(The picture comes from the official Weibo of Midea Group)

(The picture comes from the official Weibo of Midea Group)Welcome to the WeChat subscription number of “Sina Technology”: techsina

Text | Hernanderz

Source: Value Institute

Revenue and net profit attributable to the parent have both achieved year-on-year growth, and its five business segments have also recorded growth of varying degrees. Midea’s semi-annual report is basically in line with market expectations. Among them, in terms of revenue alone, Midea’s performance is worthy of recognition, whether it is a vertical comparison of historical performance or a horizontal comparison of major competitors such as Gree and Haier Zhijia. However, the net profit margin that is significantly behind Gree and the current situation of increasing revenue but not profit is still a cause for concern.

In fact, the profit data of the three white goods giants are not optimistic, and they have all declined significantly compared with the peak period. Behind this, it reveals the coldness of the entire home appliance industry, especially the shrinking of the C-end consumer market. Data show that in the first half of this year, the sales volume of the national home appliance market was about 360.9 billion yuan, down 11.2% year-on-year. Only the air conditioner category achieved growth against the market.

The weakness of C-end consumption is related to many factors: the decline of related industries such as real estate, changes in consumer attitudes, and so on. Nowadays, the C-end business is not easy to do, and looking for growth at the B-end will undoubtedly become a new trend.

However, Midea’s B-end business is not smooth sailing. This transformation is more like a tough battle that has to be fought, but no one is sure to win.

Midea’s semi-annual report announced

Revenue exceeded expectations, net profit margin was not as good as Gree

On the evening of August 30, Beijing time, Midea Group released its financial report for the first half of fiscal year 2022. In the context of the overall downturn in the home appliance market, Midea, the industry leader, still handed over a report card that met expectations: both revenue and net profit attributable to the parent achieved year-on-year growth, and its five business segments also recorded growth of varying degrees. . But some old problems remain: high costs and a net profit margin that lags behind rivals such as Gree.

In any case, Midea’s position in the domestic home appliance industry cannot be shaken. Taking Midea’s financial report as an incision, we may explore the current situation of the entire domestic home appliance industry.

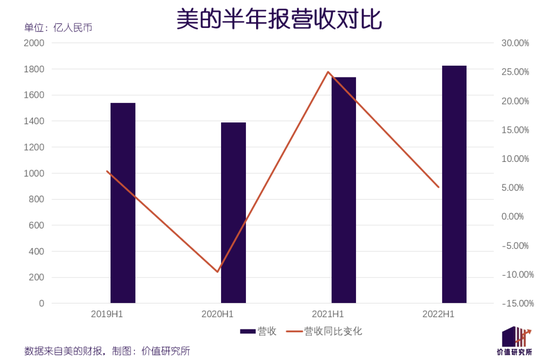

Let’s look at revenue first. In the first half of this year, Midea achieved total revenue of 182.661 billion yuan, a year-on-year increase of 5.09%, slightly exceeding market expectations. In terms of revenue alone, Midea’s performance is worthy of recognition, whether it is vertical comparison of historical performance or horizontal comparison of major competitors such as Gree and Haier Zhijia.

Historical data shows that from 2018 to now, except for the 8.29% year-on-year contraction in revenue in the first half of 2020 due to the epidemic, the rest of the year has achieved year-on-year growth. Of course, in the first half of last year, thanks to the low year-on-year base, Midea’s revenue recorded a year-on-year growth of 24.98%. This explosive growth trend is difficult to continue. However, the revenue growth rate in the first half of this year is not much different from that before the epidemic, indicating that everything is getting back on track.

In terms of horizontal comparison, Haier Zhijia and Gree Electric recorded revenue of 121.858 billion yuan and 95.807 billion yuan respectively in the first half of this year, both significantly behind Midea, whose dominance is still quite stable. Comparing the year-on-year growth rate, Midea lags behind Haier Zhijia’s 9.07%, but ahead of Gree’s 4.13%, but basically at the same level.

