$Kweichow Moutai(SH600519)$ $Haitian Flavor Industry(SH603288)$ $Hengrui Medicine(SH600276)$

This is a summary that I originally wrote when I read Buffett’s letter to shareholders. After a few years, I look back and have a new experience.

Why is a shareholder letter a classic? The classic is that with the increase of experience, read it again and again and gain it again.

So, why is the free shareholder letter that anyone can download and view, but not many people want to read? It’s because no one appreciates it for free. But it is really fragrant and useful.

There is a saying that “the end of physics research is philosophy, and the end of philosophical research is religion”, so investment is the same. I don’t know much about investment, philosophy and religion now, but I think investment should be a way of life or even a belief, and what kind of people do what kind of investment, investment is also shaping investment man himself.

1. Clarify the investment philosophy

Value investing works in China. Buffett has been emphasizing that he is betting on the fortunes of the United States. I also believe in the luck of our country. Trusting this automatically resolves a lot of distractions.

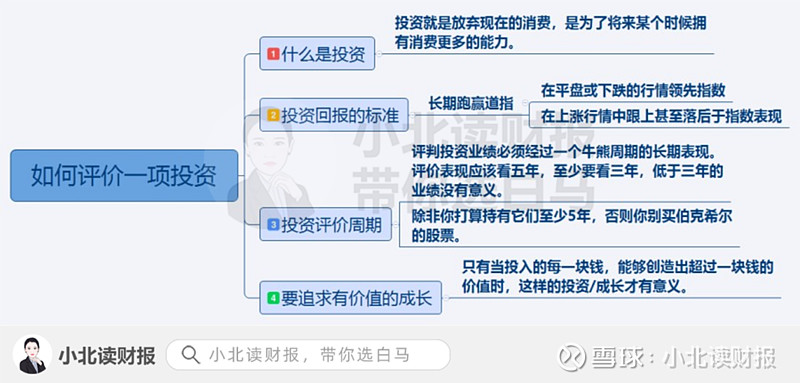

2. How to evaluate an investment?

What is an investment?

Investing is giving up consumption now in order to have the ability to consume more at some point in the future.

Therefore, not only buying stocks is an investment, but also investing in those who give up current consumption to make themselves better, such as education. A 15% yield rolls into a big number with compound interest. A little bit of progress every day, persistence brings big changes, and any small improvement, multiplied by a function of time, will make a big difference.

2. What is a reasonable return on investment?

Buffett’s goal in managing money has always been to outperform the Dow over the long term, by leading the index in flat or down moves, and keeping up or even lagging in up moves.

Many people have no idea how much the annualized rate of return is, and always feel that the higher the better. Buffett’s average annualized return is about 20%. People can’t be too greedy and too inflated.

3. Evaluation cycle

Judging investment performance must go through a long-term performance of a bull-bear cycle. The performance evaluation should look at five years, at least three years, and performance less than three years is meaningless.

When screening stocks, I tend to prefer those companies that are older and more fragrant, preferably companies with a return on equity greater than 15% after weighted deductions for 5-10 consecutive years. But doing so would exclude a lot of new stocks. Don’t know the solution to this problem.

Three, the four elements of investment

There is a lot of content in this part, and it is the very dry part of the letter.

The four elements of investing are:

① market price;

② intrinsic value;

③ Margin of safety;

④ Circle of competence.

I have learned about market price and intrinsic value, but I don’t know how to use these four elements.

