(After buying Coca-Cola at 0.4PR, “buy $1 for 40 cents” became Buffett’s mantra)

Foreword: I recently watched the TV series “Basic Law of Genius” and found that it is not difficult to invent a valuation formula in the investment field. What is difficult is to prove its universal correctness. As the inventor of the P/E ratio, I have recently written three articles on which the P/E formula is difficult to falsify. It can be basically determined that the price-earnings ratio formula is Buffett’s investment secret, and I implore Snowball V to help forward it.

In order to learn from Buffett, the author imitated PEG and invented a valuation parameter called “price-earnings ratio”. The formula is: price-earnings ratio = price-earnings ratio/return on equity (PR=PE/ROE). When the price-earnings ratio is equal to 1PR, it is a reasonable valuation, and if it is greater than 1PR and less than 1PR, it is overvalued and undervalued. Buffett’s classic investment: See’s Candy. The market-to-earnings ratio = 12.5/25 = 0.5PR, which is equivalent to buying at half price. Buffett claims to have changed from “ape” to “human”!

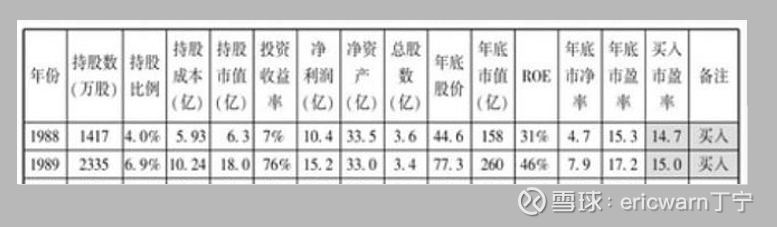

After buying See’s Candy, Buffett, who tasted the sweetness of high ROE consumer stocks, turned his attention to Coca-Cola. And in the two years after the stock market crash in 1987, Coca-Cola was successively bought. According to online data, Buffett’s buying price in 1988 was 14.7PE, the ROE was 31% that year, and the price-earnings ratio = 14.7/31 = 0.474PR. In 1989, Buffett’s purchase price was 15PE, the ROE was 46% that year, and the price-earnings ratio was 15/46=0.326PR. The average valuation of the price-earnings ratio purchased in two years is exactly 0.4PR, which is equivalent to buying Coca-Cola at a discount of 40%. (A weighted algorithm can also be used, and the calculation results are approximate)

It’s worth noting that Buffett often claimed to have gone from ape to man after buying See’s Candy. But after buying Coca-Cola, “buy a dollar for 40 cents” became Buffett’s mantra.

