“In what form do bank provisions exist? Where is it? (1) Starting from the provision of Shuanghui Development”

I. Introduction

In the previous article, we analyzed the financial data of Shuanghui Development, and finally came to the conclusion that the provision of Shuanghui Development is the result of the accumulation of asset impairment losses (operating expenses) over the years from the perspective of the profit and loss statement (income statement). A bookkeeping technique that is a virtual concept.

From the perspective of the balance sheet, the provision exists in the form of assets, and the main source of asset impairment is the loss of inventory depreciation. Obviously, this part of assets refers not to currency cash, but to inventory, so the provision of Shuanghui corresponds to The asset is the inventory, and the real body of the inventory may be the ham sausage or cold fresh meat on the shelf, or the pig in the cold storage. Only when these assets that are expected to expire and cannot be sold are “accidentally” sold and turned into cash, the provision can be turned into a cash-covering profit. If they are eventually expired and destroyed, the provision will be written off (another way of accounting).

So, what are the similarities and differences between banks’ provisions and non-financial companies such as Shuanghui? This article will come to a detailed analysis of the bank’s provisions.

Second, the bank’s income statement (profit and loss statement)

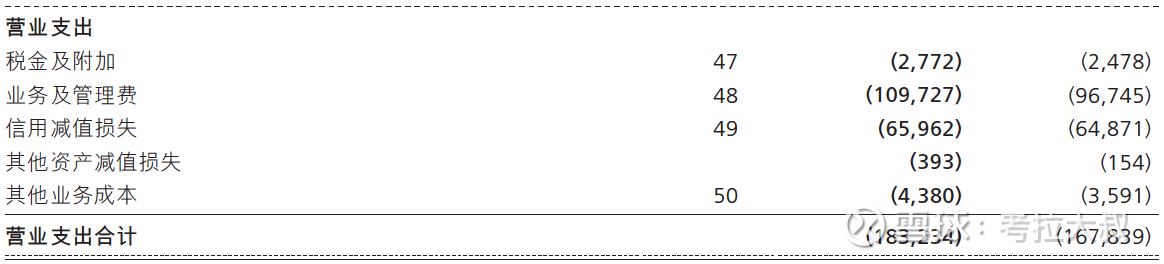

Figure 1 – China Merchants Bank’s 2021 Annual Report Consolidated Income Statement

As shown in Figure 1, the credit impairment loss is a very important item in the operating expenses of China Merchants Bank, accounting for almost one-third of the total cost. The “credit impairment loss” here is what we commonly call provision, and the part of the impairment accumulated year by year that has not been written off is called “impairment provision and loss provision”, which is what we commonly call provision.

Similar to Shuanghui Development, the credit impairment loss here is also realized through bookkeeping, so we can’t see what form the provision is in (for example, banknote cash, deposits, loans, bonds, etc.) .

3. Credit impairment losses of banks

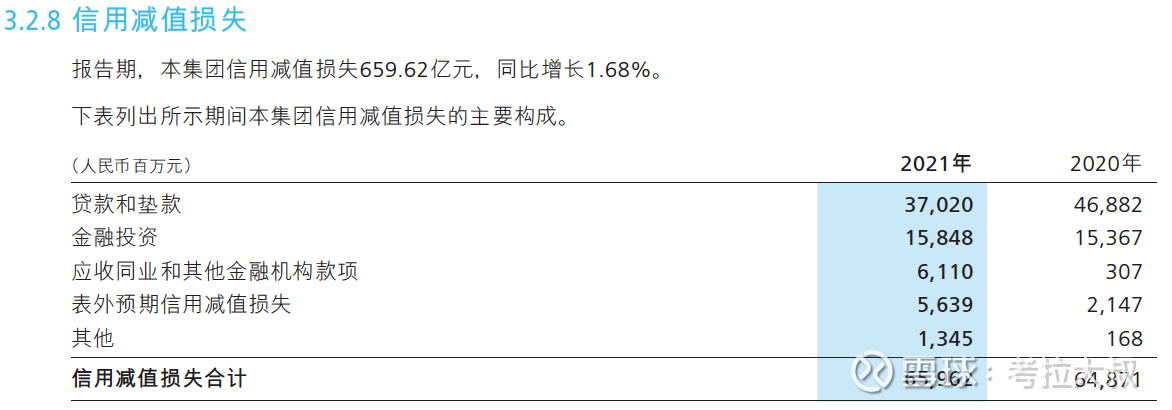

Figure 2 – Composition of Credit Impairment Losses in China Merchants Bank’s 2021 Annual Report

As shown in Figure 2, among the credit impairment losses of China Merchants Bank, the proportion of credit impairment losses on loans is roughly 50%, which is relatively low among joint-stock banks and large state-owned banks. Most bank loans have credit impairment losses. Losses account for 80%, and even many banks will exceed 90%.

