It’s time to overturn our inherent cognition. Everyone can feel the difficulty of investing in 2022, but the “poor baby” I didn’t expect is not Manager Cai and Goddess Ge, nor is it Baijiu and Zhonggai. Let me first give you a set of data (as of October 27, the yield of each benchmark fund this year):

Chip Active Class Representative >> Lion Growth Mix: -38.43%;

Pharmaceutical active class representative >> CEIBS Healthcare: -25.89%;

Liquor Active Class Representative >> E Fund Blue Chip Selection: -34.99%;

Representative of Hong Kong Stock Technology Class >> Celestica Hengsheng Technology: -39.39%.

If you think this is already exciting, then look at the picture below should be more exciting.

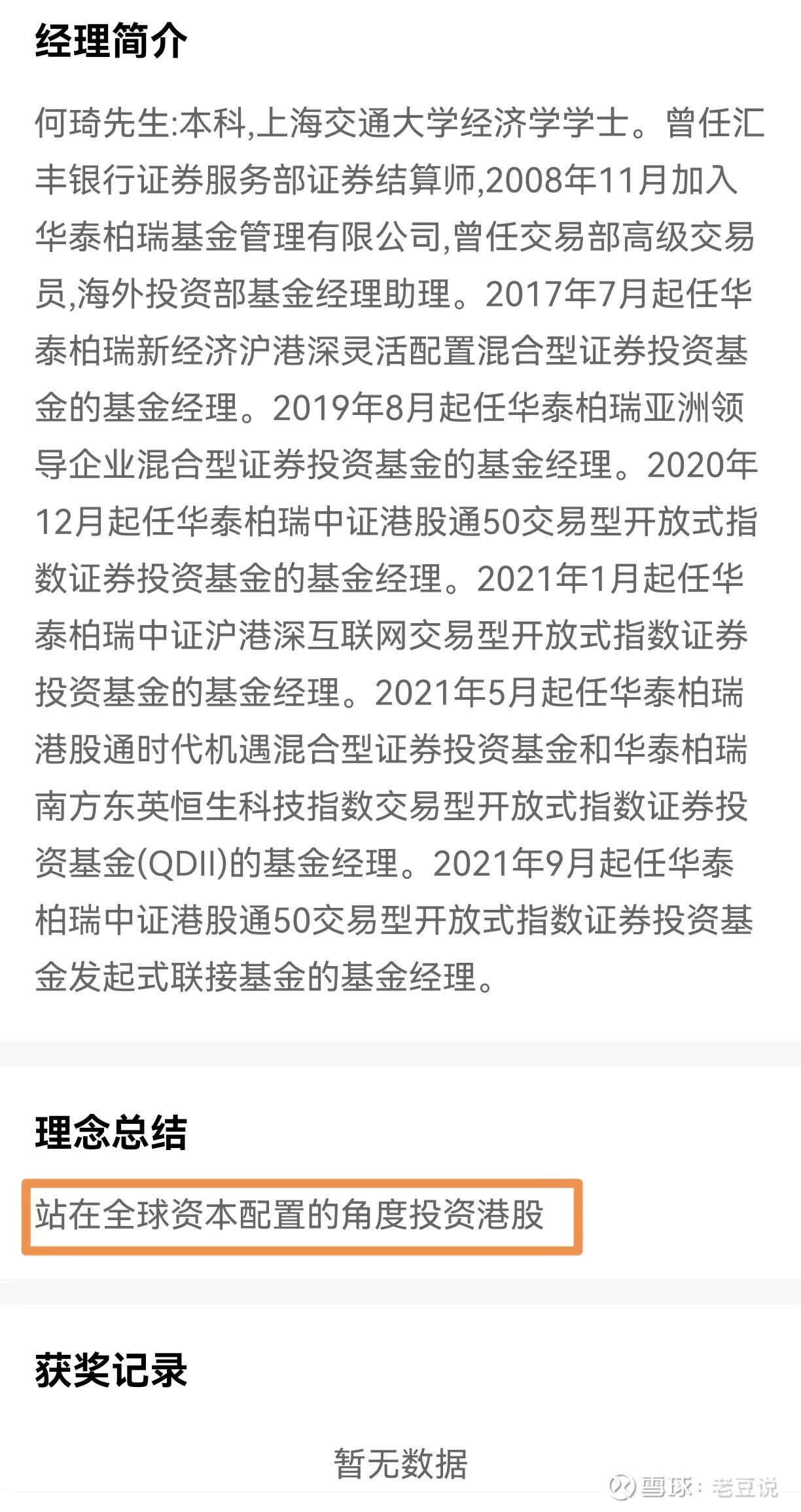

Even more exciting, there are both index funds and active funds in this table, and these 9 products are managed by the same fund manager. The three marked green in the chart are all “representatives of the four major classes in seconds” (and also crushed the index fund he manages himself), and all of them have the “potential” to cut their net worth by half this year. The “investment in Hong Kong stocks from the perspective of global capital allocation” mentioned in the title of this article is the “idea summary” on the profile page of the fund manager (see the figure below), and this investment philosophy is destined to be doomed to the product performance in 2022.

