooked a point, but when Bin started to clear the warehouse, there was no such thing as Shanghai, so this is completely two issues.

Recently, Dan Bin liquidated A shares and bought US stocks.

Missing the rebound of the A-share market, and seeing the decline in the US stock market , once again stood on the cusp of the storm, and was bombarded by investors.

This time, I think he did the right thing, but it was a more courageous act.

Because, in my opinion, buying U.S. stocks right now is indeed the most cost-effective value investment .

In fact, investing in the stock market is similar to buying a house and buying assets. There are many factors that affect the cost-effectiveness of an investment.

But the key point is to see whether it is expensive to buy (whether static valuation is high or not), good or not (asset quality , good growth) , and whether there is excess return (market valuation level improvement space , monetary policy space).

Therefore, we can look at the basic situation of the U.S. stock market , Hong Kong stock market , and A-share stock market from the perspectives of valuation level , growth , and excess return.

-01-

U.S. stock valuations are at a 10-year low, with the best growth in the world

1. First of all, we need to answer a question, are U.S. stocks expensive (static valuation)?

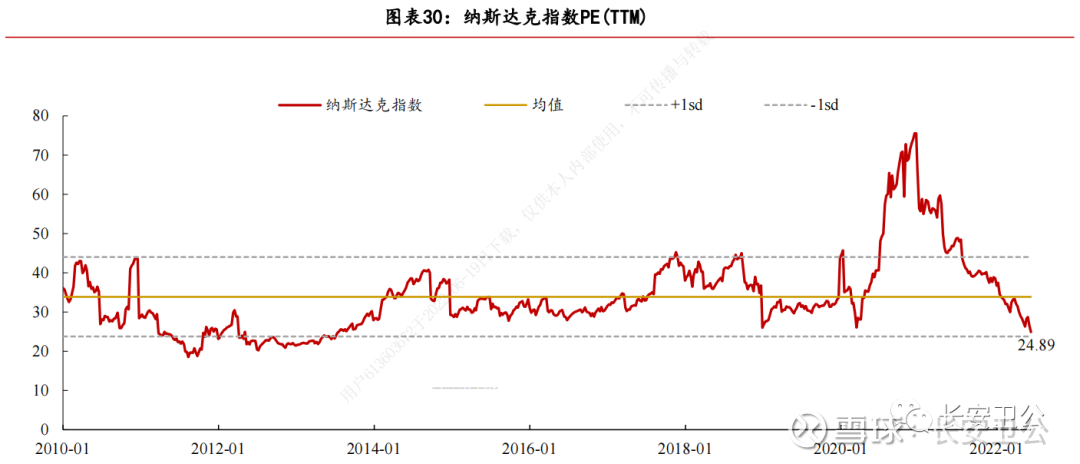

From the perspective of static valuation, the current price-to-earnings (TTM) ratios of the US stock Nasdaq Index, Dow Jones Industrial Index, and S&P 500 Index are 27.6 times , 20.33 times , and 19.91 times, respectively. It is lower than the time points of 81.08%, 41.73% and 69.56% in the past ten years, respectively.

In general, it is considered that the index quantile below 30% is underestimated, 30% to 60% is reasonable, and over 60% is overestimated:

(Data source: ifind, 2012/06/13~2022/06/16)

Therefore, from the current point of view, the Nasdaq Index, the Dow Jones Industrial Index , and the S&P 500 Index are at the undervalued, reasonable and undervalued levels, respectively, and the overall valuation level of US stocks is undervalued .