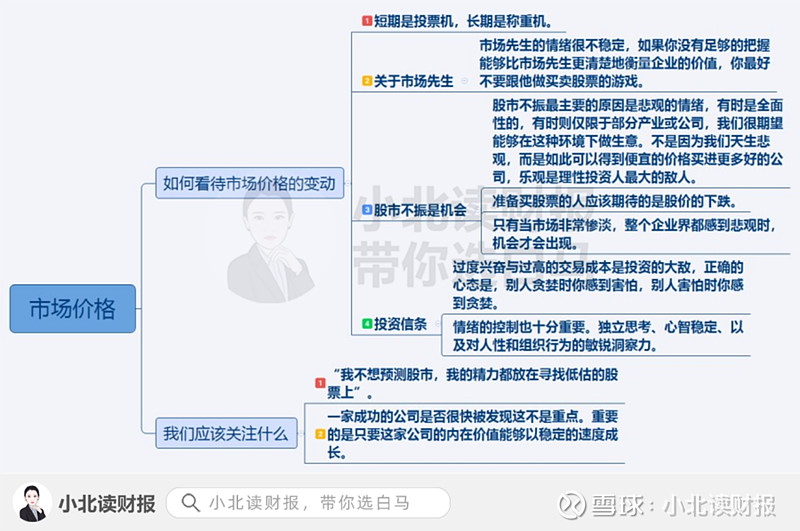

First: market price

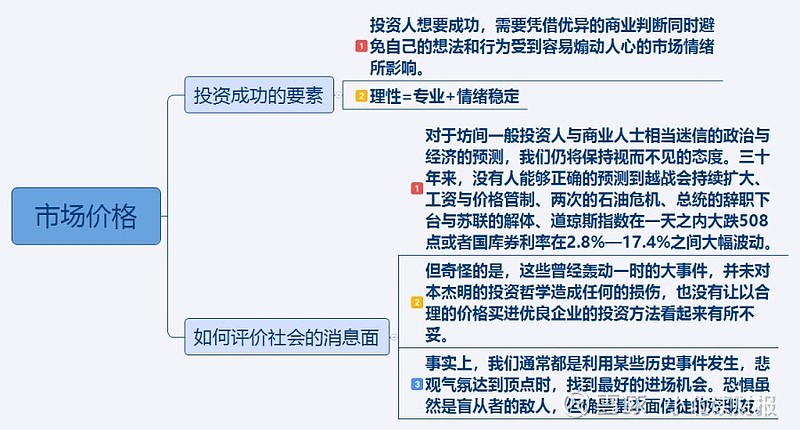

How to face the fluctuations in market prices is a problem that everyone has faced after the US stock market has been melted many times recently.

Investing is a very human thing. Everyone else is panicking. You can’t panic, buy it, and believe that you’re valuing the company correctly. It’s worth buying. too difficult.

The picture below is the description of Mr. Market in the shareholder letter. Recently, I was watching the documentary “The culprit of uncontrolled consumption”, which mentioned that the desire for survival and the “greed” and “fear” derived from survival are the most fundamental needs of human beings, and they have appeared again and again in the stock market.

Second: Intrinsic Value

How to Assess Intrinsic Value

The essence of business operation is to use cost capital to invest in production, and finally discount the generated cash flow into intrinsic value. The element that runs through it all is the flow of money/monetary funds.

The indicator of return on equity reflects the ability of the company to make money and how much return on investment it can bring to shareholders, but the analysis of this indicator only involves the balance sheet and the income statement. Wealth”, and does not take into account actual cash flow.

The DCF discounted cash flow method is to discount the cash flow that may be generated in the future years, which is a echo and supplement to the use of ROE to measure the intrinsic value.

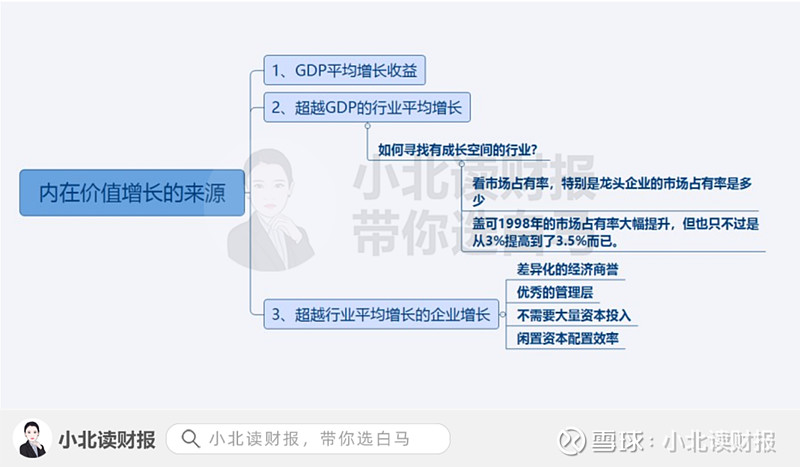

source of intrinsic value

Intrinsic value comes from three aspects:

Average GDP growth benefits; industry average growth that exceeds GDP; business growth that exceeds industry average growth.

There are three dimensions to the analysis problem, macro, meso and micro. The most mentioned in the letter is the source of growth at the micro enterprise level, mainly including: differentiated economic goodwill, excellent management, no need for large capital investment and increased idleness The efficiency of capital allocation.