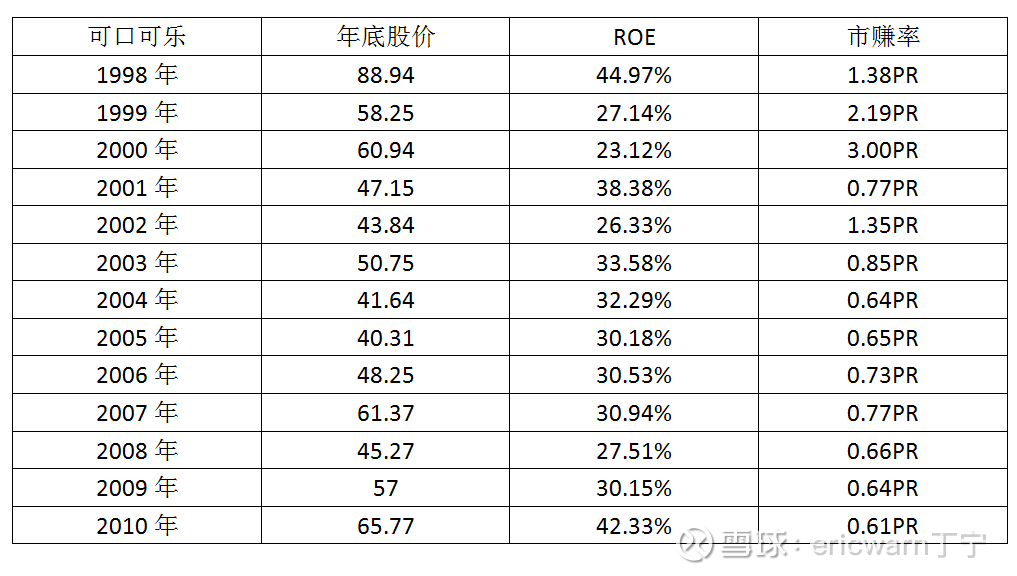

In 1998, Coca-Cola hit an all-time high of $88.94, and Buffett’s investment performance was exactly ten times that of a decade. The ROE that year was as high as 44.97%, the price-earnings ratio also soared to 62.2PE, and the price-earnings ratio valuation was 1.38PR. It’s a pity that Buffett didn’t overestimate selling. Over the next decade or so, Coca-Cola’s stock price never hit a new all-time high, and it wasn’t even a breakthrough until 2011. For more than a decade, Buffett could only rely on Coca-Cola’s dividends and buybacks to make up for his gains. Although it is also very rich, but my heart is very unhappy. Not only did he blame himself for selling at a high 50PE in the shareholder letter, but he no longer mentioned the concept of “permanent shareholding”.

From 1998 to the present, Coca-Cola has occasionally had abnormal years with ROE falling below 30%. However, in normal years when ROE is greater than 30%, Mr. Market has never given a price-to-earnings ratio valuation of more than 1PR. Similarly, in normal years when ROE is greater than 30%, the current price of Kweichow Moutai has also exceeded the 1PR valuation, so caution is needed.

Last but not least, a closer look at the P/E formula reveals a problem. That is under the premise of constant ROE and 100% retained earnings. Buying and selling companies with different ROEs at 1PR valuation, the higher the ROE, the higher the investment compound interest will be. For a company with an ROE of 30%, the theoretical investment compound interest of the market-to-earning ratio is as high as 30%. For a company with an ROE of 20%, the theoretical investment compound interest of the market-to-earning ratio is only 20%. In this case, why doesn’t Buffett blindly pursue high ROE companies? In fact, in the real world, high ROE companies are prone to decline in performance and encounter Davis double kills. Therefore, the market-to-earning ratio gives high ROE companies a higher theoretical investment compound interest, which is actually a kind of risk compensation. It is precisely because companies with high ROE are difficult to maintain for a long time, so Buffett lowered the minimum threshold of ROE to 15%.

Last but not least, the P/E formula is by no means a panacea. But it can go beyond the price-earnings ratio and price-to-book ratio, providing a clearer margin of safety when investing. As for whether the investment can be successful, it depends on the investor’s personal competence circle (selecting outstanding companies), the company’s moat (long-term stable ROE), and even a little luck (Mr. Market completes the valuation repair faster) .

Related Links: “Price-to-Earning Ratio Formula Difficult to Falsify First Case: PetroChina Leaked Buffett’s Investment Secrets”: web link “In the face of state-owned and central enterprises that cannot be acquired, it is more suitable to revise the market-to-earnings ratio”: web link

@Today’s topic @雪ball creator center @snowball talent show @forcode @micro evolution @HIS1963 @天地夏影@流水白菜@牛春宝@Luoyang small retail investor @ Fuguo Zhou Jun @ Refuge Woodland @ Phoenix Investment Villa @ Yaya Hong Kong stock circle @houeninvestzhangyankun @lifetime focus on growth stocks @faith in value @happy stocksea @snow tears shadow @mysterious Amazon

$Kweichow Moutai(SH600519)$ $Tencent Holdings(00700)$ $CNOOC(00883)$

There are 98 discussions on this topic in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/9363345092/228631862

This site is for inclusion only, and the copyright belongs to the original author.