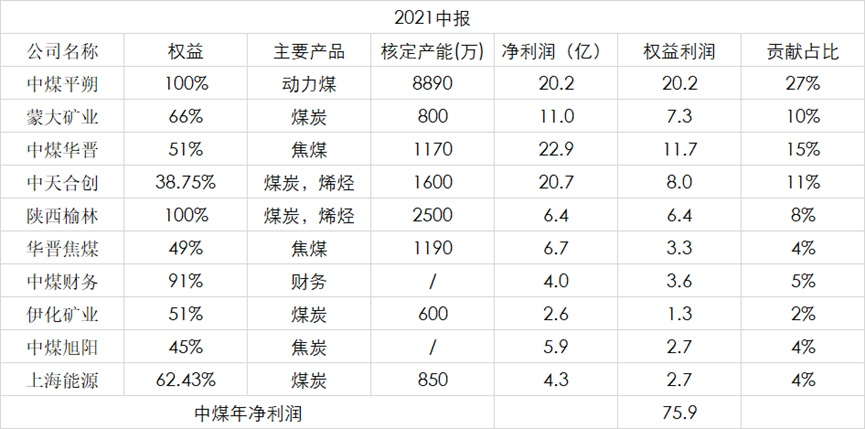

Coal investors like to count mines. Amao @Amao Investment leads the trend. The profit contribution of China Coal Energy mainly comes from the following subsidiaries. Compared with last year, the profitability in 2022 will be greatly improved. One of the profit ceilings of the coking coal industry The net profit margin of Coal Huajin is 54+%, the small and beautiful Hecaogou is 53%, the always excellent Mengda is 45.9%, and Yihua, which has returned to normal, is 40%. The profitability of these mines can be taken out to PK the best peers in the industry without falling behind.

The future potential of China Coal Energy has yet to be released. The infinitely possible sea will contribute an annual net profit of about 5 billion, the gradually decreasing 4.5 billion + debt interest, and the anthracite coal with a net profit of 1 billion.