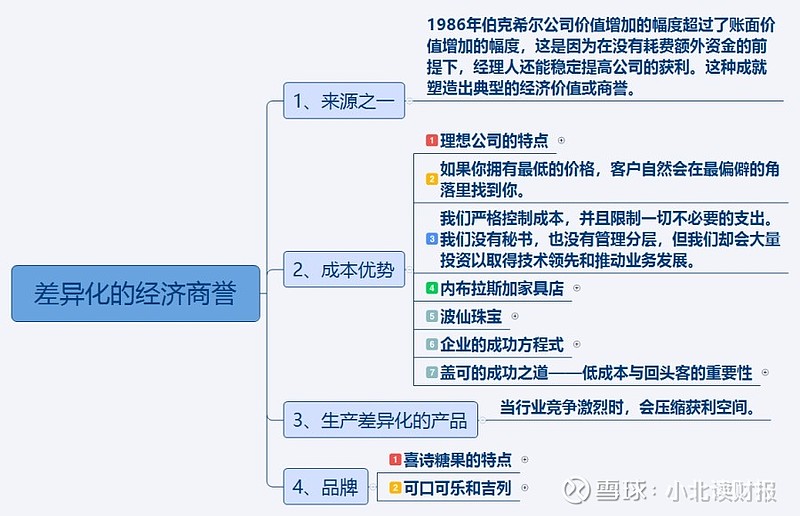

One: Differentiated economic goodwill

Differentiated economic goodwill comes from many sources, including cost advantages and branding mentioned many times in the letter.

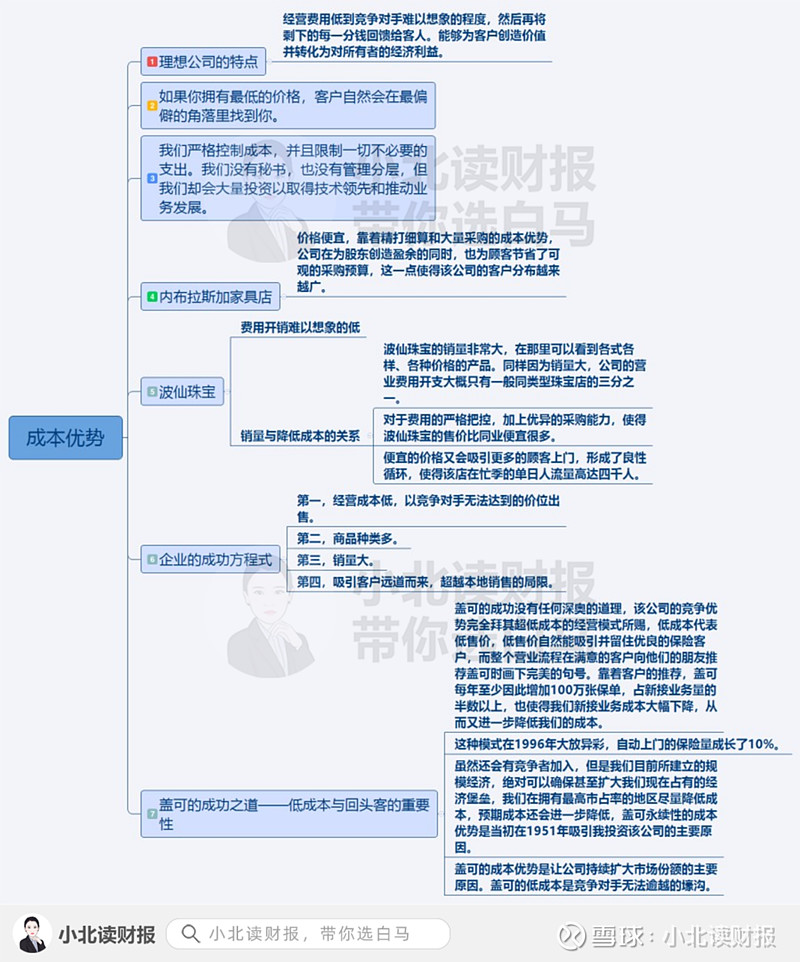

Cost advantage

Cost awareness is important.

From an investment point of view, those companies with good cost control will have better profitability and will create more value for shareholders. For Geco, low cost is the moat.

From the point of view of business operation, we should use the money on the edge of the knife and do things that are conducive to the development of the enterprise.

