Another extremely important article by Zoltan Polzsar, which provides a detailed analysis of the disintegrating nature of the existing world order and the strategies the United States and the West will adopt to deal with it. This is part of Zoltan Polzsar’s work on the continuous construction of the Bretton Woods three systems, which has enormous influence on Wall Street and even in global financial markets.

This article is an unauthorized translation, and readers should refer to the original text.

Zoltan Polzsar, Credit Suisse, August 24, 2022

War means industry.

There is no war in the criss-crossing supply chains of a globalized world. Many critical products are produced and manufactured in one corner of the world, and only secure and open supply chain channels can ensure that these products are shipped from the factories there. Such global supply chains are only effective in times of peace. And in the event of war and conflict—whether thermal or “economic”—those supply chains fail immediately. However, this globalized supply chain is the cornerstone of the so-called low-inflation, high-growth world we have experienced over the years. This system has three pillars:

- The entry of a large number of cheap immigrant labor into the United States depresses nominal wages in the United States, making wage growth in the United States stagnant;

- In a state of stagnant nominal wages, cheap Chinese-made goods increase the purchasing power of real wages;

- Cheap Russian energy feeds Germany and the wider European industrial system, maintaining European competitiveness and living standards.

Two huge geostrategic and geoeconomic blocks are implicit in this “trinity” system: Neil Ferguson calls the former “Chimerica” (Central America). I would like to call the latter “Eurussia” (Russian Continental).

The two geopolitical/economic blocks are a “match made in heaven”: the EU pays euros for cheap Russian energy and the US pays dollars for cheap Chinese goods. Russia and China are “duty” to repay their trade surplus to the G7 (buying financial assets of G7 countries). The parties are entangled financially and commercially. As the old wisdom says, if all people benefit from trade, there is no point in fighting. But as with any marriage, arrangements that benefit all can only exist if there is harmony and stability, and this harmony needs to be built on the basis of “trust”, and occasional disagreements can only happen with trust. A peaceful and proper settlement. And once that trust is lost, all the prosperity and stability we have experienced in the past may be lost along with it. This is exactly what Dale Copeland attempts to argue in his book Economic Interdependence and War:

Looking back at the past 200 years, including the Napoleonic Wars and the Crimean War, the authors argue that “when great powers have positive expectations about the future trading environment, they want to secure their core economic interests by maintaining peace, thereby Strengthen their own long-term economic strength. And once those expectations turn negative, these great powers may fear losing raw materials or markets, incentivizing them to trigger a crisis to protect their commercial interests.” This “trade expectations theory” is very valuable for understanding the root causes of the conflict between the United States and China and Russia, and even understanding the nature of inflation faced by the Western world.

In short, the stabilizing effect of trade only works when trust exists. For China and the United States, this trust has disappeared, and the same is happening between Russia and Europe. Instead, it is Russia’s proximity to China: as the “king” and “queen” of the BRICS system, the “summer in heaven” on the huge chessboard of Eurasia, this powerful new alliance is emerging from “China and the United States.” ” and the “Russian Continental” two major systems were disintegrating and reborn.

How is trust lost?

An “easy-to-understand” story goes like this: China made a fortune by selling cheap goods, and then wanted to build a 5G communication network around the world, using the most advanced lithography machines to produce the highest-end chips. At this time, the United States said: “No way!” From then on, “China and the United States” fell into a crisis of confidence.

And a short version of the story about Russia and Europe goes like this: Russia made a fortune selling cheap gas to Europe, while Germany became very rich selling expensive goods made with cheap gas to Europe and the world. Business is so good that Russia and Germany have even prepared a ceremony to celebrate the opening of the Nord Stream 2 pipeline. But suddenly one day, the conflict between Russia and Ukraine broke out. Germany believed that this behavior exceeded Germany’s bottom line, the celebration was cancelled, and the two sides broke up.

America’s wealth comes from quantitative easing (money printing). But QE is based on low inflation from cheap energy in Russia and cheap goods in China. The United States, at the top of the food chain in the global economic system, certainly does not want the end of the era of low inflation, which would mean the end of the easy money-printing model. But if the cooperation between China and the United States (China-US) and the cooperation between Russia and Europe (Russia-Europe) go bankrupt respectively, low inflation will come to an end.

