Welcome to the WeChat subscription number of “Sina Technology”: techsina

Source: bad review (ID: chaping321)

Recently, this payment model called “buy now, pay later” has become a mess in foreign countries.

And it is often abbreviated as BNPL (Buy Now, Pay Later).

Let’s just say that, according to data reported by Global Payments, 2% of the total global online shopping last year was paid for by BNPL.

Under this wave, a Klarna company from Sweden, which specializes in BNPL business, has quietly risen to hundreds of billions in valuation, becoming the largest unicorn company in Europe and the fifth largest in the world.

Even Apple, the big-eyed guy, announced its own “buy now, pay later” business Apple Pay Later at the recent developer conference.

It is no exaggeration to say that the BNPL business in the past two years has become an outlet for the crazy pursuit of foreign giants.

Seeing a lot of poor friends, most of them will say, isn’t this thing just lending? The big domestic factories have played a round for a long time, and the supervision has sorted out a wave of chaos. As for the foreigners, have they never seen the market?

In fact, this BNPL looks similar to domestic consumer loans at first glance, but it is quite different in form.

And today, the bad reviewer is going to talk to you about this “overseas Huabei” business BNPL, which is addicting to foreigners and has attracted giants to enter the game.

For example, the interest rate of credit cards in the United States is generally stable at around 15%, and the online loan platform ranges from 8% to 36%.

But no matter how perfect it is, for young people who apply for a credit card for the first time, it will take three or four days at the earliest. After the card is applied, most of them may have forgotten what they want to buy.

And the BNPL service saw this market, and it caught the group of young people who didn’t have credit cards.

Isn’t the credit card process long and slow to review?

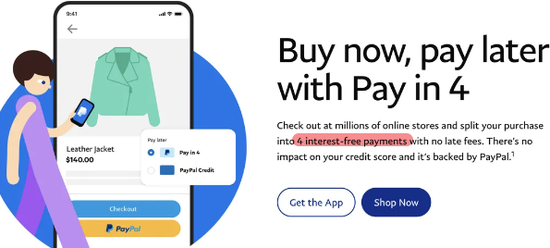

BNPL is the same as Ant Huabei and Baitiao, which are familiar to everyone. It is a quick word.

Take the Klarna platform as an example. After submitting your personal information and obtaining the quota, you can directly select the installment from the supported merchants.

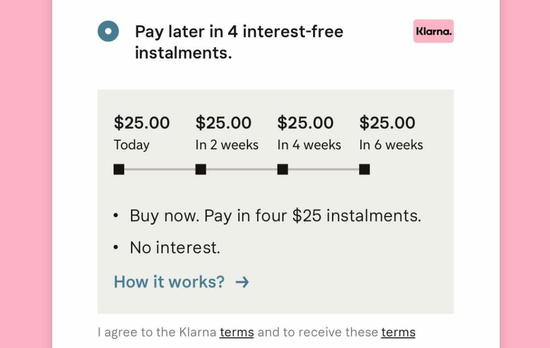

It only takes a few minutes from registration to final use.

Because the credit card has been repaid a few times less, and the discount on the mortgage cannot be reduced in the end, the bad reviewer has heard a lot of stories.

This wave of operations that does not affect the credit score can be said to reduce the burden on users.

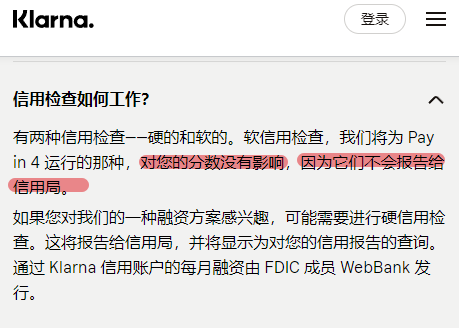

In addition to being reviewed as fast as consumer loans, BNPL’s fees are still lower, even lower than credit cards.

BNPL does not charge all the fees such as handling fees, management fees, annual fees, etc. that are common to credit cards. . .

What’s more, most BNPLs don’t even charge any interest. If you borrow 925 yuan, you will pay back a total of 925 yuan on time, and you won’t be charged a penny.

You must know that the real annualized interest rate of Huabei is about 15%.

But starting a company is not about giving money for charity. Since BNPL does not charge interest to borrowers, what do they earn?

The answer is actually very simple, because in turn, the merchants who use the BNPL service are asked for money. . .

When the user pays in BNPL instalments, the platform will directly transfer the full amount of money to the merchant’s account, and collect a commission of about 6%.