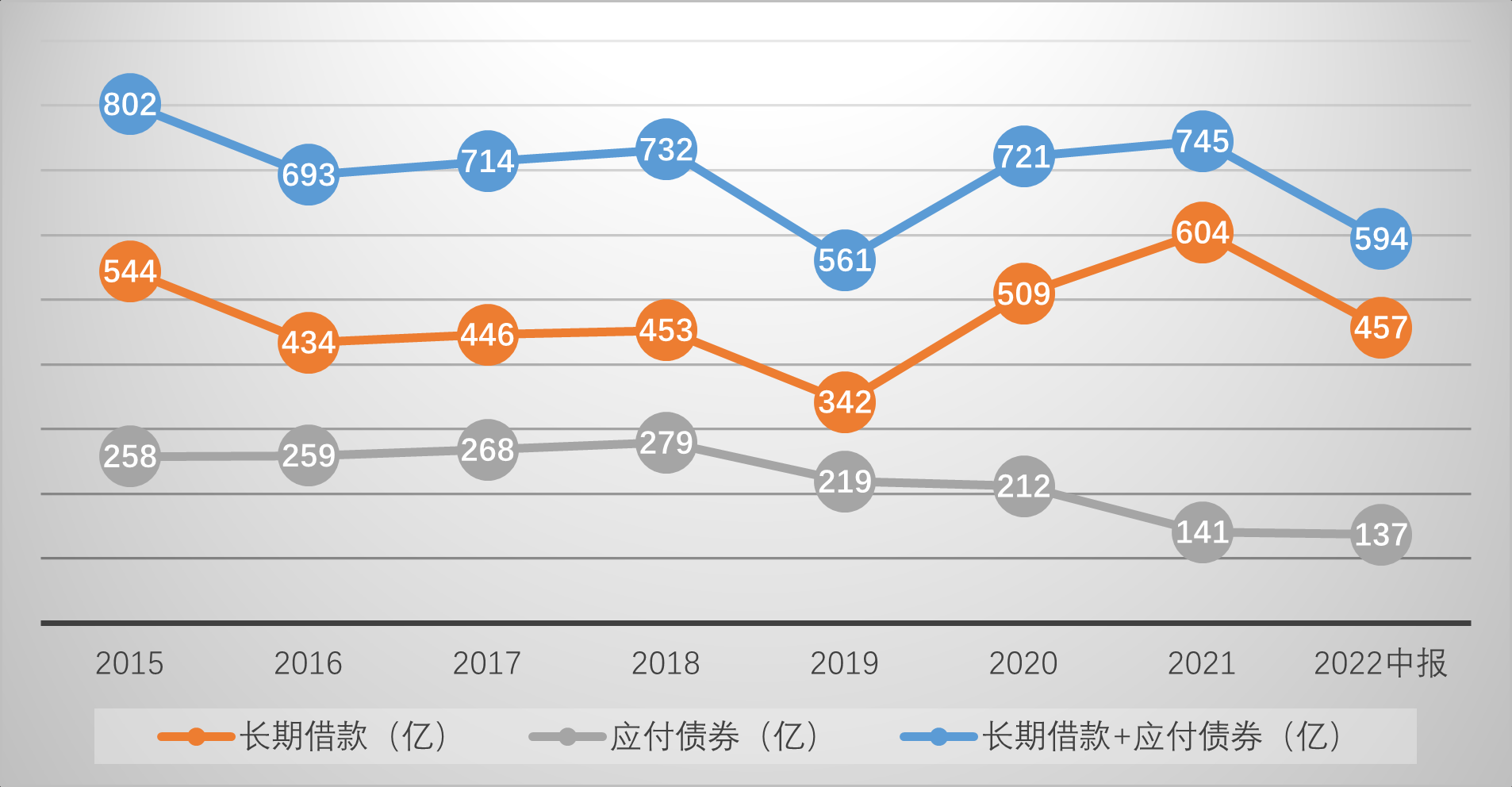

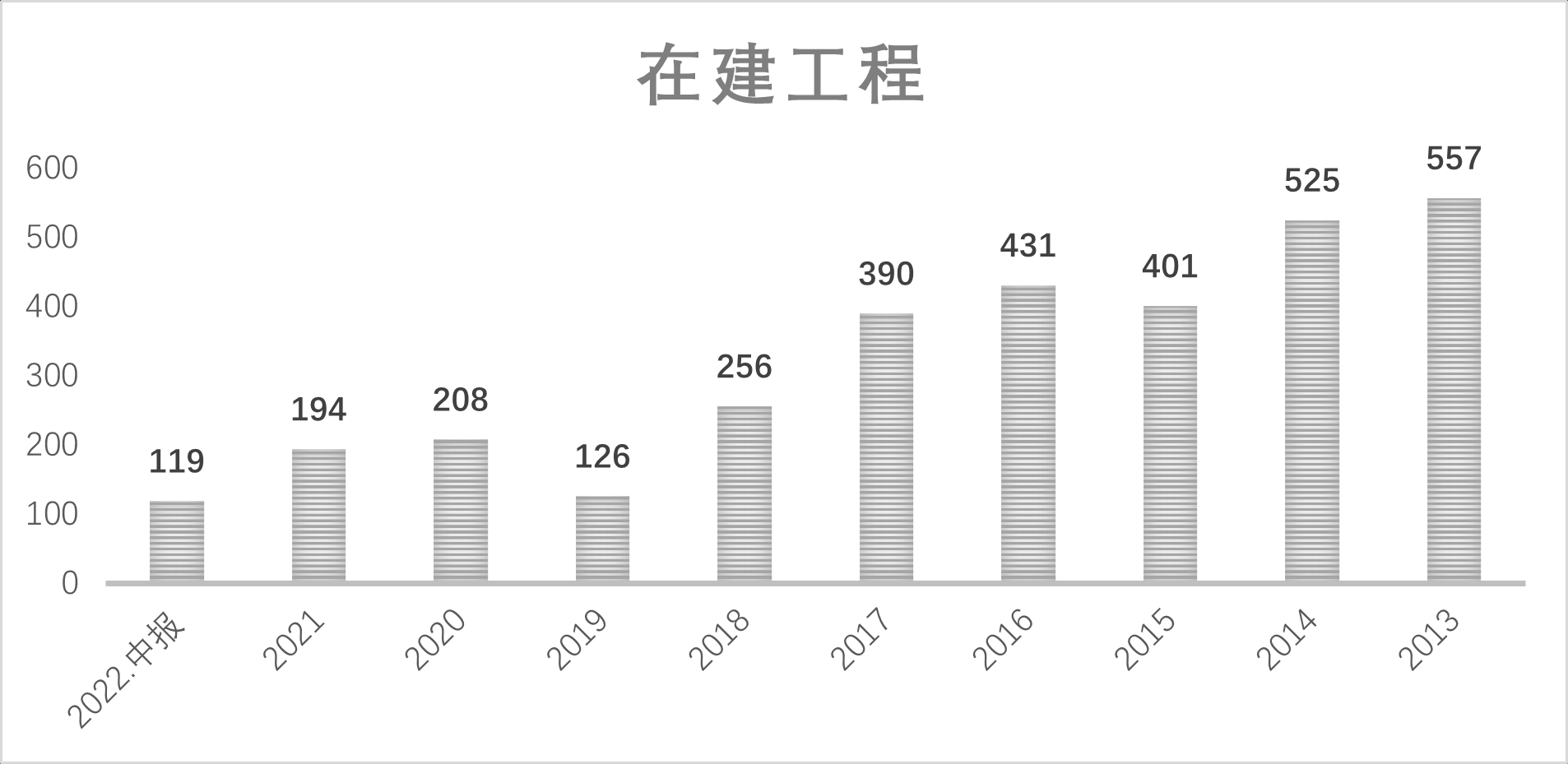

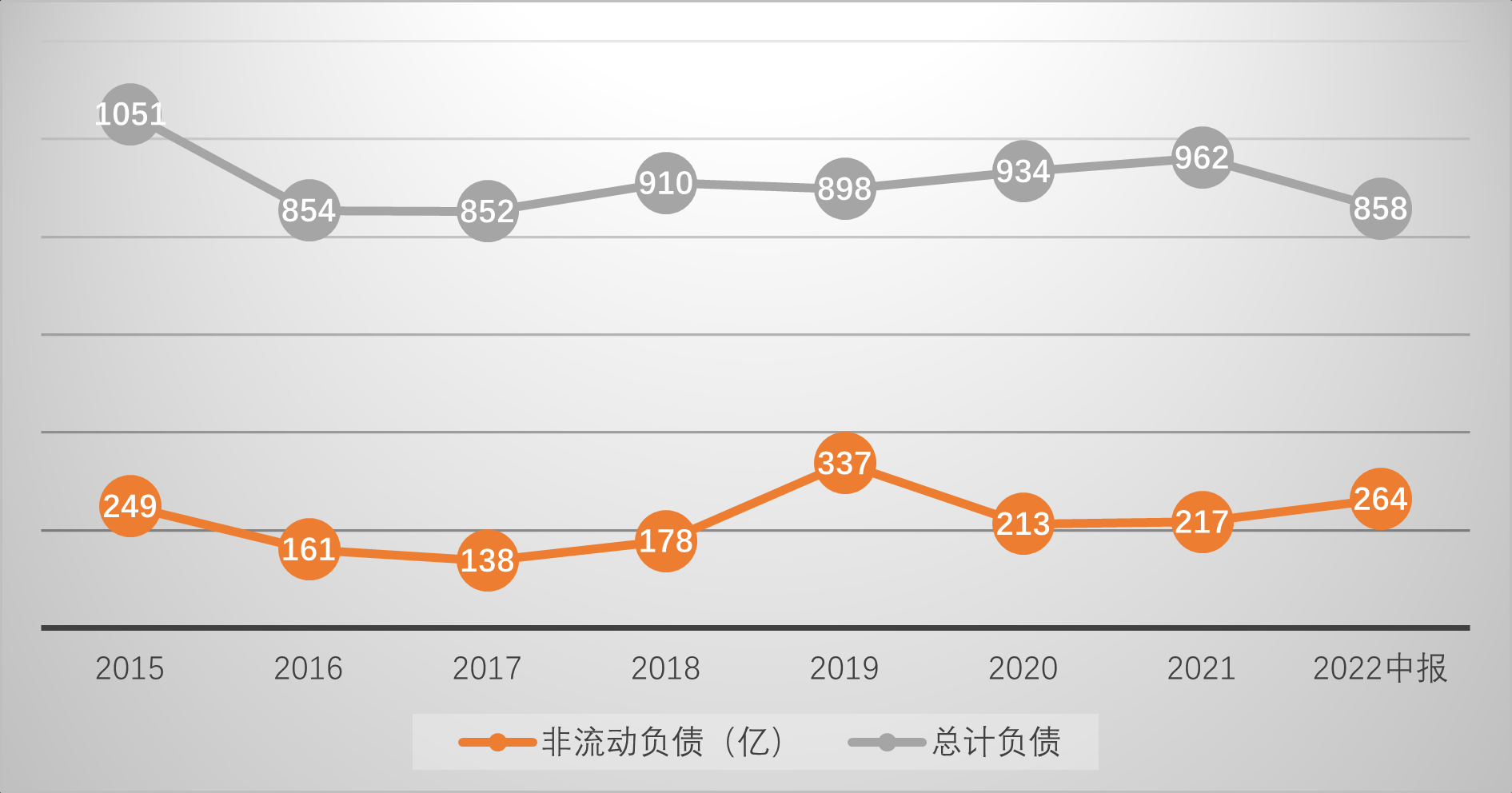

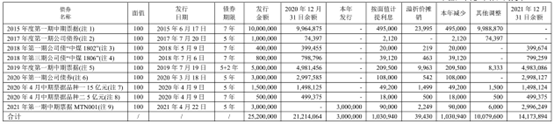

China Coal Energy has been criticized by conservative investors for its high debt. Based on the debt ratio, one of the important assessment indicators of the central enterprises themselves, the management of China Coal Energy of course attaches great importance to it and has been working hard: using the support of the financial company and the group to adjust the debt structure. Unfortunately, in the past few years, the construction projects have been bleeding, the profit of the coal mine is not enough to support the large-scale expansion of China Coal, the debt basically expands in tandem with the balance sheet, and the absolute debt scale has been at a high level.

If, coupled with non-current liabilities due in one year, the absolute size continues to soar!