The special relationship between China and Russia that is taking shape is a powerful union: it is a marriage of commodities and industrial products, uniting the world’s largest producer of commodities (Russia) and the world’s factory (China), while Geographically, it can cover and control the entire Eurasian continent.

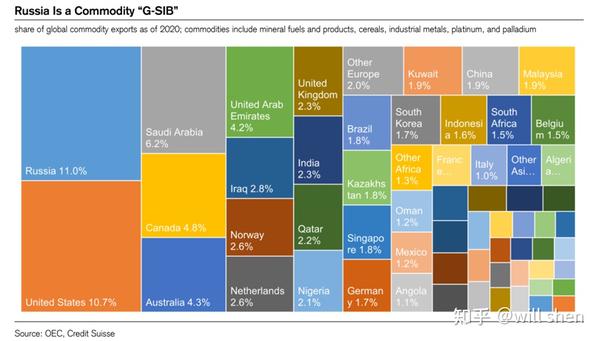

“G-SIB” in the field of commodities, Russia bears the brunt

“G-SIB” in the field of commodities, Russia bears the brunt

The special Sino-Russian relationship is like an economic alliance formed by two spouses who have been betrayed (China, which was driven out of Sino-US cooperation, and Russia, who was driven out of Russian-European union), in revenge for their “predecessors”: one of the long-term Lack of raw materials, another lack of key industrial goods such as chips due to sanctions. And two “exes” from previous marriages come together to form a new alliance, but this alliance is different from the interdependence and complementarity that existed in the previous alliance, in which one (Europe) is extremely dependent on the other (United States) for economic security.

In wars, like the economic wars currently underway, the key battle is control: control of technology, control of commodities, control of production capacity, and control of key geographic nodes—including the Taiwan Strait, the Strait of Hormuz, chokepoints like the Bosphorus.

War is also about alliances. In the current complex conflict game between China, the United States and Russia, the so-called friend is defined as “the enemy of the enemy is a friend”. A number of important geopolitical events reveal the gradual formation of this alliance: Russia conducts naval exercises with China and Iran in the Strait of Hormuz; Iran coordinates Russian-Turkish arrangements for grain shipments in the Black Sea and the Bosphorus – first Ukrainian grain shipped through the Bosphorus arrived at Tartus, a port in Syria, the Russian protectorate; Turkey and Russia agreed to settle bilateral trade in rubles, and so on.

In this complex web of geostrategic hotspots around Eurasia, the noose on the “friend of the enemy” is tightening: Ukraine is under attack, Taiwan is under a week-long blockade, South Korea under pressure from China proposes “three nos” “Policy – The essence of this policy is to gradually end all forms of military cooperation with the United States. The evolution of the Korean peninsula is worth watching: the latest developments show that North Korea is actively deepening ties with Russia and China, and adopting a “brink of war” strategy on the Korean peninsula, which makes South Korean President Yoon Hee-won extremely cautious, even preferring to go to the theater. The show also declined to meet with visiting U.S. House Speaker Nancy Pelosi. I call this Korean strategy (Korean-style) “strategic ambiguity.”

The so-called “our currency, your problem” in the United States that people talked about in the past is now becoming, “our commodities, your problem”, or “the chip in our backyard, your problem”, or “Our strait, your problem” (the US threat to impose secondary sanctions on Turkey over its economic ties with Russia should be understood as NATO’s retaliation for its passage through the Bosphorus by Turkey’s restrictions).

Taking a step back, from a larger geographic perspective, we see a fierce competition and game taking place across Eurasia. The so-called “BRICS alliance” is not the key here, the real player here is one formed by Turkey, Russia, Iran, China and North Korea coming close to each other A coalition across Eurasia that I call “TRICKs” – a coalition of all countries that are directly sanctioned or threatened by the United States. This “alliance of the sanctioned” is asking all of America’s friends to make pragmatic choices. For example, India has significantly increased its energy imports from Russia and participated in Russia’s Vostok-2022 military exercise despite intense pressure from the United States; the lack of a response by the United States to China’s military exercises and blockade in the Taiwan Strait will also make South Korea reassessed their geopolitical reality. As Pippa Malmgren recently pointed out: Washington is beginning to doubt South Korea’s loyalty, arguing that South Korea may have chosen to work with China over the United States. Seoul’s so-called “strategic ambiguity” is in fact an option, meaning South Korea will not fight China as the West’s border in Northeast Asia. If inter-Korean reconciliation is achieved (as President Moon Jae-in has attempted over the past few years with the support of China), the 30,000 U.S. troops stationed in South Korea will have no reason to exist and will have to choose to leave.