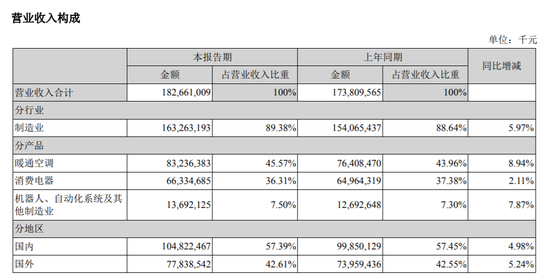

Look at the revenue structure. In the first half of the year, Midea’s Building Technology Division, Industrial Technology Division, Robotics and Automation Division, and Digital Innovation Business Division all achieved year-on-year revenue growth, but the revenue growth rate of the Smart Home Division, the number one cash cow, was relatively lagging behind.

Data show that in the first half of the year, the revenue of Midea’s smart home business unit was 125.9 billion yuan, a year-on-year increase of 3.5%. The fastest growing is the digital innovation business department, which has the lowest revenue share, with revenue of 5.2 billion yuan in the first half of the year, a year-on-year increase of 42.4%. In addition, the building technology division, which had a revenue of 12.2 billion yuan in the first half of the year, also recorded a year-on-year growth of 33.09%.

If you look at specific products, HVAC and consumer appliances contributed the most. The former’s revenue in the first half of the year reached 83.236 billion yuan, an increase of 8.94% year-on-year, and its revenue accounted for 45.57%; the latter’s revenue increased by 2.11% year-on-year to 66.335 billion yuan, and its revenue accounted for 36.31%. In general, the basic disk of Midea’s white goods is still very stable.

(The picture comes from the financial report of Midea)

(The picture comes from the financial report of Midea)On the profit side, however, the picture is less optimistic.

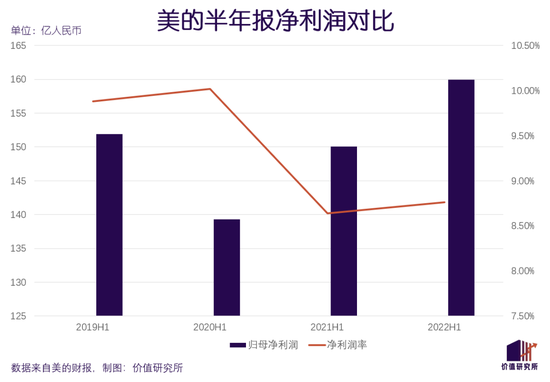

According to the financial report data, the net profit attributable to the parent company of Midea in the first half of this year was 15.995 billion yuan, a year-on-year increase of 6.57%, a slight decline from 7.76% in the same period last year, but the gap was not large; the gross profit margin during the reporting period increased by 1.2 percentage points year-on-year to 24.43%, in line with market expectations.

The main problem of Midea is the slightly struggling net profit margin. Data show that in the first half of this year, the net profit margin of Midea was 8.76%, slightly higher than the 8.64% in the same period last year, but lower than the level before the epidemic. In the first half of 2019, Midea’s net profit margin reached 9.88%, and it has maintained year-on-year growth for many consecutive years.

Compared with Gree horizontally, the disadvantage of Midea’s net profit margin is even more obvious. In the first half of this year, Gree’s net profit margin recorded 12.04%, and the corresponding net profit attributable to the parent was 11.466 billion yuan, a year-on-year increase of 21.25%. Midea used nearly twice the revenue of Gree to exchange only about 4.5 billion higher profits than the other party, and its performance may not be satisfactory to investors.

When it comes to the status quo of Midea’s increasing revenue but not increasing profits, another important data has to be drawn – cost.

In the first half of the year, Midea’s sales, management, R&D and financial expenses increased overall compared with the same period last year, and the cost pressure became more and more heavy. Among them, the major sales expenses recorded 14.698 billion yuan, a year-on-year increase of 5.36%; management and R&D expenses recorded 4.951 billion yuan and 5.865 billion yuan, respectively, a year-on-year increase of 16.44% and 10.36%.

Of course, rising costs and falling profits are not the only cases of Midea. Old rival Gree’s net profit margin in the first half of this year was also slightly lower than the 15% at its peak in 2018-2019.

The collective slowdown of the giants is easily reminiscent of the overall depression in the home appliance market.

Since 2019, the C-end home appliance market has shown signs of recession. So far, the situation does not seem to have changed, but has become more serious.

C-end market enters winter

High cost drags down the three giants of white electricity

It has long been the consensus of the industry that the life of the home appliance industry is not easy.