Therefore, the subsequent content of this article will analyze the loan provision (loan loss provision) in detail.

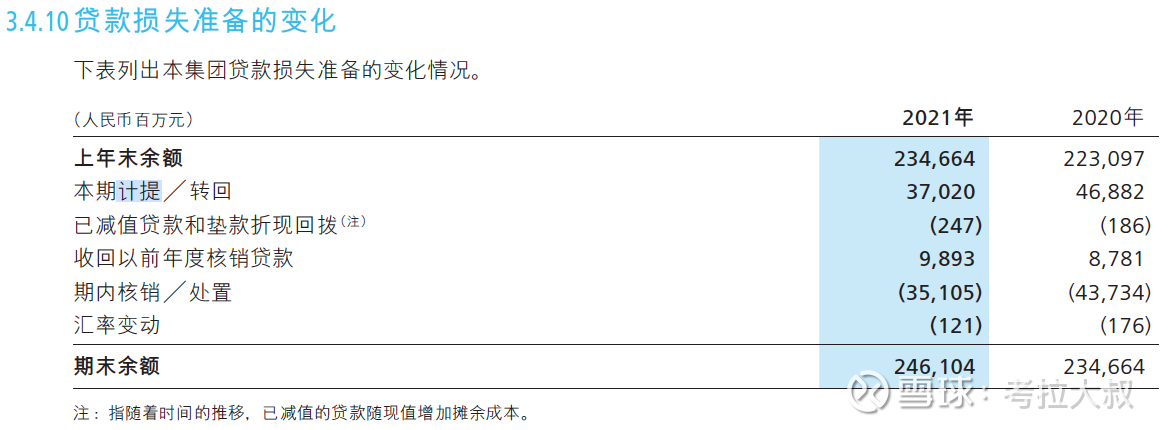

Figure 3 – Changes in Loan Loss Provisions in China Merchants Bank’s 2021 Annual Report

As mentioned earlier, the accumulation of credit impairment losses will form provisions year by year. As shown in Figure 3, China Merchants Bank’s loan provision balance at the end of 2020 was 234.664 billion, and the provision balance at the end of 2021 increased to 246.104 billion, of which 2021 The annual accrued loan loss is 37.02 billion (the second row of the table in Figure 3, the first row of the table in Figure 2). Usually, I will regard the items other than the provision in Figure 3 as a whole, that is, net write-offs, and the net write-off of loans of China Merchants Bank in 2021 is 25.58 billion. As for why I look at it this way, it is just a personal habit, in order to simplify the horizontal and vertical between banks. Compared.

Calculation formula:

Balance of provision at the end of the period = balance of provision at the beginning of the period + provision for the current period – net loan write-off during the period

Net loan write-off during the period = balance of provision at the beginning of the period + provision for the current period – balance of provision at the end of the period

The above is the accumulation process of the bank’s loan loss provision (loan provision). Although it is not clearly stated in what form the provision exists, we can see that the provision for loans will increase with the accrual of loan losses, and will also decrease with the write-off of loans. This implies that loan provisions exist in the form of loans. When accruing loan provision, the amount corresponding to a loan is transferred out of the loan account and transferred into the provision account at the same time (virtual bookkeeping method); when writing off a loan, it is directly transferred from the provision. The amount corresponding to the loan is erased from the account (the loan is no longer in the loan account at this time, but was transferred to the provision account when it was previously accrued).