Many people think that the “conversion of Paul” (the biblical story of the apostle Paul’s conversion to Jesus in Damascus) is just a biblical story, not a geopolitical reality. This belief is completely false, and those who hold it need to re-read history, or, more simply, grow up in Hungary. On June 16, 1989, when I was 11 years old, a young Viktor Orban vehemently demanded the withdrawal of Soviet troops from Hungary. This happened even months before the fall of the Berlin Wall on November 9 of that year. We link this event to the birth of modern globalization, to the economic structure of the “low inflation growth” of the past 30 years.

Could South Korea’s policy of “strategic ambiguity” be a precursor to an “Orban moment” in South Korea’s foreign policy? Can South Korea and his people feel the extreme danger their country is in and demand the withdrawal of U.S. troops from the Korean peninsula?

History doesn’t repeat itself, but it rhymes. The foreign policy of Orban back then is completely different from Orban’s foreign policy today. Similarly, the chips produced in South Korea today cannot be compared with the chips produced in South Korea in the future. Therefore, for the United States, the risk of chips is not limited to Taiwan, and huge risks also exist for chips produced in South Korea. The geopolitical events taking place today are so far-reaching and significant that they are compared to some of the geostrategic events that occurred during the Cold War in which the United States participated and supported, such as the 1956 U.S. support of the anti-Soviet movement in Hungary, and the The Suez Crisis, the US-Soviet support for Egypt against Britain, France and Israel, these events are like a child’s game in geopolitics compared to what will happen today and in the future.

But the experience of 1956 can teach today’s market a meaningful lesson: a key component of warfare is “fighting,” and even the greatest powers often choose to engage directly in some “battles” to avoid getting caught up in others. Some. Simultaneous “battles” on multiple fronts (Ukraine, Taiwan Strait, South Korea) mean that each battlefield has a choice of importance and order. In 1956, oil was more important than Hungary, so U.S. resources ended up in Egypt, and the anti-Soviet movement in Hungary ended in vain. For me, the immediate result is that I was born and raised on the east side of the Iron Curtain, surreptitiously watching good movies about West of the Iron Curtain and imagining a different life. Today, I live in Manhattan, New York, the center of the Western world, patiently watching events in the East, wondering whether the United States is still capable enough to maintain the current world order, or on multiple fronts as it did in 1956 Options include NATO’s borders in Europe, the supply of chips, or control over oil.

Or worse, a total checkmate by TRICKs on the big Eurasian chessboard?

I can’t predict exactly how things will unfold, and no one can, not even the Pentagon. That’s why we think expectations of a rapid pullback in inflation are too naive and optimistic. The logic here is that PAX AMERICANA promotes globalization, and globalization ensures low inflation (in the western world). So the fact that TRICKs countries are no longer cooperating and even trying to weaken the system means that inflation is a huge long-term risk.

To understand the logic and path of inflation from this perspective, we need to read more history, review those historical events, and think about trust, trade, and Dale Copeland’s theory of trade expectations: if globalization is driven by “mutual trust,” This globalization in turn promotes the “Great Moderation” (low inflation), then we tend to think that the creation and growth of mistrust will lead to deglobalization, which ultimately leads to the Great Inflation.

What are the economic consequences of distrust?

In today’s article, we will describe our vision for this great transformation process, from post-Cold War globalization to the establishment of a new order. Our view is that we need to form a large “L”-shaped recession to suppress inflation, and we must promote a negative wealth effect to suppress consumer demand so that the consumption side can match the new reality of the supply side. In our view, inflation (in the US) has indeed moderated, but it remains well above target. The US-China separation and the Russia-EU split will have huge costs, including the fact that the Fed will remain hawkish and keep interest rates high, because as soon as easing money leads to increased demand, the constrained supply will immediately push inflation back up. What is driving the economy from an L-shaped recession to an “L/”-shaped re-growth? We can’t count on consumption to generate this “/” upward trend, because our “predecessors”, China and Russia, have left us, the capacity provided for us will disappear, and we will have to produce everything we need ourselves . This new growth driver will come from investment, investment in production and capacity, and the government will help.

