It is hoped that after this large-scale lifting of the ban, the market can test which types of REITs are gold and which are sand, and provide a more valuable reference for our future investment in REITs.

1. The situation of this time when REITs are lifted

Briefly talk about why there is a lifting of the ban, because when REITs are released, all strategic investors are required to lock their shares for a period of time and cannot sell them. The advantage is that they can get more REITs fund shares at the issue price. If If the price of the fund after listing exceeds the issue price, then this business can be done. The risk is that the price will fall below the issue price when the lifting period ends (disregarding dividends). The sales restriction is divided into several levels. Among them, the original owner of the project requires not less than 5 years, the related parties of the original owner should not be less than 3 years, and the others should not be less than 1 year. Note that “no less than” is used here, and some original rights and interests have a voluntary lock-up period of up to 315 months (26.25 years) , basically not planning to sell.

We checked the types of institutional holders of the 9 publicly offered REITs that will be lifted this time, including securities companies and securities company asset management, local state-owned assets, private equity institutions, insurance funds, banks and bank wealth management, etc. The number of institutional holders lifted is 6-17, and the lifted shares of these institutional holders are not particularly concentrated.

The time for listing and trading after the lifting of the ban is June 21, 2022. According to the closing price on June 14, the total lifted market value of the nine publicly offered REITs is 11.482 billion yuan.

2. How big is the impact of the lifting of the ban on the secondary market price of REITs?

First of all, it is necessary to clarify an important concept, secondary market circulation share , which refers to the share that can be freely traded in the exchange according to real-time prices. It naturally does not include fund shares that have not been lifted and OTC subscriptions that have not been transferred to the market. share.

Some of the REITs fund shares lifted this time are off-market shares. If this part is not transferred to the market, it cannot be traded in the secondary market. However, since the proportion is not large, we tentatively believe that all the shares lifted this time will be transferred to the exchange. In this case, to measure the impact of lifting the ban on secondary market prices, the factors to be considered include:

①The proportion of the lifting share to the circulation share before the lifting of the ban, the larger the ratio , the greater the impact may be;

②The profit and loss ratio of the unlocked shares, the larger the profit ratio , the greater the impulse to sell to take profit, and the greater the impact on the secondary market price;

③ The size of the market value of the lifting of the ban , due to scarcity reasons, the larger the market value of the lifting of the ban, the greater the impact, if the market value of the lifting of the ban is small, even if the above two points are relatively large, it may not form a selling pressure;

The above three points are what the author can think of at this moment, and readers and friends are welcome to add them.

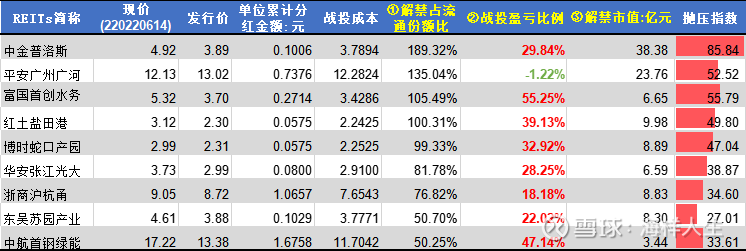

Below is the data collected by the author. It should be pointed out that the data of circulating shares is not available on many stock/fund software , and the author only found it on the financial terminal software; in addition, to calculate the profit and loss data of the unlocked shares, the cumulative dividend amount since its establishment must be considered, which must be subtracted from the issue price. Cumulative dividends are the real cost. Among the 9 publicly offered REITs, only Ping An Guangzhou Guanghe’s strategic investment lost money.

In the above table, we have calculated the three influencing factors mentioned above, and assigned the same weight to these three indicators, and calculated a ” selling pressure index “ . The selling pressure of Soochow Suyuan Industry REIT (SH508027) is the smallest. This “selling pressure index” is an indicator fabricated by the author, which is likely to be far from Dapu and is only for entertainment use.