The bank’s balance sheet

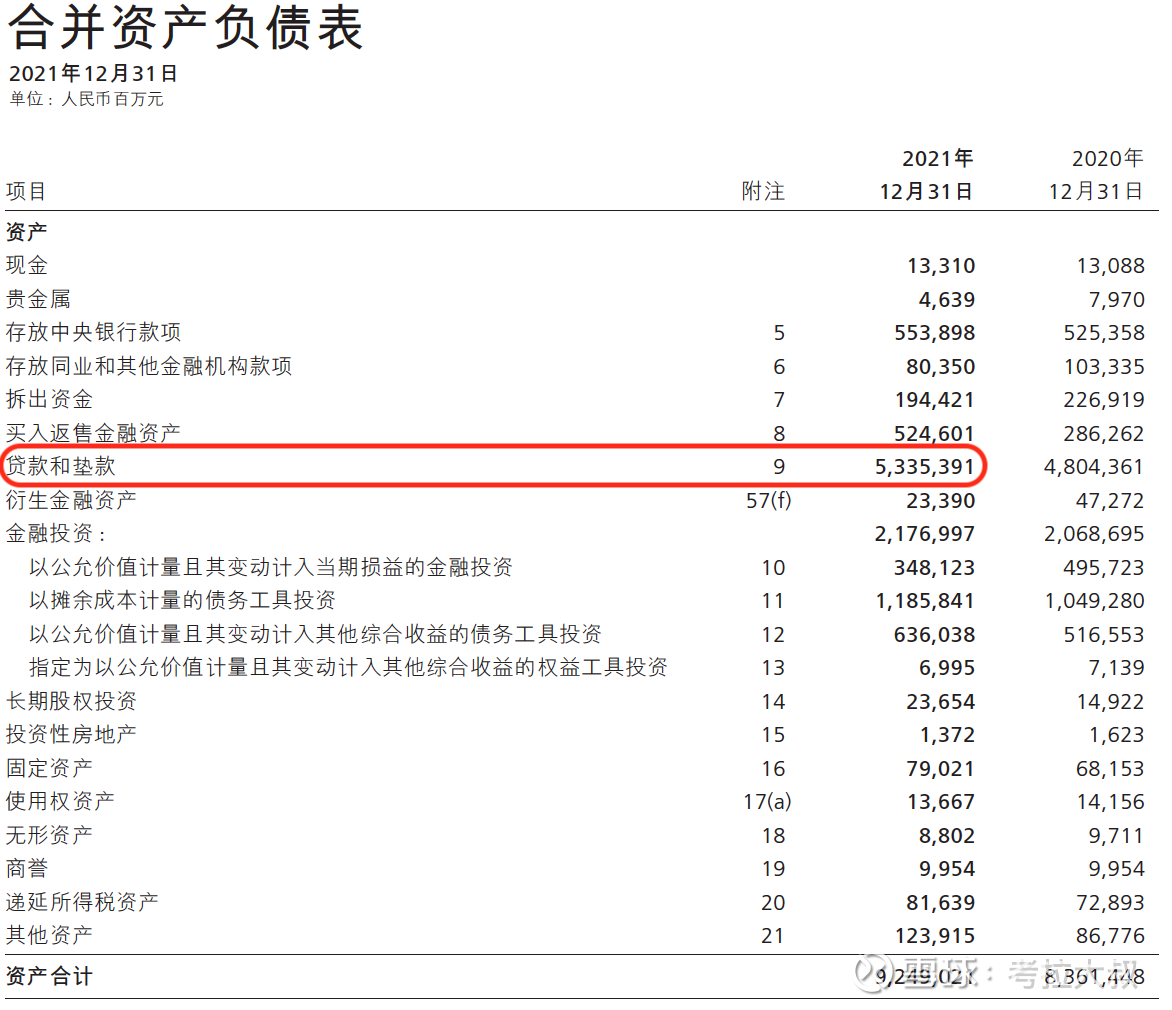

Figure 4 – China Merchants Bank 2021 Annual Report Consolidated Balance Sheet

As shown in Figure 4, in the 2021 annual report of China Merchants Bank, the cash balance is 13.31 billion, and the amount deposited in the central bank is 553.898 billion. These two items have given clear values, which can reflect from the side that the provision is neither cash nor money deposited in the central bank. Otherwise, it means that the bank has a small vault, and it has not disclosed in detail how to use it, or even If there is no supervision, it means that it may be misappropriated, which means a huge risk. At least in the more than ten years that I have invested in banking stocks, I have never seen or even heard of the relevant regulations on the management of provision funds, so I can basically confirm that provisions are neither cash nor deposits.

