Welcome to the WeChat subscription number of “Sina Technology”: techsina

Text / Jia Yang

Source/20she (ID:quancaijing_20she)

Kuaishou issued a Q2 financial report that was much better than the same period last year.

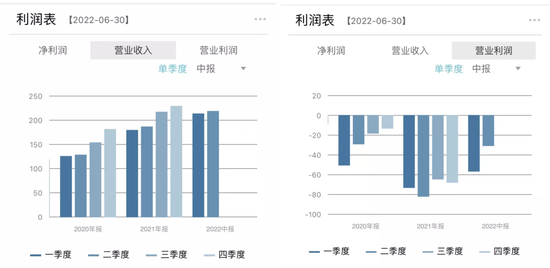

The biggest bright spot is not the revenue (Q2 revenue of 21.7 billion increased by 13.4% year-on-year, only maintaining a 3% month-on-month growth, which is still down from the peak revenue of Q4 last year), but the loss reduction that greatly exceeded market expectations (Q2 Adjusted net loss was 1.312 billion, down 72.5% year-on-year). In this quarter, after Kuaishou separated the international and domestic markets, the Q2 domestic market achieved positive operating profits.

Kuaishou’s quarterly operating income and operating profit

Kuaishou’s quarterly operating income and operating profitThe direct reason is that Kuaishou has reduced sales and marketing expenses, from 11.3 billion yuan in the same period last year to 8.8 billion yuan, and the sales expense ratio has also dropped from 58.9% to 40.4%.

This is an effective boost for the market.

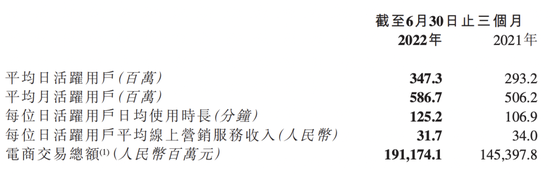

And in Q2, which was severely affected by the epidemic, Kuaishou’s two business data indicators continued to grow vigorously – the average DAU increased by 18.5% year-on-year to 347 million, and the e-commerce GMV reached 191.2 billion yuan, which was higher than the company’s previous guidance. This shows that the Kuaishou business has relatively strong resilience to epidemic risks.

But after talking about these positive factors, let’s look at the most core issue—the ability to make money, but it’s hard to be optimistic.

There are three sources of income for Kuaishou, online marketing, live broadcast, and others. The growth of online marketing has begun to be sluggish, and the live broadcast has lost its ability to grow due to industry trends and policies. “Other businesses” driven by e-commerce also account for a low proportion of overall revenue due to a low monetization rate (about 1%).

The problem with Kuaishou is that a company that is still bleeding profusely is trying its best to reduce costs and increase efficiency, and is resilient in the face of the epidemic, but its ability to make money has slowed down. When will the gap in losses be made up?

Expensive moat, after all, it is established

If we say that in the past few quarters, the biggest question investors have about Kuaishou is that the marketing expenses spent in order to maintain user growth are too high, resulting in Kuaishou’s continuous loss. Kuaishou is buying users and scale at a loss. According to Dolphin Investment Research, Kuaishou’s single-user acquisition and maintenance costs reached a high of over 22 yuan in the first and second quarters of last year.

So from this quarter, Kuaishou began to emphasize “moderation” and changed to a cheaper way of pulling new products. According to Jin Bing, CFO of Kuaishou, at the performance meeting, “We have explored the growth path of social pull in a targeted manner. The new users introduced through social pull have better performance in both short-term and long-term retention rates. Users The need for self-presentation and belonging is met through socializing.”

If Kuaishou’s previous promotion was mainly through the “online earning” model, then it is now beginning to emphasize the use of user social relationships to enhance the sense of value acquisition.

We can see that Kuaishou breaks through in terms of user activity, stickiness and usage time when there is a bottleneck in absolute share growth. The MAU of Kuaishou’s main station has basically declined year-on-year in the past few quarters, but the overall DAU of Kuaishou has continued to rise. The average DAU of Kuaishou in Q2 increased by 18.5% year-on-year to 347 million, a record high. The DAU/MAU ratio of Kuaishou app Q2 increased to 59.2%, and the average daily usage time of daily active users increased by 17.1% year-on-year to 125.2min.

Kuaishou has begun to emphasize one indicator more and more: interrelated users. As of the end of June 2022, the number of cross-related user pairs on the Kuaishou app has exceeded 20 billion, a year-on-year increase of 65.9%.

When we analyze the business model of an Internet product, network effects are the key to its success—whether each new user joins can make the product/service/experience more valuable to other users. To a certain extent, Kuaishou’s “network effect” has begun to play the value it should have played.

Of course, the above-mentioned “social relationships” cannot produce network effects alone, and they need to cooperate with each other in terms of content supply, product function design, and traffic distribution methods.

For example, the blue-collar recruitment track that Kuaishou entered is a lower-cost leveraged content and service than the previous high-cost Olympic and Winter Olympics content. The number of active users of “Quick Recruitment” in Q2 reached 250 million, a month-on-month increase of 90%.

Kuaishou CEO Cheng Yixiao said at the performance meeting that there was a “benign scissors difference” between the growth of Kuaishou DAU and the decrease in the maintenance cost of a single DAU, and the ROI of new users in the first year continued to increase year-on-year and month-on-month. “This gives us more confidence to make strides towards our 400 million DAU user target.”