Three “awakening” moments

First of all, the Ukrainian front is showing that in a “war of attrition”, ammunition stocks are being depleted much faster than the current capacity of our war industry. How can we fight hot battles on multiple fronts in this situation? What is consumed here is not high-tech weapons that require high-precision chips to manufacture, but the most basic artillery ammunition. A recent article in the Financial Times analyzed,

“The fascination with high-tech conditions and lean manufacturing principles completely ignores the importance of maintaining stockpiles of basic equipment such as artillery shells. For example, the 155 million shells that can be produced a year at full capacity in the United States are placed in Ukraine. On the battlefield, this is only enough to last for two weeks, which marks the “return of industrial warfare.” The article further states: “…cheap ammunition that can be used on a large scale is essential. The West needs to be more self-disciplined instead of always pursuing refinement. The West needs to understand how to maintain a dull and tedious front while being refined. “

Second, even sophisticated gear isn’t quickly produced:

“In May, when Washington ordered 1,300 Stinger air defense missiles to replace the U.S. stockpile of missiles sent to Ukraine, the Raytheon CEO responded: ‘We need some time…'”. It’s not just a matter of replacement equipment: The United States has had to significantly delay orders to Taiwan, and Saudi Arabia has faced severe delays in order to get enough equipment into Ukraine.

Meanwhile, in a recent earnings call, ASML CEO Peter Wennick noted:

“Last week I met with an executive from a large industrial company. He told me that the conglomerate was buying washing machines and taking the chips out of them to fit into their large industrial modular products.”

Third, news from China’s military exercises around Taiwan tells the world that chips are only meaningful when they can be shipped out of factories. These products and capacities are completely ineffective once the blockade blocks logistics. When this nascent multipolar world is disrupting global supply chains, how can the United States maintain the fate of an economic system it has built on low inflation and money printing? How can enough missile chips be obtained to defend America’s global interests and world order?

That’s not to say the East’s rivals are having an easy time. Russia has his military problems, and sanctions on Russia limit his ability to access high-end chips and Western technology. But we all know that “there is no upper limit to the relationship between Russia and China”, and China also makes a lot of chips. It’s like a soft drink: you can choose to drink Coca-Cola or Pepsi. Likewise, whether Russia uses TSMC (TSMC) chips or SMIC (SMIC) chips, Russian missiles can fly in a perfect arc. Just as the pipeline and flow of energy is being reshaped by new wars and geographies, so too will the flow of chips. Russian pipeline gas to Europe is gradually being replaced by U.S. liquefied natural gas, while chips from Japan, South Korea and Taiwan flowing to Russia will also be replaced by chips produced in mainland China.

Life has to go on, but tail risks remain. As TRICKs move more and more across the Eurasian chessboard, most of the tail risk points to the Western world, particularly the impact on inflation in the West. China’s strong control of the Taiwan Strait and South Korea’s policy of “strategic ambiguity” means that “the chip in our backyard, your problem” is a clear, urgent and present risk to the United States and the wider West.

To be precise, the three “awakening” moments discussed above mean that global supply chains, whether military or civilian, are facing a Minsky moment. In the original connotation of the concept, the Minsky moment meant the implosion of the shadow banking system, marking the beginning of the financial crisis. Today we are witnessing the implosion of supply chains in a globalized world order with a globalized production system that lacks inventory and effective protection. Western businesses design and manage in their own countries, outsourcing procurement, production and shipping logistics abroad. All the key links here, including commodities, factories and shipping fleets, are under the control and dominance of China and Russia, which are in conflict with the Western world.

The inventory in the supply chain is the liquidity of the bank. In 2007-2008, large banks only prepared short-term “immediate” liquidity: banks’ liquidity was dominated by the immediate availability of funds in financial markets. This allows market participants to sell various types of assets into the deep market at any time without worrying about compromising the fair value of the assets. So banks are not actively preparing large cash reserves at the central bank because these reserves are considered inefficient and cannot create maximum value for shareholders. (And when the market eventually failed and there was a shortage of liquidity, everyone saw how vulnerable those big financial institutions were). Likewise, today’s large corporations and corporations operate “just in time” supply chains. Businesses think they can always buy the products and parts they need at a reasonable price at any point in time without worrying about premiums. Cold facts tell people that this assumption is incorrect. The U.S. military will have to “wait a while” to get their ordered missile systems, while Taiwan and Saudi Arabia won’t get their orders until the war in Ukraine is over. Further, if your washing machine is broken and you want to replace it, you may have to wait a while, because large defense contractors need to disassemble washing machine parts to make missiles.