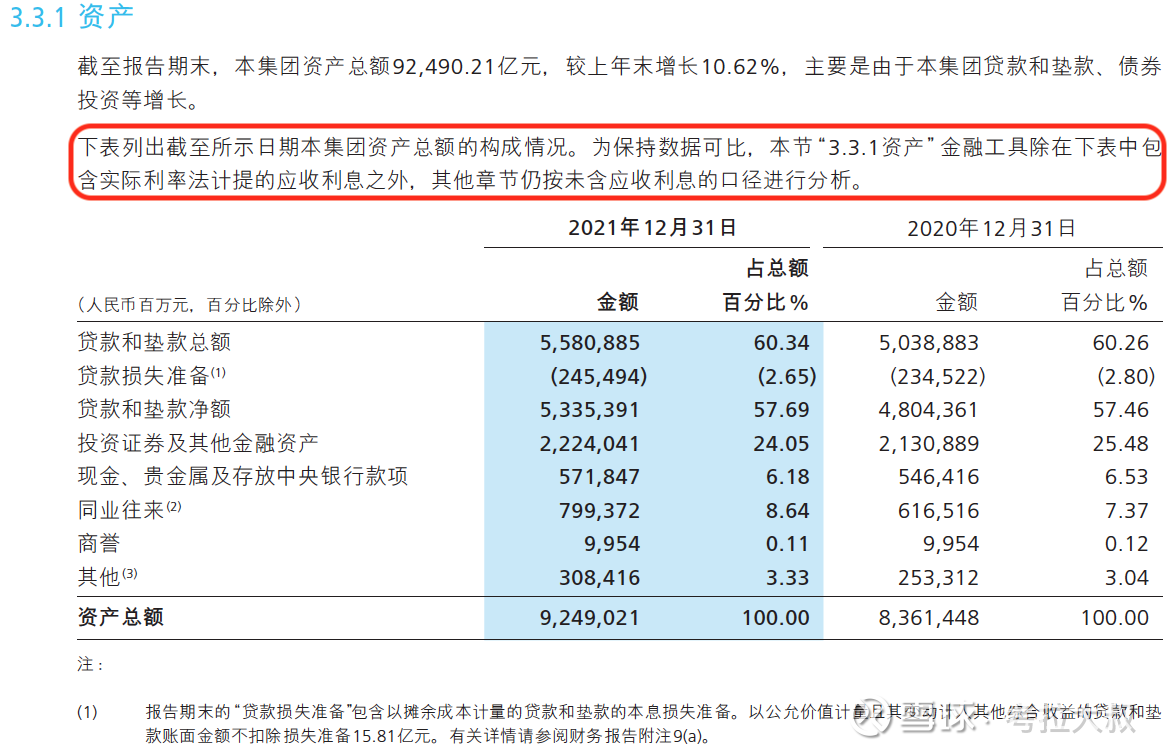

In Figure 4, the loan scale disclosed by China Merchants Bank’s 2021 balance sheet is 5,335.391 billion. There is no detailed explanation here, but in fact, the data here is the net loan amount, excluding loan impairment provisions. This point is disclosed in detail in “3.3 Balance Sheet Analysis” in Management Discussion and Analysis.

Figure 5 – China Merchants Bank 2021 Annual Report 3.3 Balance Sheet Analysis

As shown in Figure 5, China Merchants Bank uses the net loan amount (that is, the total loan minus the loan loss provision) instead of the total loan amount when calculating the total assets. The reason for this is that the total loan amount includes some unrecoverable principal and interest Loans, this part of assets can be regarded as assets that have been lost and should be deducted from the total assets, similar to the fact that in the financial report of Shuanghui Development, the inventory depreciation losses of the current period (the price of pork fell, the inventory depreciated correspondingly), and the amount of the provision should be deducted from the inventory. The function is to deduct this part of the assets by means of bookkeeping transfer.