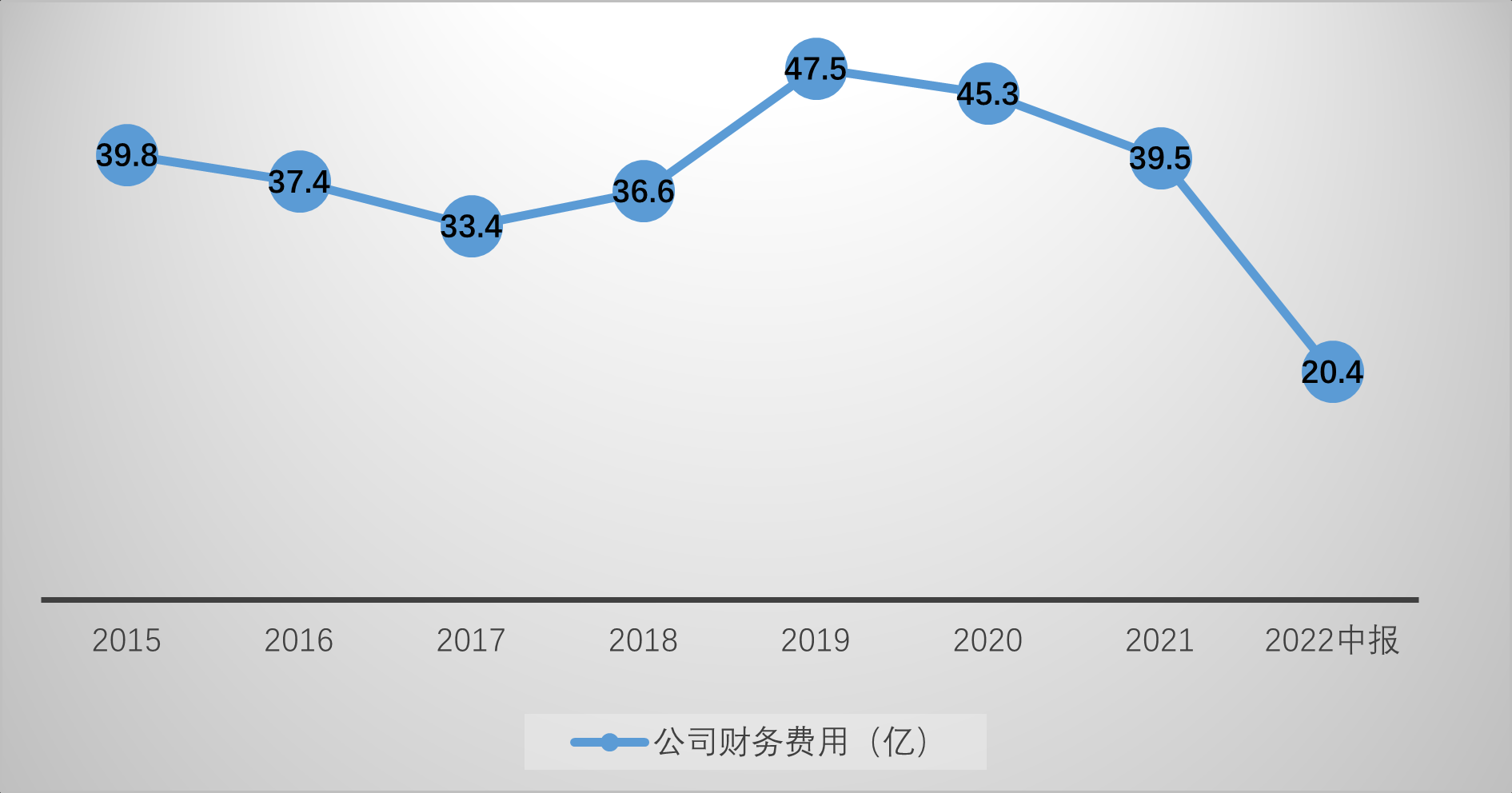

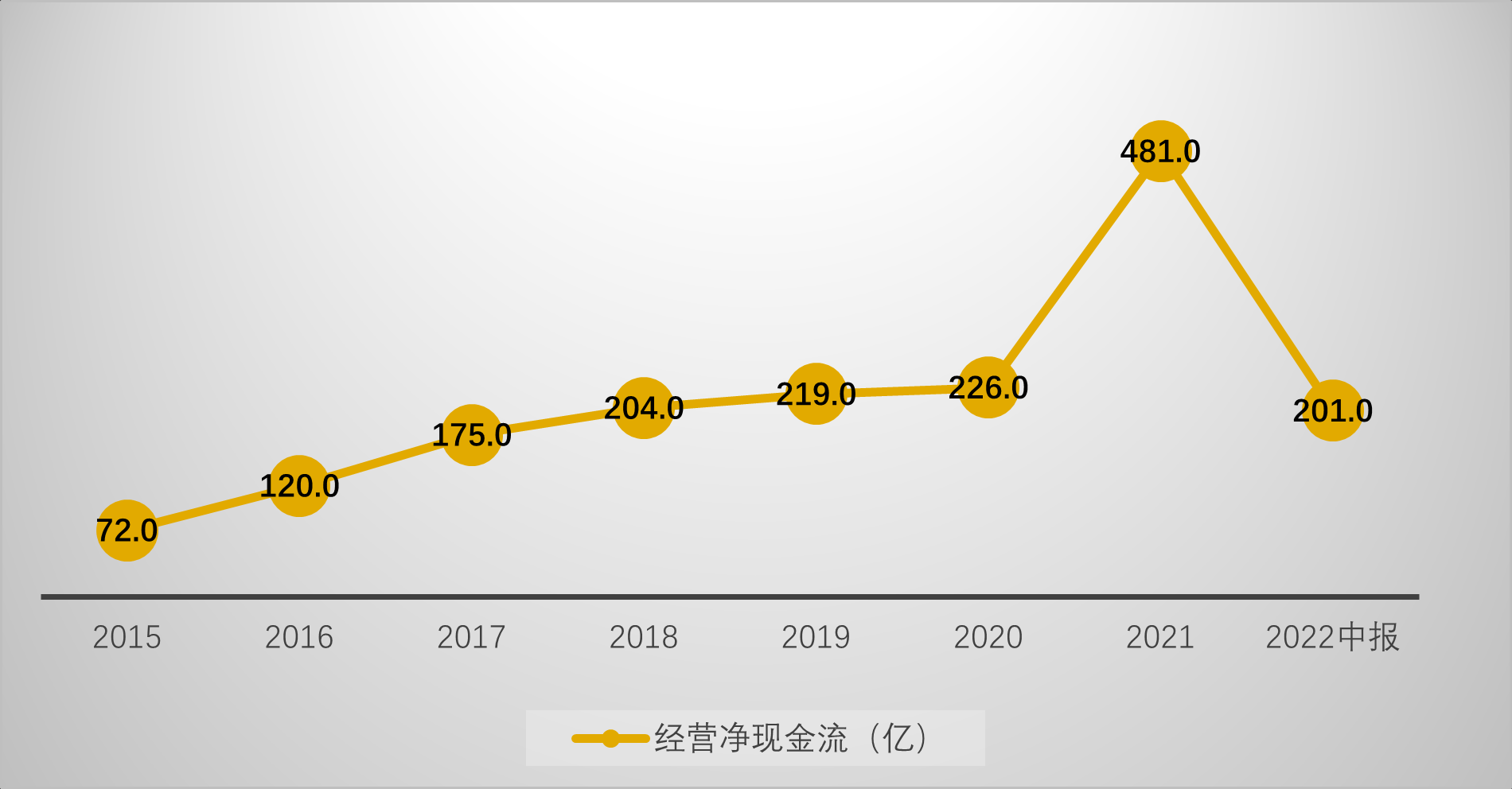

However, the inflection point is coming! , China Coal has maintained non-current liabilities of 20 billion for a long time, and under the support of strong cash flow, there is a high probability that it will not renew the loan. Interest-bearing liabilities decreased by nearly $12 billion in the second quarter of 2022. As of 2021, although the financial expenses are decreasing year by year, the main contribution is the increase in interest income due to the increase in the funds on the account, and the changes on the liability side are not obvious enough. In the first half of this year, due to the impact of the consolidation of Dahai, although the liabilities were reduced, the financial expenses were basically the same. China Coal’s cash has skyrocketed in the past two years. At present, the company has not seen aggressive debt reduction, and it is estimated that it will take time to ferment.