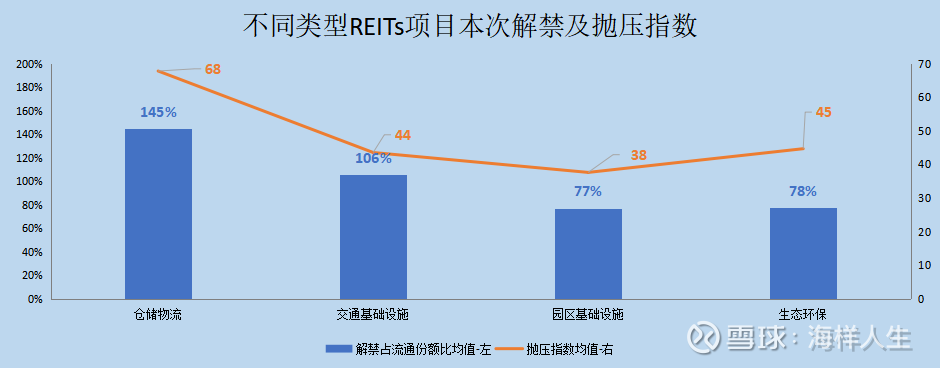

We divide it by project type and find that the average lifting of the ban on warehousing and logistics is the highest, and the park infrastructure is the smallest, and the corresponding average selling pressure index basically shows a similar trend.

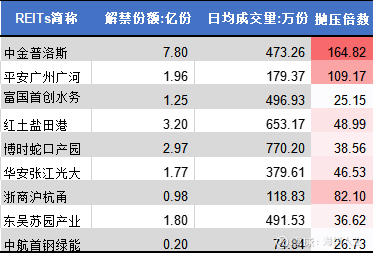

Here, the author thinks that the daily trading volume may be an important factor affecting the price performance during the sell-off. Imagine that a REITs only has a daily trading volume of 10 million copies, and this time the ban is lifted to 800 million copies. If the 800 million copies are to be Selling, just to sell these 800 million copies, it will take 160 trading days, which is likely to form a stampede.

Therefore, we counted the average daily trading volume of these 9 REITs this year, and calculated the multiple of the lifting share and the daily average trading volume. I would like to call it the “potential selling pressure multiple” (referred to as the selling pressure multiple), and The table above can be referenced together. Zhongjin Plus tops the list with 164 times. If the 780 million copies lifted are sold, it will take a long time to digest. The green energy of AVIC Shougang is only 26 times, which means the least pressure.

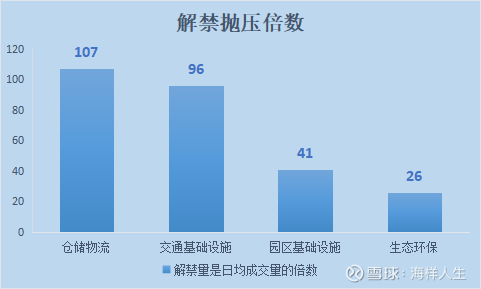

We divide it again by type, and we can see that the average lifting and selling pressure multiple of warehousing and logistics is still the highest, and the ecological environment is the least. What is a quality project? High-quality projects are assets that original stakeholders are reluctant to sell . These shareholders will choose to hold a high proportion of shares at the issuance stage and are willing to endure a long lock-up period. We will wait and see after the ban is lifted.

3. Other information worthy of attention in this public offering REITs lifting event

First of all, the current information disclosure of publicly offered REITs is based on closed-end funds, and many regulatory standards are also based on closed-end funds, which is different from stocks. For example, after the stock sale restriction period expires, it is necessary for the shareholders who have satisfied the lifting of the sale restriction to take the initiative to apply for it, and after confirming that the tax has been paid, etc., can it be circulated, while public REITs are relatively simple . share . In addition, there are strict regulations on the reduction of major shareholders of stocks, while strategic investors of publicly offered REITs have no special regulations on reduction of their holdings once the ban is lifted;

Secondly, the lifting of the ban may have a greater impact on expressway REITs, because such REITs projects are not scarce. The fourth batch of REITs projects that have been identified so far are also expressways, which makes expressway projects that are not scarce enough even more mediocre, and the premium rate will inevitably go up for a long time.

In the end, don’t overestimate the “rationality” of institutions . In the face of the temptation to exceed expectations, the determination of institutions to sell first is likely to be more determined than we imagined.

$Fuguo Capital Water REIT(SH508006)$ #reitsnews# #CRCC Chongqing Yusui Expressway REITs#

Data source: wind, deadline 2022.6.14

@snowball creator center @snowball fund

This topic has 10 discussions in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/8529783827/222790184

This site is for inclusion only, and the copyright belongs to the original author.