We disassemble “here” to make “there” products. Do you remember the Minsky three entities? Hedging entities can make their payments out of their income. Speculative entities have to borrow money to pay. Ponzi entities can only make payments after selling the assets they hold. Among the three, the Pond’s unit is most affected by interest rate fluctuations. And just like our example in the chip industry, according to Minsky’s Law, the supply chain of our military industrial system is at best a “speculative unit”, and as geopolitical tensions and conflicts escalate, these supply chains will even soon be Downgraded to a “Ponzi” supply chain. The same framework can be applied to European energy markets: when Russia’s gas supplies are cut, Germany is immediately faced with a break-even situation, and the government will have to ask citizens to conserve energy in order to leave more room for industrial output to consume.

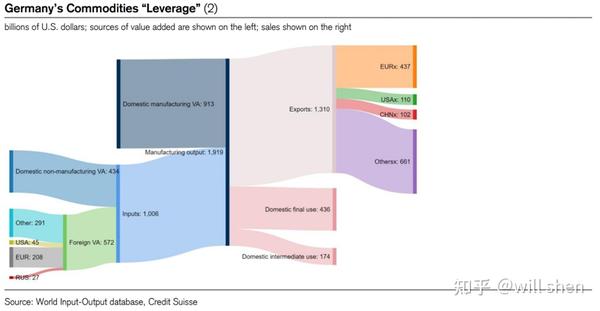

Minsky moments are caused by excessive financial leverage. Applied in the context of supply chains, the leverage here is excessive operating leverage: Germany, for example, whose $2 trillion in industrial added value depends on $20 billion in natural gas imports from Russia—from this perspective To understand, Germany’s leverage on Russian gas is 100 times, far exceeding the leverage ratio of Lehman Brothers.

Leverage of German production against Russian energy

Leverage of German production against Russian energy

The concept of operating leverage also applies to the military: for example, chips produced in Taiwan are used in missiles produced in the United States, and once Taiwan is blocked, these missile parts are likely to not reach the US missile factories, From this point of view, the United States simply cannot cope with a war on the east and west fronts.

The ability of “American rule of the world” to maintain the global supply chain is like the capital of a bank. During the 2008 financial crisis, large banks were caught in the crisis without sufficient capital to deal with systemic liquidity crunch. Because they were “too big to fail,” the U.S. government had to resort to massive bailouts, the cost of which was Basel III.

Investors today tend to think of “globalization” as a “too big to fail” thing as well. But “globalization” is not a bank that can be bailed out, and the system needs a “world hegemony” to keep it in order. The risk to this system is that someone will challenge this world hegemony – like China and Russia today. In order to maintain today’s world order and its associated trade arrangements and global supply chain networks, these challenges must be met swiftly and decisively, with forceful means to suppress them, as General Powell (later the U.S. Secretary of State) during Operation Desert Storm. However, Ukraine and Taiwan are not the Kuwait of the year, and Russia and China are not comparable to the Iraq of the year. Top Gun 2 and Top Gun 1 are two completely different movies…

Imagine what Tim Geithner (the US Treasury secretary under Obama) said was needed to deal with a financial crisis or to attack short-sellers in the US banking system. In today’s context, Russia and China are basically “short sellers” challenging the US-led world order. To quote Geithner back in the day, we need to take “overwhelming thunder—not piecemeal, similar to what we did during the Vietnam War; if we don’t stop (to the banks) With a run, the market won’t build confidence in our commitments. So we’re going to be prepared to put ‘an enormous amount of money’ that makes us determined to look bigger than the total market debt.” General Powell’s prowess in Operation Desert Storm, and Treasury Secretary Geithner’s determination to save the U.S. banking system, lead me to associate these actions with the U.S. Commerce Secretary Gina Raymond today. Compare the stances that many countries have taken to address the challenges of global supply chains.