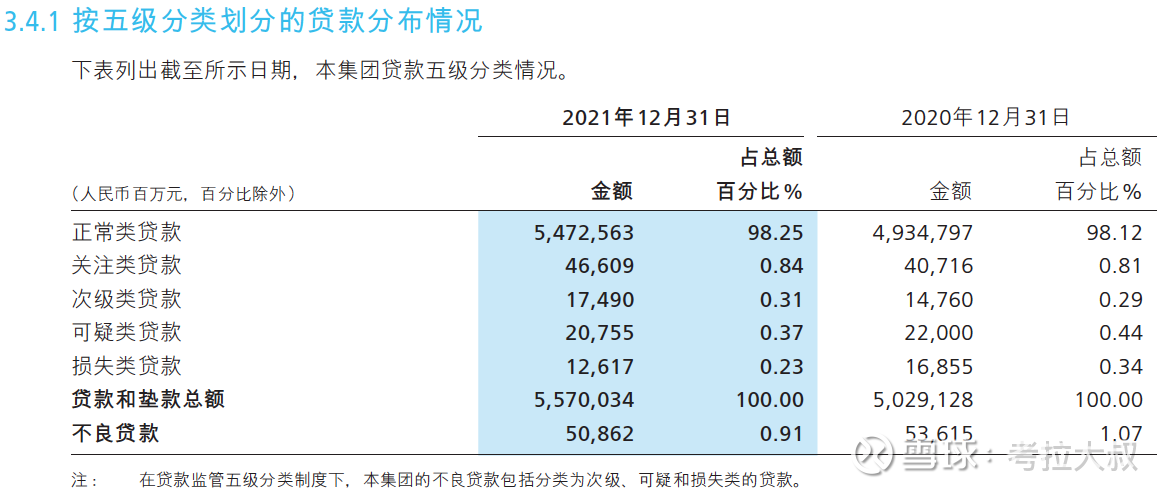

Figure 6 – Five-level classification of loans in the 2021 annual report of China Merchants Bank

As shown in Figure 6, as of the end of 2021, China Merchants Bank’s total loans included 50.862 billion non-performing loans and 46.609 billion special mention loans. Most of these non-performing loans have been unable to recover the principal and interest, and a large part of the special mention loans may be The principal and interest cannot be recovered in the future, and even normal loans may not be able to recover the principal and interest in the future. Therefore, these loans should no longer be included in the assets. They are all transferred to the provision year by year in the form of impairment losses. inside. In other words, the provision corresponds to the assets that have been lost or may be lost in the future. Specifically, the provision for loans corresponds to the loans that have or may not be able to recover the principal and interest in the future.

Calculation formula:

Total loans = normal loans + special mention loans + non-performing loans (substandard loans + doubtful loans + loss loans)

Net loan amount = total loan amount – loan loss allowance

Net loan amount = normal loan + special mention loan + non-performing loan – loan loss provision

Careful friends should have discovered that the total amount of loans in Figure 6 is 5,570.034 billion, while the total amount of loans in Figure 5 is 5,580.885 billion. The two are not consistent. This point is explained in the second paragraph of the text in Figure 5. The total loan here includes the interest receivable, while the total loan in other places does not include the interest receivable, that is to say, the total loan ratio in Figure 6 The 10 billion less in 5 is the interest receivable.

The net loan amount in Figure 5 is consistent with the loan amount in Figure 4, which means that the bank uses the net loan amount after deducting loan provisions when calculating total assets and net assets.