This fund manager seems to manage tens of billions of dollars, but in fact, it is mainly the scale of two ETFs, Hang Seng Technology and Hong Kong Stock Connect 50, and the rest are very small. In the latest third quarterly report, several have liquidation risks. How did this fund manager enter everyone’s field of vision? It has to start with a third quarterly report (interested friends may also go to the official website to find the original document).

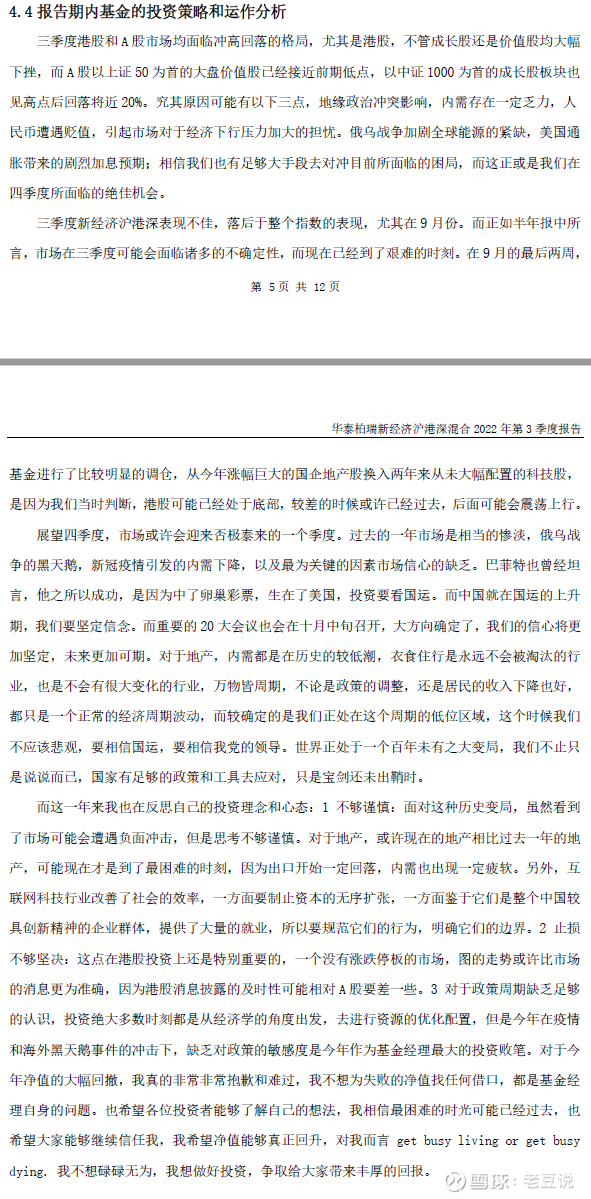

In fact, in terms of the sincerity of the quarterly report, it is already enough (of course, his second quarterly report is also so sincere), He Qi admitted that he is not cautious enough, obsessed with real estate, indecisive about stop loss, lack of cycle awareness, lack of ZC sensitivity, and finally almost begging “I don’t want to be mediocre, I want to invest well and strive to bring good returns to everyone.”

(At this time, the BGM sounded, and Mitsui Shou, who was kneeling on the ground, shed tears of remorse, and said: “Coach, I want to play basketball woo woo woo…”) If I have to say something that is not so sad, it is these few The scale of active funds that are almost cut in half is very small, and there should be not many Christian Democrats who have been injured outside of internal holdings.

Finally, I would like to say: it is estimated that He Qi himself did not expect to be “familiar” by everyone in this form, and I wonder if he will be so “sincere” when he writes the annual report next time? I’m afraid that other fund managers will become more “prudent” when they write reports later, after all, the days of investing in 2022 are really not easy…

#Fund’s three quarterly reports are released one after another, what are the highlights? # $ Shanghai Index (SH000001)$ $ Kweichow Moutai (SH600519)$ $ Tencent Holdings (00700)$

@Today’s topic @snowball fund @snowball creator center

There are 48 discussions on this topic in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/5188297436/233846816

This site is for inclusion only, and the copyright belongs to the original author.