Rather than showing strength and determination, what the US Department of Commerce shows is the fragility of the United States. As Secretary Raimondo said recently, the United States “buys nearly 70 percent of advanced chips from Taiwan. This includes a large number of chips used in military industrial production. And there are about 250 of these chips in the Javelin missile system. You Want to continue getting these critical chips from factories in Taiwan? There is no security in a supply chain like this. We need Congress to pass the chip bill as quickly as possible so that we can re-produce these chips on U.S. soil.” These remarks Means Secretary Raimondo’s Paulson moment: when he was in Congress begging for a quick TARP bailout to support America’s banking system.

War allows you to truly understand the boundaries of your abilities. You need to understand the boundaries of your production capabilities, the boundaries of your combat capabilities, which is exactly what Simon Kuznets was commissioned by the Commerce Department in 1942 to develop U.S. national data to assess the true capabilities of the United States in World War II. And today, Congress would not have passed the $52 billion chip bill in such a short period of time without detailed data and intelligence from the Commerce Department under Secretary Raimondo. But the hard work lies ahead. It will take years to build a wafer fab, and we can only regain our “semiconductor sovereignty” when these capacities are in good working order.

But the problem is that we need to show our “overwhelming power” to the “short sellers” right now, today, right now, now, not what tomorrow, months and years later, in the future. It is now that a powerful force is showing “overwhelming power” in the Taiwan Strait, and that show is not the United States.

This is exactly why the US is trying to “turn back the clock” with technology embargoes and sanctions. As described in the recent film “Creed”, “inverted time” can be used to shape the future: the United States is trying to slow China’s technological progress through technical sanctions again and again, thereby reshaping the future balance of power. Slowing down China’s development will buy time, which will be used to build homegrown wafer factories that will be able to produce chips inside the US for missiles to defend US hegemony.

So far, the list of U.S. tech sanctions on China is getting longer. Recent developments include a U.S. attempt to ban ASML from selling DUV lithography machines, as well as other chip-making processes and software products, to China in an effort to curb the semiconductor ambitions of China and Chinese companies such as SMIC. Further, the United States is also considering restricting the sale of chip manufacturing equipment to Chinese memory chip manufacturers. The proposed new restrictions also include “preventing South Korea’s Samsung Electronics and SK Hynix from shipping new technological tools to their factories in China, thereby preventing them from upgrading to large-scale factories that can serve customers around the world.”

Will these new pressures targeting South Korean chipmakers force Seoul to consider their policy of “strategic ambiguity” further? I can’t answer such a question. However, make sure your inflation forecast formula has an extra dummy variable.

I can understand why the U.S. has adopted a strategy of “turning back the clock.” But people have to understand that we can’t win by just slowing down our opponents. We also need massive construction, which is why we need American industrial policy:

As an investor, you care about the inflationary consequences of a China-Russia challenge to U.S. hegemony. And once inflation soars, policy rates will rise with it, and failure to do so creates a problem of financial repression. Regardless, if your company is focused on bond investing or fixed income, you’ll be keeping a close eye on these metrics and movements. This market will be the so-called “rental” and “euthanasia” market. To ensure that the West wins this economic war, overcoming so-called “our commodities, your problems”, or “chips in our backyard, your problems”, or “our straits, your problems” — and so on and so forth Dilemma, the West needs to invest trillions of dollars from “yesterday” in four types of projects:

- Rearming (to maintain the existing order)

- Industry returns (to avoid being blocked)

- Build inventories and invest in commodity production

- Reconfiguring the energy and power network

Similar to Basel III as the label of the 2008 financial crisis, the four major projects listed above are the label of the ongoing globalization crisis. The items on the list are self-explanatory, and we read similar related stories in the news every day, such as:

- With regard to rearmament, Germany plans to spend 100 billion euros for rearmament; the West plans to invest 750 billion US dollars to rebuild Ukraine; the G7 goal is to raise 600 billion US dollars against China’s Belt and Road Initiative – a core of the Eurasian chess game is about the Belt and Road All the way and the competition of the items it includes.

- Regarding manufacturing reshoring, Secretary Raimondo focused on military chips and three new fabs funded by the $52 billion Chip Act. Europe is also busy investing in wafer capacity in anticipation of “industrial sovereignty.” Relying on the production capacity of so-called “friendly countries” is also unreliable. Because products from friendly countries also have to be shipped through the strait, which may be blocked.

