The Hang Seng China Enterprises Index (HKHSCEI) has performed bleak after 2018, giving the impression that Hong Kong stocks are forever in a bear market. Many people say: The low valuation investment strategy has failed, and the Hong Kong stock market is a value trap. Is it really? Recently, I read “Twenty Years of Hang Seng Index, The Controversy Between Emperors, Nobles and Beggar Gang” written by Erlang Fund, and I deeply felt that “the devil is in the details”.

Let’s first look at the composition adjustment of the Hang Seng China Enterprises Index after 2018. In 2019, the Hang Seng State-owned Enterprises Index included Sunac China, Country Garden and other Chinese real estate stocks, and in 2020, it included Alibaba-W, Xiaomi Group-W, Meituan-W and other Chinese concept stocks. On the other hand, the weight of state-owned enterprises in traditional industries continues to decline. From the end of 2018 to mid-2022, the proportion of H-share ETF holdings in China Mobile dropped from 7.72% to 3.80%, and the proportion of CNOOC dropped from 3.61% to 2.34%. Bank of China The proportion dropped from 6.25% to 3.14%.

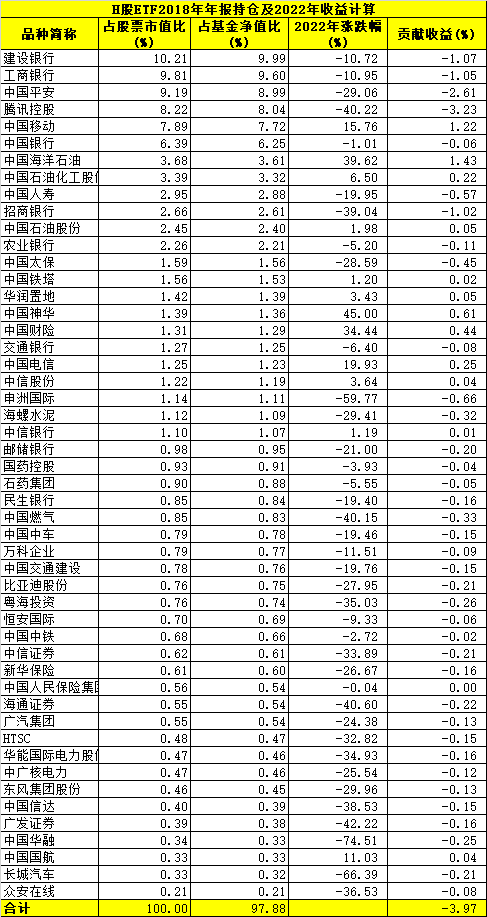

What if the constituents do not adjust? I use the approximate calculation of the holdings of the $H-share ETF (SH510900)$ . If the Hang Seng China Enterprises Index keeps the weight of the constituents at the end of 2018 unchanged, the increase this year will be -3.97%; if the weight at the end of 2019 is maintained, the increase this year will be – 6.96%; considering that the Hong Kong dollar has appreciated by 10.96% against the RMB this year, holding H-share ETFs should be profitable in 2022 !

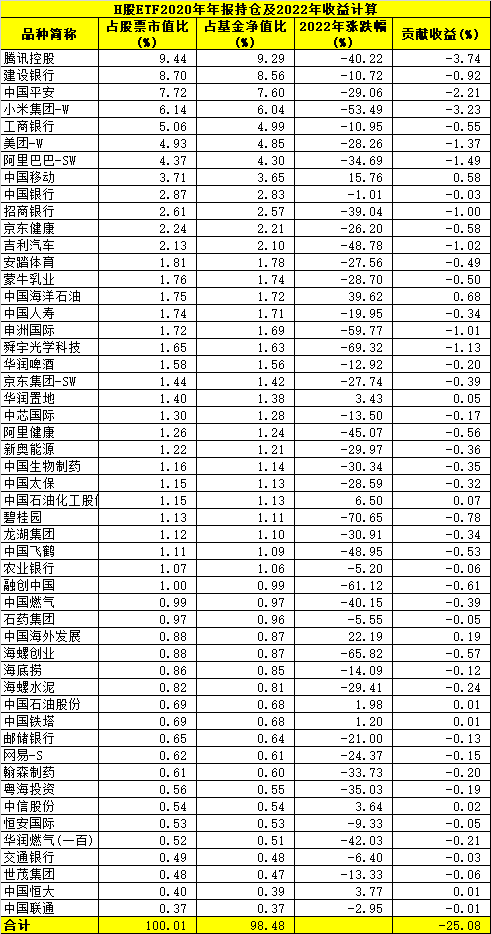

After being included in the returning Chinese concept stocks in 2020, the constituent stocks have completely changed their faces, and the “state-owned enterprise index” is no longer worthy of its name-if the weight of the constituent stocks at the end of 2020 remains unchanged, the increase this year is -25.08%, and the actual increase this year is -28.89% .

The conclusion is obvious, it is not the low valuation investment strategy that has failed. The problem is that after 2019, Hong Kong stocks used index funds to become overvalued Chinese real estate stocks and Chinese concept stocks. The dismal performance in the past two years is precisely the result of abandoning low-valued investments.

The enemy is at Honnoji Temple!

@A Tu Ge a @Chen Shaoxia

This topic has 20 discussions in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/5231009643/232092240

This site is for inclusion only, and the copyright belongs to the original author.