V. Amortized cost and fair value

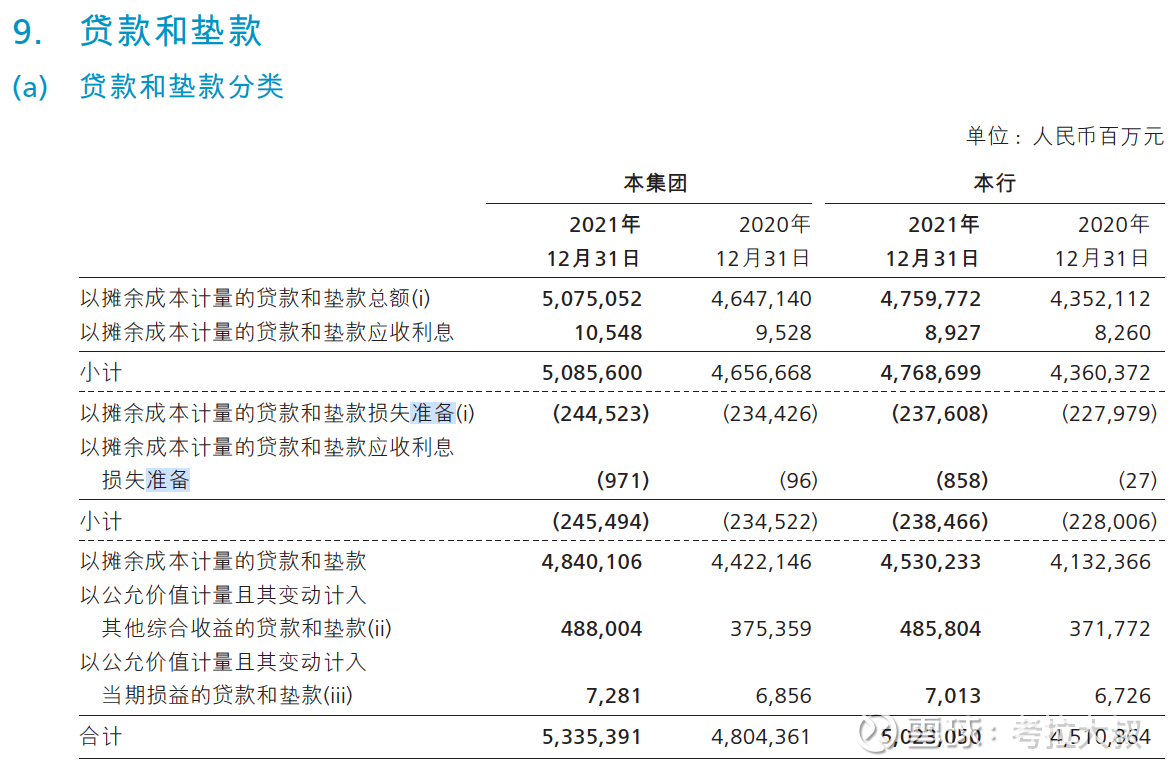

As already mentioned in Note 1 in Figure 5, when calculating the net loan amount, the loan loss allowance deducted from the gross loan only includes the loan loss allowance measured at amortized cost, and does not include the loan measured at fair value Loss preparation. Details are set out in Appendix 9.

Figure 6 – Appendix 9(a) of China Merchants Bank’s 2021 Annual Report

Figure 7 – Appendix 9(a)(ii) of China Merchants Bank’s 2021 Annual Report

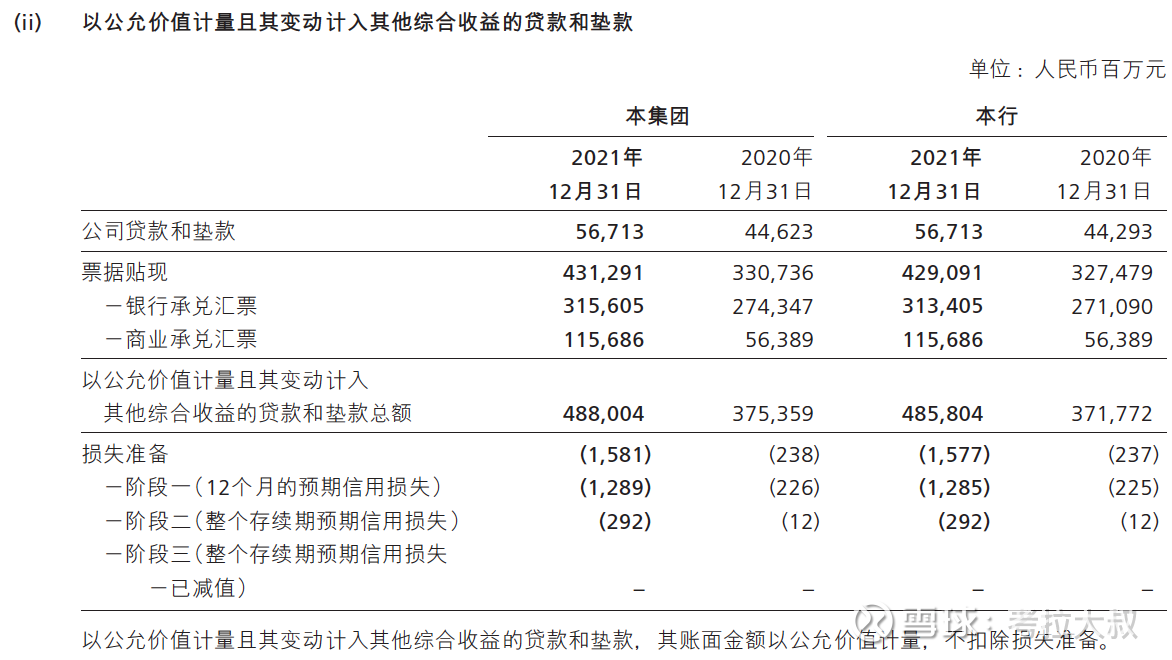

From Figures 6 and 7 in Appendix 9(a), we can clearly see that the net loan amount includes both the net loan amount measured at amortized cost and the gross loan amount measured at fair value.