- With regard to restocking, the situation of the EU gas crisis and energy shortage need not be repeated. The EU desperately needs to re-establish commodity supplies to maintain industrial dynamism and winter heating. The US needs to rebuild the Strategic Petroleum Reserve as well, because our SPR will be “depleted” by November this year. India has directed all its industrialized provinces to build coal stocks sufficient to cover three years of residential and industrial needs. Europe and China are suffering from historic droughts, and Ukraine has lost most of this year’s wheat harvest. The crisis of energy and food is imminent, and the strategic reserves of global commodities will skyrocket like the foreign exchange reserves after the Asian economic crisis in 1997. This involves not only food and energy, but also some industrial products.

- With regard to rebuilding energy and power grids, even after the outbreak of the Russian-Ukrainian war, the U.S. government’s commitment remained unwavering. The energy transition was the only major item on the prewar to-do list, and it was a daunting challenge from the start. As the war begins, the list will grow longer and the challenges will become more difficult.

I believe that the above four themes will be clear targets for industrial policy over the next five years. How much the G7 will spend on these projects is an open question, but given the challenges to the global order, they are likely to be generous. If we’re lucky enough that Western governments can really manage this moment of “strength and determination” by someone like Geithner, or with the attitude Geithner had in dealing with the financial crisis, then for investors, The corresponding investment strategy would be a list of:

- Commodity intensive

- capital intensive

- interest rate insensitive

- East is not investable

Commodity-intensive will mean that inflation will be one of the most vexing problems the Western world faces in implementing the above list. Rearmament, industrial return, restocking and rebuilding of energy networks, these policies all require the consumption of large quantities of commodities, not only for production consumption, but also for large strategic reserves and inventories. This would create a sharp demand shock for the West’s heavily underinvested commodities sector, a hangover from the past decade’s focus on ESG policies. Insufficient investment means supply shortages, while geopolitical factors will lead to resource nationalism, resulting in more shortages and restrictions. Investors can see Russia’s latest stance on its resources and Mexico’s decision to nationalize its lithium mines. There will be a surge in demand and a shortage in supply, with the result that prices could skyrocket. This will likely drive a new commodities supercycle, as we have seen since China joined the WTO in 2001. The last commodity supercycle occurred in the context of a peaceful unipolar hegemonic world order, and the world’s major countries have positive expectations for the future trading environment. Today’s situation is very different.

Capital-intensive means that the government and the private sector will have to borrow long-term to invest. Rearming and restocking are both areas of government policy, while industrial repatriation and energy network construction may involve public-private partnerships. Private companies will have to issue debt and raise equity to build and produce everything from ships to fighter jets, from factories to commodities, to solar panels and wind turbines.

Rate insensitivity means that whether the Fed raises rates to 3.5% or 7%, this to-do list has to be executed, no matter how painful and difficult the process is. Because our industrial sovereignty depends on it.而从另一个角度来看,私募股权(PE)行业对利率极其敏感。一旦执行强力的产业政策,这将排挤私募股权。金融市场是一个数十年为一个周期的系统。私募股权经历了“低通胀”周期和全球化周期,并在金融危机之后享受了十年的低利率和印钞的好日子。对于私募股权投资而言,这个繁荣的周期可以宣告结束了。

东方不可投资,意味着对于某些东方的大国,循环滚动这些国家对G7国家的债券和其他资产的投资是完全不可行的。这不仅仅意味着俄罗斯的外汇储备所遭受的制裁将会警示这些国家的投资者可能的风险,更是因为,滚动数万亿美元的美国国债投资组合意味着你将为作为你的对手的西方世界的重新武装,再库存,产业回归等一系列有损你利益的行为努力提供资金。

我们现在又回到了我们全文开始的地方:戴尔.科普兰的贸易预期理论正是从这里来理解和思考世界的框架。我们,以及这个世界的运行方式,像过去那样继续运行下去是完全没有意义的,无论是从真实的(贸易/生产)的视角,还是从金融(外汇储备)的视角。这正是布雷顿森林III所注定要发生的原因。

这一切都已经在发生了。

来源:知乎www.zhihu.com

作者: will shen

【知乎日报】千万用户的选择,做朋友圈里的新鲜事分享大牛。

点击下载

本文转自: http://zhuanlan.zhihu.com/p/558859527?utm_campaign=rss&utm_medium=rss&utm_source=rss&utm_content=title

This site is for inclusion only, and the copyright belongs to the original author.