2. Secondly, whether the U.S. stock market is good (asset quality, growth)?

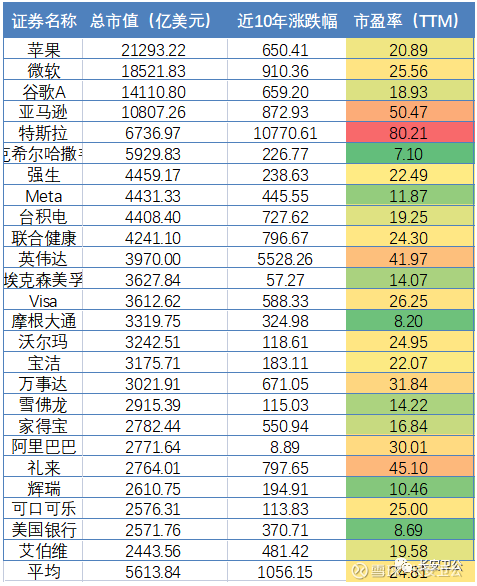

From the perspective of asset quality, the heavyweight stocks in the United States are mainly composed of Apple, Microsoft, Google, Amazon, Tesla, Facebook, Johnson & Johnson, Procter & Gamble and other technology, pharmaceutical, and consumer companies. The 25 largest companies in the United States have nearly 10 years. The rise and fall were as high as 10.6 times.

Whether it is the Internet from 1995 to 2000; consumer electronics from 2005 to 2015; new energy vehicles from 2010 to 2022 ; Growth is the world’s first.

(Data source: ifind, 2012/06/16~2022/06/16)

Driven by leading companies in the US stock market, the stock markets in the related technology , consumer and pharmaceutical industries also performed very well.

Therefore, in terms of growth, thanks to the entrepreneurial atmosphere of attracting top global talents and Silicon Valley companies, the growth of US stocks is very good.

3. Is there any excess return on the US stock market?

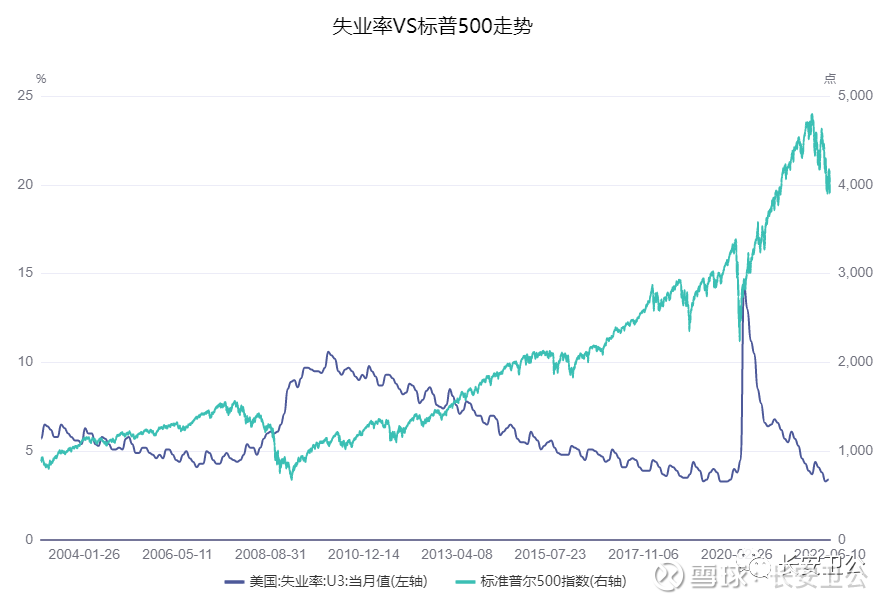

From the historical trend of U.S. stocks, economic conditions and monetary policy are the most important reasons for affecting the trend of U.S. stocks, and the unemployment rate has a significant negative correlation with the S&P 500 index, that is: the better the economy, the lower the unemployment rate, the lower the U.S. stocks (S&P 500). 500) the better the rally.

(Data source: ifind, 2012/06/13~2022/06/16)

Since the beginning of this year, there have been many adjustments in US stocks, mainly due to the rise in commodity prices, which has driven the US CPI to continue to grow .

(Data source: ifind, 2012/06/13~2022/06/16)

This has put a lot of pressure on the valuation of U.S. stocks, the most obvious being that the equity market has had a relatively significant impact.

However, judging from the trend of U.S. Treasury bond yields in the past 10 years, the background of U.S. bond yields continuing to rise is high energy inflation + the U.S. economy is still strong.

Therefore, although the current interest rate is relatively high, if the conflict between Russia and Ukraine subsides, there is a possibility of a decline in the medium term, and high-tech growth stocks in the United States are also expected to usher in a round of valuation repair process.