“We strictly control costs and limit all unnecessary spending. We have no secretaries and no management layers, but we invest heavily to gain technology leadership and drive business development.”

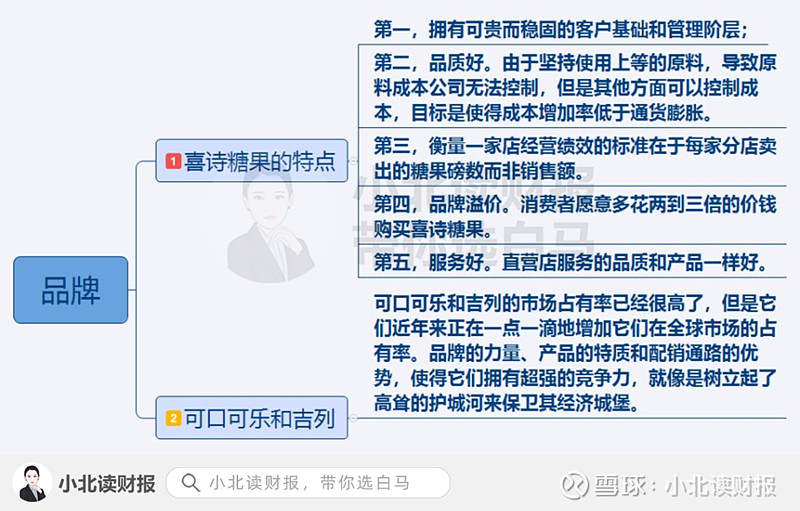

brand

The brand should be the result of the combined effect of various advantages, and finally precipitated into the brand or label that the company has left in the minds of consumers. Haitian Flavor has a large scale and has a cost advantage; at the same time, many people only recognize Haitian brand soy sauce, which is the power of the brand. Therefore, the source of moat or differentiated economic goodwill should be a structural competitive advantage. An enterprise will not have only a single moat, but some moats are the most obvious.

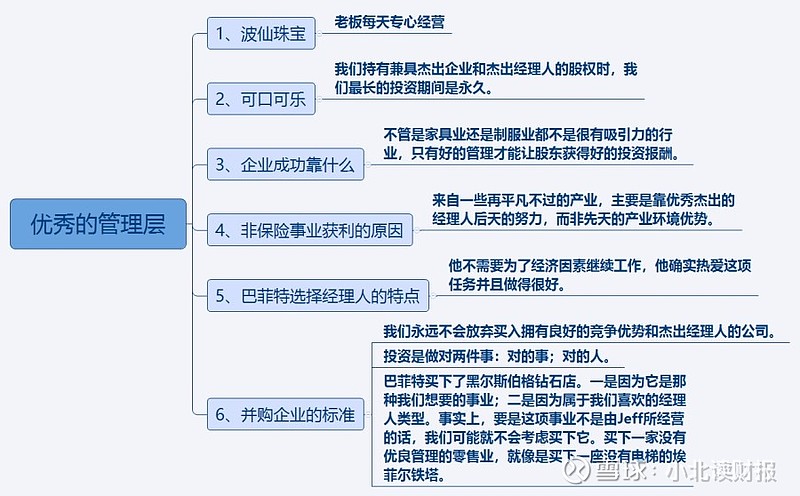

Second; excellent management

If there is a problem with the management, it will ruin a good deck, such as Shanghai Jahwa and Dong’e Ejiao.

For ordinary investors, how to judge and analyze the quality of enterprise management, whether there are quantitative indicators that can be found, and how to look if it is qualitative analysis.

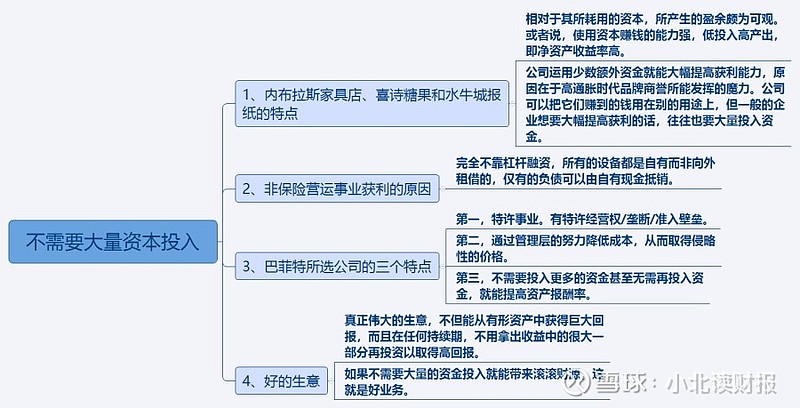

Third: No need for large capital investment

For a business, how to spend less and earn more.