According to the report of the China Household Electrical Appliances Association, the total profit of China’s home appliance industry last year was about 121.8 billion yuan, a slight increase of 4.5% year-on-year, far lower than the 15.5% revenue growth rate. By 2022, even the fig leaf of income cannot be kept. The same data from the China Household Electrical Appliances Association shows that the sales volume of the national home appliance market in the first half of this year was about 360.9 billion yuan, down 11.2% year-on-year. Only the air conditioner category achieved growth against the market.

As for other major home appliance categories, the situation is even less optimistic. Data from Aowei Cloud also shows that in the first half of this year, the retail sales of color TVs, refrigerators (including freezers) and washing machines all fell year-on-year. Except for washing machines, the other two categories fell by more than double digits.

It can be said that Midea’s plight today is the epitome of the entire home appliance industry.

In the home appliance industry, the dominance of the C-end market is still unshakable. The depression of the industry is also closely related to the sluggish C-end consumption.

The decline of C-end home appliance consumption is naturally related to many factors. There are objective constraints, such as the decline of related industries such as real estate; however, the defects in the business strategies of home appliance companies and the changes in consumer attitudes are also closely related to the shrinking market.

On the one hand, as we all know, the real estate industry and the home appliance industry have always been in a state of deep bundling, which can be said to be both prosperity and loss. At the beginning of 2019, the real estate winter, which was infinitely amplified by the epidemic, had a direct impact on the home appliance industry.

Statistics show that the development of the domestic real estate industry reached its peak in 2017, and the spillover effect on the home appliance industry reached the highest level. That year, the sales of home appliances brought by the delivery of new houses accounted for more than 20% of the total retail sales of home appliances. In 2019, affected by policies and other factors, the real estate industry turned from prosperity to decline, and the home appliance industry also lost its strongest support.

On the other hand, after the outbreak of the epidemic, the consumption concept of C-end consumers has also changed greatly. According to the report of the National Bureau of Statistics, in the first three quarters of last year, the fastest growth rate of consumer spending was 68% for education and culture and 19% for medical services, while the growth rate of consumer spending was only 15%. Under the impact of the epidemic, more consumers are spending money on health care and long-term education, and their desire to spend on durable goods such as home appliances is declining.

The house leakage happens to rain overnight, and it is more suitable to describe the home appliance industry at this stage. Due to the blocked supply chain and the soaring prices of raw materials such as aluminum and copper, many home appliance manufacturers can only pass on the cost pressure to consumers by raising prices. As a result, consumers are more depressed, and C-end consumption is becoming more and more sluggish.

In the first half of the year, the air-conditioning category with the strongest sales volume faced the challenge of falling average sales price and shrinking proportion of high-end products. According to the statistics of Aowei Cloud, the average sales price of domestic online air conditioners fell by 2.6% in the first half of this year, and the proportion of sales of high-end products of 9,000 yuan and above also declined.

In the past few years, Haier, Midea and other brands have vigorously developed high-end terminal brands, trying to seize Gree’s air-conditioning market share. In the new situation, they may need to re-examine the effect of premiumization strategy.

For a long time, major home appliance giants have regarded the C-end as their business focus. This strategy is also in line with the actual situation that the domestic home appliance market is dominated by household and personal consumption. However, the market is always changing, and the strategies of home appliance manufacturers must also keep pace with the times.

Nowadays, the C-end business is not easy to do, and looking for growth at the B-end will undoubtedly become a new trend.

Fully embrace the B side

Midea’s betting on more than just home appliances?

Midea has been shouting the slogan of expanding the B-end business for a while.

As early as December 2020, when the five business segments were adjusted, Midea established a new strategy of focusing on B and C. At the annual operation and management meeting at the beginning of this year, Midea CEO Fang Hongbo emphasized the decision of the group’s top management through a speech to all staff: insist on taking the B-end business as the second engine and create a new situation.

“In an unpredictable market, step-by-step means mediocrity. Regardless of business model or technology, continuous change and innovation are required.”

However, at this stage, it is difficult to say how successful Midea’s B-side business has been. Data shows that in the first half of this year, Midea’s B-side business revenue accounted for about 24%, an increase of nearly 3 percentage points from the previous fiscal year. The biggest contributors were the Building Technology Division and the Robotics and Automation Division. No matter in terms of revenue share or market share, the core position of the C-end business is difficult to shake in a short period of time.