After all, the valuation of Nasdaq, this round has basically reached the lowest point in nearly 10 years, and it is too low…

Some people also said that U.S. stocks are now in the water-receiving stage, while the domestic market is in the water-releasing stage, and the cost-effectiveness of investment is different.

However, from a longer perspective, water release is the main theme. Moreover, the long-term bond spread between China and the United States cannot be inverted too much.

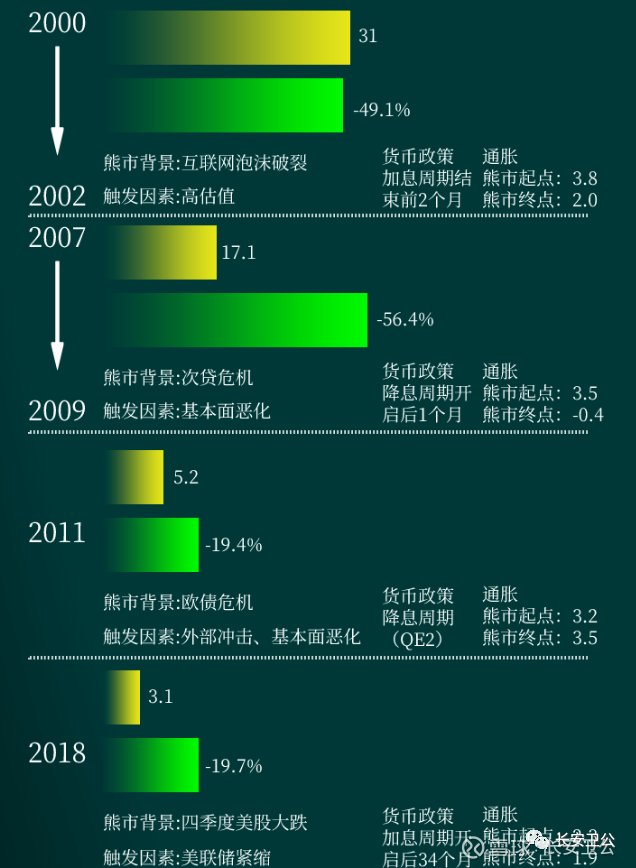

Regarding U.S. stocks, in fact, the S&P 500 has pulled back 23.7% in this round, and the Nasdaq has pulled back 33.4% from its highs.

Judging from the magnitude of the decline, the current bear market decline has reached the median level of the bear market decline in U.S. stocks since the 21st century, surpassing those in 2011 and 2018 .

In 2000 and 2007, the sharper declines occurred due to economic crises .

I can’t judge how likely this is, you can judge for yourself.

(Source: Huawen Futures)

In addition, from a technical point of view, the Nasdaq 10,000 is superimposed on the 60-month line, which has not fallen below it in the past 13 years.

10,000 is a strong support line for the Nasdaq and is also very likely to form a mid-term bottom.

-02-

The vertical valuation of Hong Kong stocks is not cheap, and the growth is poor

1. Let’s take a look at whether Hong Kong stocks are expensive (static valuation)?

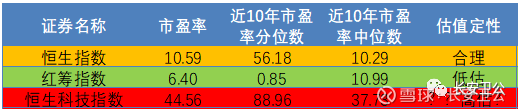

From a static valuation point of view, the current price-earnings ratios (TTM) of the Hang Seng Index , the Red Chip Index and the Hang Seng Technology Index are 10.59 times , 6.4 times , and 44.56 times, respectively.

It is lower than the time points of 43.80% , 99.15% and 10.04% in the past ten years, respectively.

In general, it is considered that the index quantile below 30% is underestimated, 30% to 60% is reasonable, and over 60% is overestimated:

(Data source: ifind, 2012/06/13~2022/06/16)

Considering the fact that the Hang Seng Technology Index as a whole should be at a reasonably low level due to the decline in profits and the distortion of the price-earnings ratio due to domestic Internet regulation.

The current valuation of Hong Kong stocks should also be at an overall reasonably undervalued level.