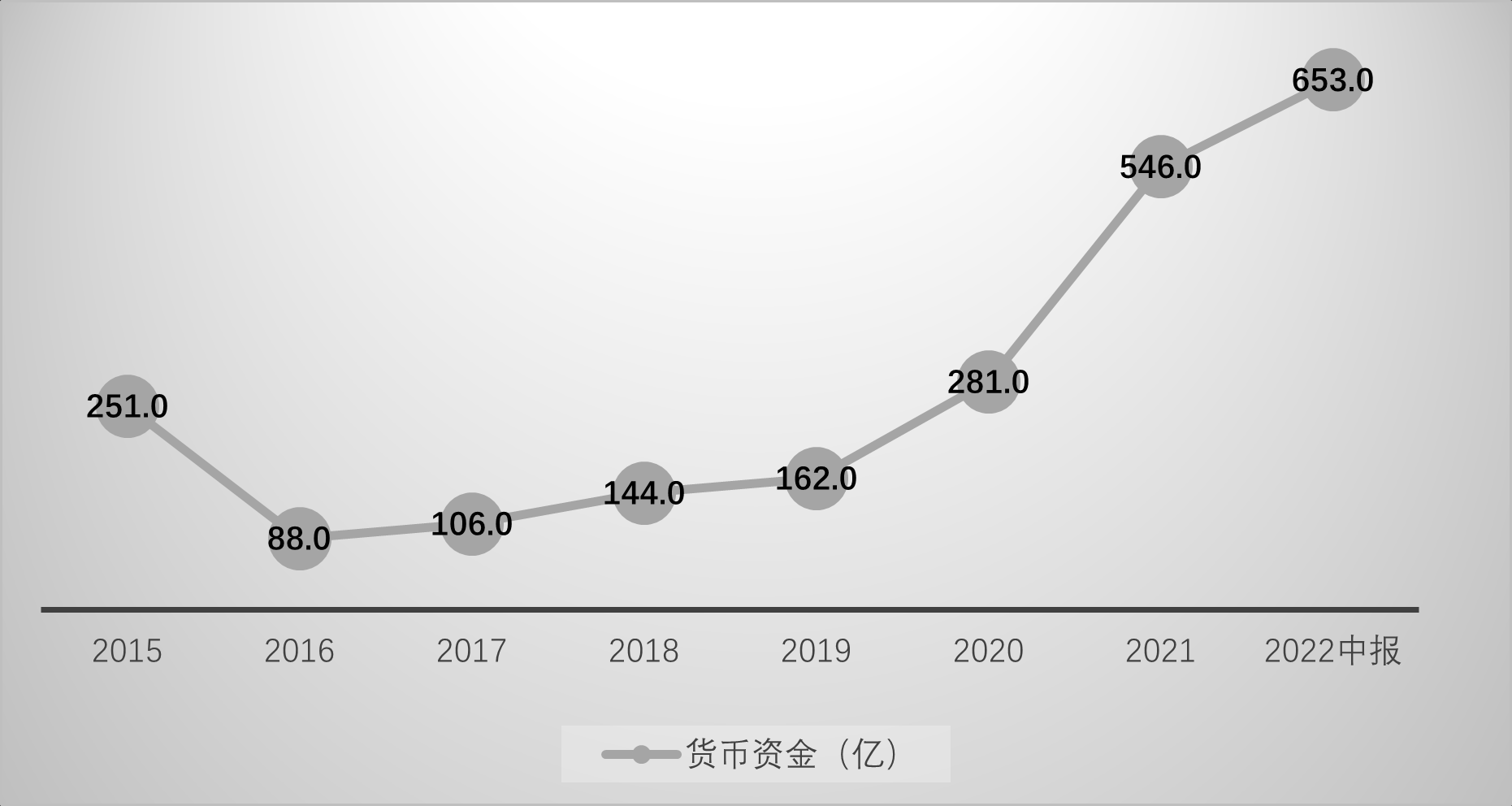

For a long time in the past, monetary funds have not been enough to meet the non-current liabilities due within one year, which means that the company’s funds have been very tight. Starting from 2021, the company’s monetary funds have rapidly accumulated to deal with huge maturing debts. Getting more and more comfortable. Monetary funds mainly come from the company’s operating income, and there is no problem with future sustainability.

China Coal Energy actively adjusts its debt structure, high-cost bills and bonds are gradually maturing, and the interest rate and scale of debt will gradually decline in the future.

It is expected that within 2-3 years, the balance sheet of China Coal Energy will reach the first-class level in the industry.

@アコInvestment @cultivation dezhen @中新disk @16 fortune rape king

There are 27 discussions on this topic in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/3203323063/229151783

This site is for inclusion only, and the copyright belongs to the original author.