Take Klarna as an example. Commissions from merchants account for about 80% of their income. H&M, Nike, etc. are all its gold owners.

Young people who are willing to spend, and then lend them money to spend in the established stores.

It is normal for the platform to earn some handling fees because it attracts customers.

This point is very similar to Huabei, except that Huabei is a two-way smash, and only charges about 1% of the merchant’s handling fee.

The biggest difference between BNPL and Huabei and Baitiao is that Huabei provides financial services, and the money behind it comes from licensed consumer finance companies, which, like banks, are regulated by the China Banking and Insurance Regulatory Commission.

BNPL is not necessarily, people do not charge interest, whether this model is a financial service, in some countries, it is still up for debate. . . The sources of funding behind it may be varied and unregulated.

Anyway, according to Karna’s data, after using the BNPL service, customers buy more frequently and spend more money.

Maybe this is the legendary borrowed money that is better spent.

In this way, stores that support BNPL payment are more likely to attract the attention of the chopping party.

In the UK, more than half of young people have used BNPL, and one-fifth of the population in Australia has used BNPL.

The number of stores accepting BNPL payments is also increasing, and it is said that by 2030, the total size of BNPL will jump 40 times to $3.98 trillion. . .

So in addition to Apple, Amazon, which has its own mall, cooperated with BNPL platform Affirm to join this wave of lending.

For example, Microsoft has already cooperated with Quadpay and integrated the BNPL function on its own browser.

At that time, this wave of updates was also criticized by everyone as “not doing a proper job”.

On the user side, they are bombarded by BNPL advertisements. According to statistics, more than half of young Americans have seen BNPL on TikTok or Facebook.

Various promotion incentives are also emerging one after another, just like the feeling of the domestic and foreign sales and taxi subsidy wars.

This capital carnival made the poor reviewer want to sigh, the end of the Internet is indeed lending.

Because aside from those fancy business models, BNPL’s business is essentially lending to young people. Not to mention immorality, the risk alone is huge.

Coincidentally, because of this interest-free repayment model, BNPL has some legal loopholes.

For example, the “Credit Card Act” in the United States stipulates that it is forbidden to issue credit cards to young people under the age of 21, but BNPL is not under their control, so many young people under the age of 21 have become the main users of BNPL services.

In the past two years, in the United States alone, the number of young people using BNPL has increased by 300%.

Also in the UK and Australia, this set of interest models has more or less helped BNPL get out of some financial supervision, so that this set of things can take root and spread better.

But as the saying goes, what you owe is always repaid.

Australia’s FCA has conducted a survey and said that it found that 60% of the respondents were over-use of BNPL and were burdened with multiple BNPL bills, which affected their normal life.

Affirm, known as “Alipay in North America”, even started asset securitization and packaged up and sold various BNPL IOUs in its hands, hoping to allow the market to absorb some of the risk of bad debts. . . It can only be said that it is a bit like the subprime mortgage crisis.

As for the bad reviewer, I also checked to see if there is any comparable overseas BNPL model platform in China.

Finally, I found an app called “Watermelon Pay”, which just received financing from AfterPay, an Australian BNPL platform last year.

Whether this platform is easy to use or not, how is the current situation?

But what is certain is that this platform has now been targeted by some black businessmen who specialize in small loans.

A group of old brothers waiting to cash out are waiting to feed in the post bar.

However, whether it is risk control or regulatory compliance, there are still obstacles and long-term obstacles on a global scale.

Simply encouraging young people to overspend and overdraft future business will not go long.

After all, for those of us who have just experienced various P2P thunderstorms and fully cleared off non-compliant online loans, we have experienced many battles and have seen them a lot.

Written by: Jiang Jiang Editor: Noodles Cover: Xuan Xuan

Pictures, sources:

Everyone is a product manager. Why is BNPL used by Amazon and SHEIN?

China Economic Weekly, the end of technology is lending? Apple forms dedicated financial subsidiary for “buy now, pay later” service

Geek Park, no interest is charged when the account is received in one second, the “consumer loan” hollows out the “post-00s” in Europe and the United States

Everyone is a product manager, let’s talk about buy now, pay later (BNPL)

(Disclaimer: This article only represents the author’s point of view and does not represent the position of Sina.com.)

This article is reproduced from: http://finance.sina.com.cn/tech/csj/2022-06-15/doc-imizirau8517080.shtml

This site is for inclusion only, and the copyright belongs to the original author.