2. Is the Hong Kong stock market doing well now (asset quality and growth)?

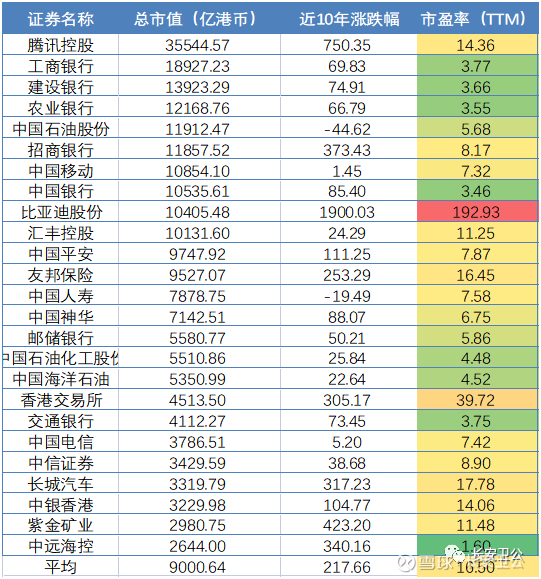

From the perspective of growth, before 2018, most of the heavyweight stocks in Hong Kong were leading companies in traditional industries such as energy, finance, and insurance, with poor growth.

On April 30, 2018, the amendments to the Main Board Rules of the Hong Kong Stock Exchange came into effect, lowering the listing threshold for three types of companies listing in Hong Kong, namely: companies with weighted voting rights structures; biotechnology companies; proposed secondary listing ‘s company .

This has led to a large number of leading Internet companies in biomedicine, such as Alibaba, JD.com, Meituan, Innovent Bio, Kangfang Bio, and BeiGene, etc., to accelerate their listing on Hong Kong stocks in recent years, enhancing the growth of Hong Kong stocks.

However, on the whole, the growth of Hong Kong stocks is still slightly lower than that of US stocks and A shares.

(Data source: ifind, 2012/06/13~2022/06/16)

Judging from the growth rate in the past ten years, the same is true. The top 25 heavyweight stocks in Hong Kong stocks have an average growth rate of only 2.2 times in the past ten years, and most of the heavyweight stocks are financial enterprises. The growth rate is very slow, and the growth rate is seriously lower than that of A shares and US stocks. .

3. Do Hong Kong stocks have excess returns (space for monetary policy, room for valuation improvement)?

Since Hong Kong adopts a peg to the US, monetary policy is converging with US stocks. The Hong Kong stocks listed are all domestic companies, and their operating performance is mainly matched with the domestic economic situation, and it is generally difficult to have excess returns.

However, Hong Kong stocks can generally use the Hang Seng AH premium level to see the premium level relative to A shares:

The index center is around 130. Generally speaking, 150 Hong Kong stocks have excess returns, and 120 Hong Kong stocks have no excess returns relative to A shares, so currently Hong Kong stocks have excess returns, but it is not obvious.

-03-

The A-share indicator shows at the bottom, with better growth potential or excess returns

1. Are A shares expensive? (Static valuation situation)

From a static valuation point of view, the current price-earnings ratios (TTM) of CSI 500, CSI 300, and SSE 50 are 20.97 times , 12.60 times , and 10.12 times, respectively. It is lower than the time points of 89.38% , 46.77% and 45.31% in the past ten years, respectively.

In general, it is considered that the index quantile below 30% is underestimated, 30% to 60% is reasonable, and over 60% is overestimated:

(Data source: ifind, 2012/06/13~2022/06/16)

The current valuation of A shares is at an overall reasonably undervalued level.