According to profit = revenue – cost = unit price × sales volume – sales cost – period expense,

If you want to earn more, in addition to ① reducing unit costs through economies of scale and ② reducing period expenses through management capabilities, if you want to earn more, you must also increase unit price and sales volume. There will also be many subsections under each subheading.

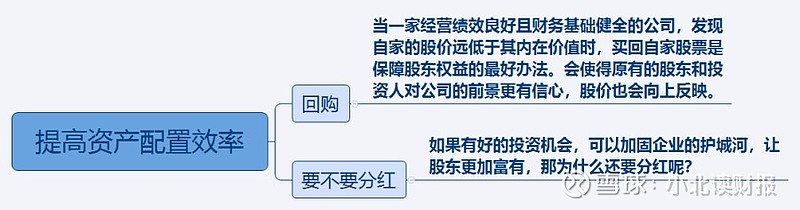

Fourth: Improve the efficiency of asset allocation

More than 50% of the assets in Moutai’s account are monetary funds, and even bank wealth management products will not be bought. Is this responsible to shareholders? In other words, Maotai has too much money and doesn’t care about making other small money.

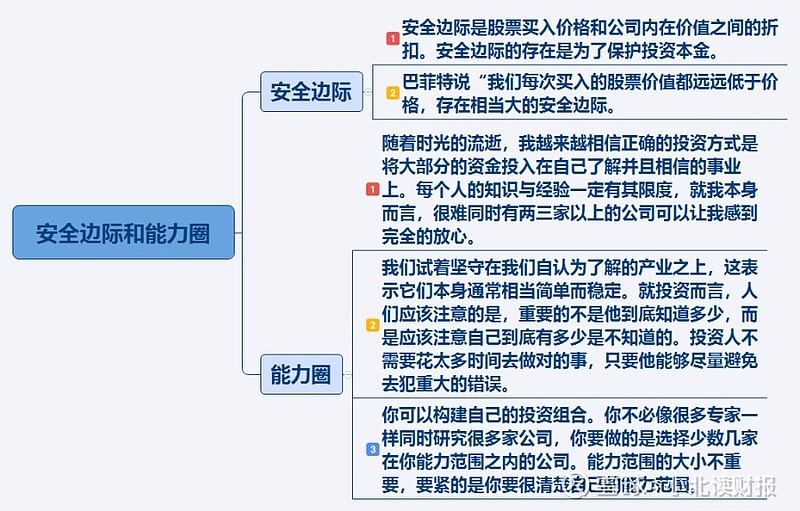

3rd + 4th: Margin of Safety and Circle of Competence

Self-awareness.

4. About investment risks

Risk comes from uncertainty. The first rule of thumb in investing is not to lose money. Either because he is too greedy, or because he does not know his own circle of ability and does not know himself, the money earned by luck will be lost by strength.

