This week, the stock prices of container shipping companies plummeted collectively. We also reduced our positions for the first time in six months since the opening of the market yesterday and believed that this action should be done under the situation of uncertainty. From Wednesday to Friday, the stock prices of various shipping companies were in a cliff-like slump. We still need to clarify what happened here. This round of slump originated in the United States, and we are relatively clear about the situation in the United States. Today, let’s sort out what we have learned before the US stock market closes today:

one. As of today, the stock prices of the world’s major container shipping companies are all below the half-year line, except for COSCO SHIPPING Holdings, which are basically at the lower edge of the rising channel. If it continues to go down, the whole situation will reverse. In fact, the stock price also follows the perception. Therefore, it is more important to judge the general understanding of the market. This week’s situation stems from JPMorgan’s warning, but the actual situation may need further identification.

two. High inflation in the United States is certain, and the U.S. government is struggling to find ways to reduce inflation from various aspects. One is the possibility of tariff cancellation, and the other is the possibility of government intervention in freight rates (see Presidential Address in February). The two have positive and negative effects on freight volume and freight rates.

three. In fact, several major container companies have fallen below the half-year line in March and April, but at that time, considering the issue of China’s epidemic and inflation, they were looking forward to a rebound. The rebound also came as scheduled, and the situation this week was different from the previous round. The situation in March and April was a supply-side issue, and this round is a demand-side issue.

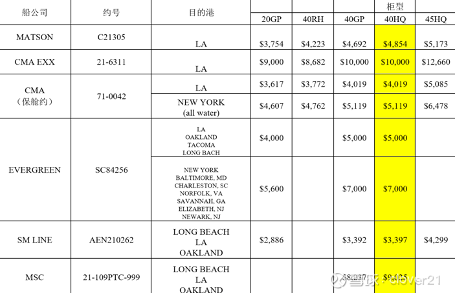

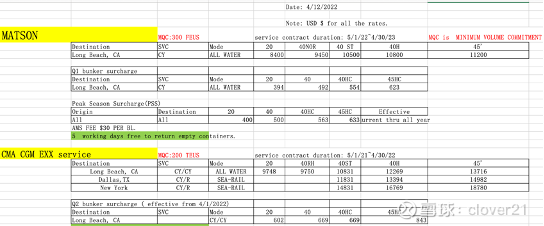

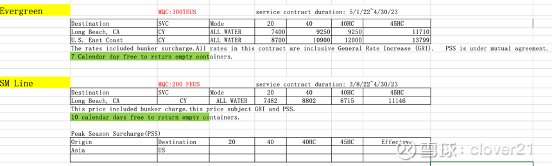

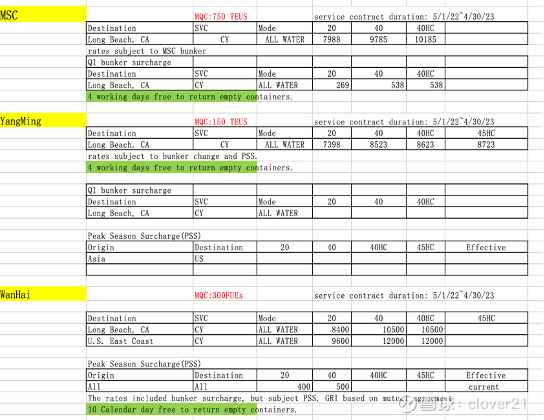

Four. We are more familiar with the US line, and the price of the long-term association has indeed doubled compared to last year. The market price follows the market demand. At the same time, we believe that after several years of capacity reduction and integration, several major alliances already have a fairly high market share, and joint market making is an objective reality. Therefore, the long-term association price is a base price. On the other hand, because of the high freight rate in the past two years, the high freight rate has driven out low value-added products when the market is relatively full. Therefore, in the case of falling freight rates, the return of low value-added products is also an important underpinning force. The conclusion here is that we believe that the freight rate is underpinned, and the market price is unlikely to be lower than the long-term contract price. Below is a comparison of our long-term contract prices last year and this year:

This is the 21-year long-term agreement price

These are the 22-year long-term association prices, and there is no doubt that the long-term association price has doubled.

five. The shipment of our orders exported to the United States in the third quarter did drop by 50% compared with the same period last year. One of the reasons we see is that the inventory of American retailers is relatively high (but agree with Han Jun’s analysis that the inventory-to-sales ratio is actually one month), and the other reason is that Retailers based on the former reason are also waiting for the removal of tariffs to place orders. We haven’t seen cases where retailers cancel orders on hand because of inventory. For US retail demand, the structure of imported products can also change. We believe that China’s total import and export volume and the US import container data will not go down, and it is indeed difficult to say that US demand will shrink significantly. In this case, we will continue to pay attention to the changes in this data, because some signals appear.

six. Last week there was a signal that one of our shipowners, MSC, took the initiative to come to the door to reduce the price of the 40HC long-term contract from 10185 to 8485. This proportion is not small, but it should be said that they have reduced the price to a reasonable level compared with other shipowners. We are contacting other shipowners to see their trends. If companies cut prices collectively, then this is a trend. Shrinking demand will become a consensus, and the relevant logic will also change.

To sum up, for COSCO SHIPPING Holdings, we still believe that the logic has not changed but the situation is in the process of evolution. The reflected signal needs to be confirmed and falsified. In the case of a large gap and low opening for two consecutive days, the position is first reduced to take a risk-averse action and the subsequent development of the situation. On the other hand, it is even more impossible to expect Haikong to rise sharply for the time being.

$COSCO SHIPPING Holdings(SH601919)$ $COSCO SHIPPING Holdings(01919)$

This topic has 82 discussions in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/9400537476/222337841

This site is for inclusion only, and the copyright belongs to the original author.