In short, from the results, Kuaishou’s total traffic (daily active * average daily user time) increased by 38.7% year-on-year, while marketing and sales expenditure decreased by 22.3% year-on-year, and traffic costs continued to decrease.

For Kuaishou, this is a growth method that is more suitable for the current macro environment and more suitable for the characteristics of its own platform.

real danger

In addition to “cost reduction” in marketing expenses, technology costs and live broadcast profit sharing costs are also improving. Jin Bing introduced that in the first half of the year, the total domestic traffic increased by more than 40% year-on-year, but the ratio of Kuaishou bandwidth and server costs to revenue fell by more than 5%. According to Dolphin Investment Research, the share of live streaming for guilds/hosts may have dropped from 70% in the first quarter to 63%.

This cost reduction and efficiency increase leads to a fairly good data. That was the first profit in the domestic market.

According to Kuaishou’s Q2 financial report, for the first time, the domestic and overseas operations were displayed separately. Kuaishou’s domestic business achieved its single-quarter profit target two quarters ahead of schedule, with Q2 operating profit exceeding 93 million yuan.

In the total revenue of 21.7 billion yuan in Q2, the contribution of online marketing services (advertising), live broadcast and other services accounted for 50.7%, 39.5% and 9.8% respectively. Kuaishou commercialization is better than many Internet companies in resisting the falling gravity of the Internet advertising market. As a new pillar of revenue cultivated by Kuaishou after the live broadcast business, advertising Q2 increased by 10.5% year-on-year, which is extremely eye-catching compared to the previous 18% year-on-year decline in Tencent’s advertising business.

But the problem behind these optimistic figures is that the growth engine of advertising is also starting to falter.

Q2 advertising revenue of 11 billion yuan increased by 10.5% year-on-year, and the growth rate has slowed down significantly. The growth rate in the same period last year was 156.2%, and the growth rate in Q1 was 32.6%; compared with the 11.4 billion yuan in Q1, there was a downward trend, with a decrease of 3.5%.

In the current environment, advertisers are more demanding on conversion requirements. According to “LatePost”, many analysts have estimated that Kuaishou’s Q2 advertising revenue has been declining if excluding advertising brought by e-commerce business. Ma Hongbin, who has been in charge of commercialization for two years, said in May that he might be questioned by the Economic and Management Commission because of the poor performance of Q2 commercialization. Before the release of the financial report, Ma Hongbin transferred to overseas business.

In-platform advertising brought by the Kuaishou e-commerce business is increasingly regarded as the resilience core of the advertising business. That is, the “inner cycle” that Cheng Yixiao repeatedly mentioned in the previous quarters.

Therefore, in the second half of last year, Kuaishou began to promote the “new market business”, and this year, it proposed a new e-commerce strategy of “big and fast brands”, hoping to accelerate the upgrade of the industry with a white brand and guide the white brand to upgrade to a “fast brand”. ”, allowing merchants in the Kuaishou ecosystem to increase their distribution on the site after making profits.

But obviously, the effect of “big and fast brand” is hard to resist the slowdown of external circulation. Judging from the Q1 financial report, although the number of advertisers increased by 60% year-on-year, it only drove a year-on-year increase of 32.3%. In Q2, the number of advertisers on the Kuaishou platform increased by more than 90% year-on-year, while the growth rate of advertising revenue remained at only 10.5%. This shows that the willingness and budget of these small and medium-sized businesses newly added by Kuaishou are not as good as those of the previous advertisers.

While Kuaishou veterans have become stickier and longer, a single user has not contributed more performance conversions. In the second quarter, Kuaishou’s per capita online marketing service revenue from daily active users was 31.7 yuan, down 6.8% year-on-year, and fell for two consecutive quarters. From the perspective of ad inventory, Kuaishou’s ad load rate has actually declined without considering the eCPM price fluctuations.

According to media reports, Kuaishou’s advertising revenue target for this year is 59 billion, and it plans to break even by the end of the year. In the first half of the year, the quota of 22.357 billion yuan was completed. At present, it seems that the pressure to achieve this goal is not small.

When it comes to the e-commerce business itself, Q2’s GMV reached 191.2 billion yuan, a year-on-year increase of 31%, higher than the consensus forecast by Bloomberg. Cheng Yixiao mentioned at the performance meeting that in the medium and long term, I believe that the GMV of the live broadcast e-commerce industry with short video platforms as the core has the opportunity to reach 6 trillion yuan, and Kuaishou will continue to strengthen our dominant position in the industry.

The “other” business income brought by e-commerce and other services was 2.12 billion yuan, a year-on-year increase of 7%. It can be roughly calculated that the comprehensive commission rate is 1.11%.

The live broadcast e-commerce represented by Kuaishou and Douyin is already a rare track with high growth in the entire e-commerce industry. In the case of logistics shutdown during the epidemic, live broadcast e-commerce was relatively less affected, capturing the needs of merchants for deterministic conversions and promotions.

For a longer period of time in the future, in the face of the low overall consumption willingness of the people and the relatively low purchasing power of Kuaishou platform users, how to move up Kuaishou is a more core proposition than saving food and clothing.

This article is reproduced from: http://finance.sina.com.cn/tech/csj/2022-08-25/doc-imizmscv7730392.shtml

This site is for inclusion only, and the copyright belongs to the original author.