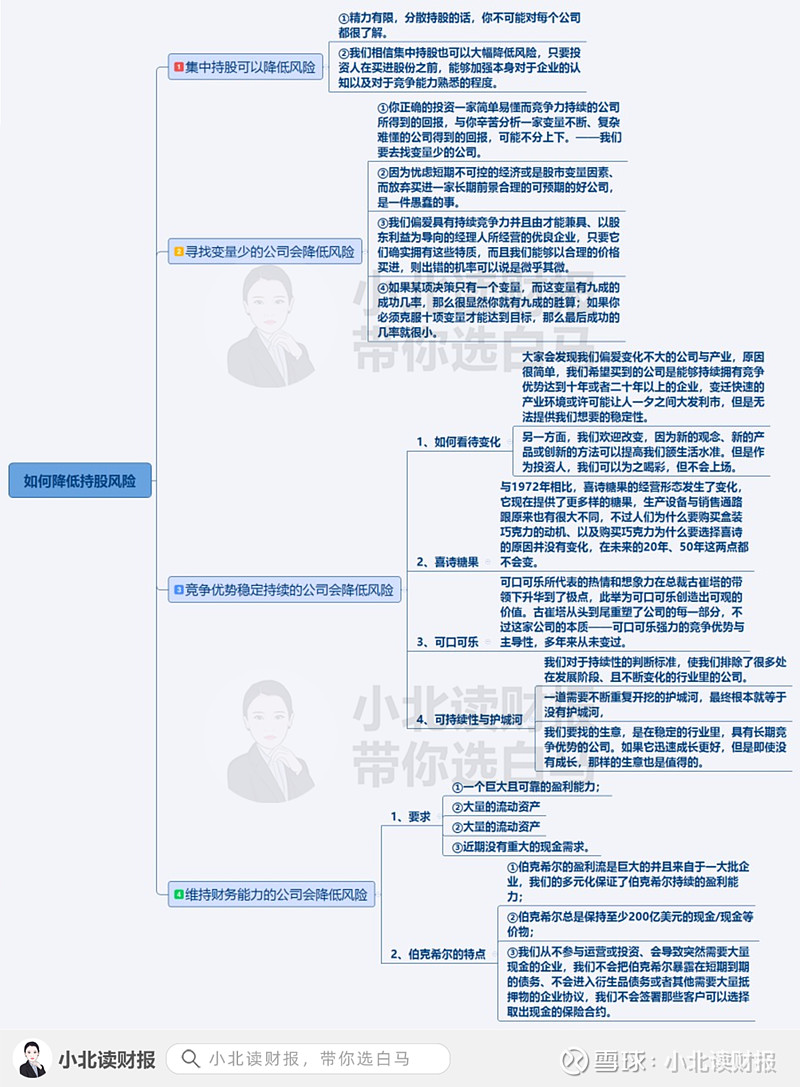

There are four ways to reduce holding risk:

concentrated shareholding;

Look for companies with few variables;

A company with a stable and sustainable competitive advantage;

Financially strong company.

Having money itself is competitiveness, and it can resist risks, especially in the early stage of burning money when the industry concentration is not high, just like Meituan and Didi have burned other companies to death in the end, and the market is theirs .

5. Reflection on reading the letter

There is a lack of understanding of many of the contents of the letter, and the consequences of eating what others have chewed are obvious. Therefore, if you read English and translate it yourself, the effect will be better. In addition, much of the knowledge in these letters still appears to be beneficial.

For example, the following is mentioned in the 1993 letter, which is not much better than the content of many best-selling books.

⒈ Criteria for judging enterprise value

What really matters is real value per share, not book value. Book value is an accounting term used to measure the capital invested in a company, including large undistributed profits. Real value is the estimated discounted value of the cash flows that a business can generate over its lifetime.

Over the long term, Berkshire’s market value and real value will be at the same level.

⒉ Which industry do you invest in?

We never imagined we would enter the footwear business five years ago.

We don’t have a specific opinion on which industry we will enter in the future. For a large corporate shareholder, pursuing promising new ventures can sometimes be harmful, so we prefer to focus on those economic forms that we want to have, but also We love the company of managers we work with.

⒊Why do you need to concentrate shares?

With limited energy and diversified holdings, you can’t know every company well.

We believe that concentrated shareholding can also greatly reduce risks, as long as investors can strengthen their knowledge of the company and familiarity with the competitiveness before buying shares.

⒋About risks

Risk refers to the possibility of loss or injury.

Risk is not the relative volatility of the stock price, not the beta value,

Real investors like volatility, and as long as the market fluctuates more, some ultra-low prices have a better chance of appearing in some good companies. It is better to be vaguely right than precisely wrong.

(1) How to assess risk?

Whether the aggregate of the after-tax income (including the sale of shares) received by an investment during the period it is expected to hold will allow him to maintain the purchasing power he had at the time of the original investment, plus a reasonable interest rate.

Factors evaluated:

First, the extent to which the company’s long-term competitiveness can be measured;

Second, the measurable extent to which the company’s management has used the company’s potential and used capital effectively;

Third, the company management does return the benefits obtained by the company to shareholders, not to a measurable degree of enrichment;

Fourth, the price at which the enterprise was purchased;

Fifth, the net purchasing power income of investors must be deducted from taxes and inflation.

Investors don’t need to rely on precise formulas or stock price history, but use less precise but useful methods to see the risks lurking in certain investments.

This topic has 14 discussions in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/1830902728/230241156

This site is for inclusion only, and the copyright belongs to the original author.