Old rivals Gree and Haier Zhijia also have a similar situation. In the first quarter of this year, Gree vigorously praised the business performance of the B-end in the financial report, especially the hot sales of air-conditioning products. However, in the semi-annual report, Gree’s promotion of the B-end business has weakened a lot. Although no specific revenue data has been disclosed, it is not difficult to guess the fact that Gree’s B-end business is blocked.

Objectively speaking, the B-end electrical appliance market does have potential and room for development, but the limitations are also obvious – the B-end increment is only concentrated in a few categories such as central air conditioners and freezers, and the replacement rate is low, and companies are not willing to change. High, it is difficult to meet the expansion ambitions of Midea, Gree, Haier and other giants at the same time.

Take central air conditioning as an example. According to RT rail transit statistics, the three giants Midea, Haier, and Gree all account for about 20% of the important air conditioning market in the national rail transit system. They are comparable in strength to each other, and their penetration rate is growing slowly. The market ceiling is already looming.

However, in the view of the Institute of Value (ID: jiazhiyanjiusuo), the growth potential of the B-end is more worth looking forward to than the C-end. The ambitions of Midea and Gree may also exceed our expectations-their imagination of the B-side business has long been more than just traditional white goods.

In May of this year, the Maanshan Intelligent Industrial Park, which Gree invested 6 billion yuan, officially broke ground. According to the officially disclosed plan, Gree will build an intelligent manufacturing base in the industrial park, mainly serving Gree’s electrical and electrical business and smart home appliance business, and will develop and provide smart factory solutions, automated production line solutions and customization for corporate customers. Industrial robot applications.

On Midea’s side, combing through its existing business lines, it can be found that its layout on the B-end in the past two years has long gone far beyond the scope of home appliances.

The Building Technology Division, which completed its business upgrade in September last year, focuses on building digital services related to B-end enterprise customers, mainly providing customers with overall construction solutions and electrical products such as HVAC equipment. In the past, the successful bid for the Beijing Winter Olympics and the Dubai World Expo venue equipment supply project, as well as the cooperation with Hilton, InterContinental Hotels Group and other customers, have provided Midea with rich operational experience.

In addition, the Industrial Technology Division is another pioneer in Midea’s development of B-end business, mainly targeting customers in the automotive and semiconductor industries. Among them, the three product lines related to new energy vehicles, drive system, thermal management system, and assisted/autonomous driving system, were fully launched in May last year. In February this year, Midea invested 11 billion yuan to build a strategic base for new energy vehicle parts in Anqing, Anhui.

From traditional electrical appliances, hardware to solution services, the continuously widening service boundaries indicate that the B-end battle of white goods giants is about to enter a new stage.

write at the end

Under the circumstance that the popularity has dropped sharply, the senior management of Kelu Electronics told investors on August 31 that the merger and acquisition plan between the company and Midea Group is still in progress.

Back in May of this year, Midea issued an offer to acquire Kelu Electronics, intending to increase its new energy business and counter Gree, which had invested in Dunan Environment not long ago. At that time, the two major home appliance giants Midea and Gree started a full-scale war, both in terms of main white goods products and sub-line business, and they were tit-for-tat and unwilling to follow.

At that time, the hot topic in the industry was that if Kelu Electronics could be successfully won, the number of Midea A-share listed companies would increase to 6, and no one could stop the limelight.

But the development of the story later, everyone is very clear. After the main white goods business suffered the impact of the downturn in the general environment, especially after the shrinking of the C-end consumer market, the overly large business line and acquisition territory became a heavy pressure on Midea.

When the time comes to July, Meizhi Optoelectronics, which originally planned to spin off and list from Midea, terminated its GEM IPO application. Midea, who had been racing all the way in the capital market, finally slowed down.

In an unfavorable market environment, a company’s routine operation is to accumulate grains, delay the kingship, and reserve ammunition to meet various challenges that may arise in the future. Sometimes it’s not necessarily a bad thing to stop and think about it and re-plan your route. For Midea, whose hegemony status is still stable, it should be more calm to slow down and reorganize resources.

(Disclaimer: This article only represents the author’s point of view and does not represent the position of Sina.com.)

This article is reproduced from: http://finance.sina.com.cn/tech/csj/2022-09-01/doc-imizmscv8698573.shtml

This site is for inclusion only, and the copyright belongs to the original author.