2. Is the A-share market good (asset quality , growth)?

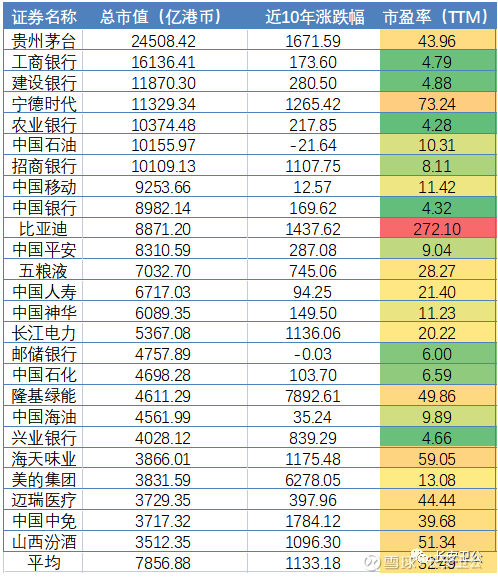

From the perspective of growth, A-shares have gathered the most domestic domestic listed companies.

Unlike Hong Kong stocks, which are dominated by finance , real estate , and the Internet, A-share companies have more evenly distributed industries, and the proportion of manufacturing and industry is significantly higher than that of Hong Kong stocks.

(Data source: ifind, 2012/06/13~2022/06/16)

Judging from the growth rate in the past ten years, the top 25 heavyweight stocks in A-shares have an average growth rate of 11.3 times in the past ten years.

Considering that the growth rate of listed companies in the first quarter was lower than that of US stocks, the actual growth rate of A shares was slightly lower than that of US stocks and higher than that of Hong Kong stocks.

3. Does A-shares have excess returns (space for monetary policy, room for valuation improvement)?

Domestic policies are independent, and we are currently in a channel of interest rate cuts as a whole. The main factors that suppress the profitability of A-share companies include the impact of the epidemic on the performance of listed companies , Sino-US relations , and the conflict between Russia and Ukraine.

(Data source: ifind, 2012/06/13~2022/06/16)

From the perspective of the price/performance ratio of stocks and bonds, the current CSI 300 earnings yield is about 3 times the yield to maturity of the 10-year treasury bonds. From the past situation, more than 3 times can successfully indicate the bottom of A shares. Therefore, A shares should also have excess returns.

-04-

Three market comparison conclusions: US stocks > A shares > Hong Kong stocks

To sum up, the price/performance order is: US stock market>A stock market>Hong Kong stock market

I also summarize the characteristics of the following three markets:

A. Brief introduction of the US stock market: US stocks have the best growth, the current valuation (vertical) is at an undervalued level, and most of the Fed’s interest rate hike expectations have already been Priced in. Judging from the employment rate data, the current economic momentum of US stocks is still good, there is a certain excess return, and US stocks are the most cost-effective.

Three words summary: high growth, long cattle verification, innovation driven

B. Brief introduction of the Hong Kong stock market: The static valuation of the Hong Kong stock market is very low, and the current valuation (vertical) is at a reasonably low level. Although a large number of Internet pharmaceutical companies have been introduced after 18 years, the overall financial and energy are still dominated, and the growth potential is relatively low. Poor, the excess returns are very small, and the current Hong Kong stock market is relatively cheap.

Three words summary: extremely undervalued (horizontal), emerging industries (Internet + medicine), high dividend yield

C. Brief introduction of A-share stock market: A-shares are difficult to predict due to the impact of the epidemic, and Sino-US relations are relatively tense. However, the price-performance ratio of stocks and bonds indicates that the current A-share market is in the bottom range and has better growth potential. The current A-share market price-performance ratio is average.

Three words summary: bottom area, technological growth, sharing development dividends

Therefore, it is actually no problem for Dan Bin to increase his positions in US stocks.

Because the sweetest piece of cake in investment is value + growth.

Compared with A shares and Hong Kong stocks, the moat of US stock technology companies is relatively high. Now you can easily see Tesla and AMD with better growth prospects in US stocks at a price of around 30XPE; facebook, AMD at a price in the early 10XPE Qualcomm, Google, TSMC; even the price of 5~6X, see Intel, HP. At present, the valuation of U.S. stocks is at a relatively low position, and the valuation of leading companies is not expensive, so you can focus on it.

$NASDAQ Composite Index(.IXIC)$ $Hang Seng Index(HKHSI)$ $CSI 300(SH000300)$

There are 115 discussions on this topic in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/3203620784/223022789

This site is for inclusion only, and the copyright belongs to the original author.