So why are loans measured at amortized cost using the net amount and loans measured at fair value using the gross amount? Or why is there no deduction for loan loss provisions measured at fair value?

Because it has been clarified in the relevant definition of amortized cost, it is necessary to deduct the impairment loss that has occurred. Amortized cost is similar to the discounted value of an asset at a certain point in time. This discounted value is usually linear, while some assets have fair value at the same time. The two may be inconsistent because assets can be discounted or In a premium transaction, the transaction price will generate a fair value, but the amortized cost can literally be seen to be independent of the transaction price.

The approximate calculation formula (may not be rigorous enough, for reference only):

Amortized cost of a loan at the end of the period = loan amount at the beginning of the period – principal repaid – impairment losses incurred + interest receivable at the end of the period

Therefore, the value of amortized cost is a function of time, for example, the interest receivable will change over time, regardless of the current transaction price.

For assets measured at fair value, because there is a fair price, changes in fair value can be used to represent changes in their value, and changes in this value are usually directly included in current profits (profits and losses), so the assets measured at fair value should be provided for There is no need to deduct it from the total asset, which is the tradable value of the asset.

The simple understanding is that the transaction value is not considered in the way of amortized cost measurement, so it is necessary to estimate the discounted part of the asset when it is realized (for banks, it is non-performing assets, for non-bank enterprises, it is usually inventory depreciation losses) and Deducted; and the transaction value has been considered in the way of fair value measurement (the issue of discount has been reflected in the fair value), so there is no need to reconsider the issue of discount.

Recalling the introduction to the provision for Shuanghui Development in the previous article, the loss of inventory depreciation caused by the fall in pork prices is similar to the change in fair value here, which is directly reflected in the inventory value at the end of the period. Shuanghui’s provision is for the ham sausage and chilled meat stored on channel shelves or in Shuanghui’s cold storage. When a part of it expires and deteriorates because it cannot be sold in time, Shuanghui will use the provision to write off this part of the inventory. , so the inventory value in Shuanghui’s balance sheet is the net inventory value after deducting provisions, which is similar to the bank’s net loan amount.

6. Conclusion

To sum up, the bank’s provision does not exist in the form of cash or deposits. It is a part of the assets that is transferred from the assets by bookkeeping every year, and is accumulated year by year, so it is a virtual concept, a virtual Collection of assets. In the income statement (profit and loss statement), it is reflected as the current cost; in the balance sheet, the provision corresponds to those assets whose principal and interest cannot be recovered or those whose principal and interest may not be recovered in the future. These assets are surrounded by an invisible pen got up and was marked as provision.

Therefore, we don’t have to worry about whether the high-provisioned banks are wasting funds. Instead, we should pay attention to the probability of recovering the principal and interest of these problematic assets corresponding to the provisioning in the future. If the provisioning can be recovered, it may generate additional profits. If the provision is not returned, it will disappear as the asset is written off.

However, it must be considered that after the disintegration of Jinben in the 1970s, the bank’s business model has become an infinite game. In theory, the scale of assets can grow infinitely (loans derive deposits to create money M2), which means As a result, we may never see the end result of the provision for problematic assets from the bank statements. The bank’s loan scale will expand indefinitely in a model of borrowing new to repay the old, and the provision scale will also expand infinitely with the expansion of the loan scale.

So, can banks be able to significantly improve their performance by releasing provisions?

To be continued.

[This article is original, your likes, shares and comments are the greatest support for my continuous creation! At the same time, you are also welcome to pay attention to “Uncle Koala Snowballing” and discover my sharing in time! 】

related articles:

“In what form do bank provisions exist? Where is it? (1) Starting from the provision of Shuanghui Development”

$ China Merchants Bank (SH600036)$ $ Industrial Bank (SH601166)$ $ Agricultural Bank (SH601288)$

@Today’s topic @snowball talent show #snowball star plan#

There are 29 discussions on this topic in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/2836571636/227150931

This site is for inclusion only, and the copyright belongs to the original author.