Welcome to the WeChat subscription number of “Sina Technology”: techsina

Text/Tao Ting

Source/city boundary (ID: ishijie2018)

Remember that scene in the TV series “Ode to Joy”?

In front of Andy’s desk, a returnee financial executive, there are four large LCD screens. Andy in the play is not only a strong woman in the workplace, she will pay close attention to different market conditions when she returns home to realize the global allocation of personal assets.

In the real world, it is nothing new for Chinese investors to seek overseas asset allocation.

In particular, from March to September 19, 2022, the central parity rate of the RMB against the US dollar was lowered from 6.31 to around 6.94. During this period, some financial professionals found that more people were consulting overseas investments.

Some investors can rationally analyze the valuation and fundamentals of investment targets, and they regard overseas asset allocation as one of the means to inherit personal wealth and diversify risks. However, there are also many investors who invest overseas with a “give it a try” thinking. They are full of longing and yearning for profits and returns.

As everyone knows, roses have thorns. Today, many years later, those Chinese investors who have gone overseas to dig gold have told the world a fact with their real and cruel experiences: overseas gold digs just look beautiful.

A Twice Deferred Dollar Project

Song Nan, who is engaged in overseas asset allocation, is trapped in a US dollar project and is now extremely depressed, “This US dollar fund has to be postponed for another two years, who can bear this?”

In 2018, Song Nan learned about a low-threshold overseas allocation method through a financial platform owned by a well-known domestic e-commerce company: buying channel funds of overseas private equity funds, at least US$100,000, can invest in well-known overseas asset management Company-managed private equity funds. What moved Song Nan’s heart was an opportunistic debt fund called American Commercial Real Estate.

Its issuer, DCR, is an American asset management company. The Chinese name in the promotional materials is Derui Capital. The fixed rate of return (interest distribution) of this fund is 5.25%/year, and the target rate of return (after taxes and fees) is 10%-12%. The investment targets are commercial real estate collateral with continuous and stable cash flow, short-term overdue Preferred Commercial Mortgage.

Derui Capital also claims to be backed by Goldman Sachs, a big bank. This made Song Nan let go of his vigilance. In his view, the idle dollars in overseas accounts need to find a place to preserve and increase their value.

Song Nan has some knowledge of American companies that specialize in acquiring non-performing assets, such as Blackstone. What’s more, the yield of this fund looks so attractive. Coupled with the endorsement of a well-known e-commerce platform, Song Nan finally bought the fund with an amount of 100,000 US dollars (about 700,000 yuan today).

Time soon came to September 2021, the day when this dollar fund expired in three years, but Song Nan was unexpectedly told that the fund would have to be extended for one year. Although there are doubts, because the amount of funds involved is not large, he did not struggle too much. But what Song Nan did not expect was that in September this year, the US dollar project that expired again was notified to extend it once again for two years.

Song Nan, who realized that something was wrong, wanted to find out where the money went. But the matter is far more complicated than he imagined: the agent of Derui Capital in China has only repeatedly emphasized that the projects invested cannot be realized due to the epidemic and must be given a two-year disposal period. Two years, there is a lot of variables.

In desperation, Song Nan hoped that the financial platform would come forward, but the platform became ignorant. The market has learned that there are about 30 or 40 Chinese investors who bought this fund like Song Nan, with a total amount of about 4 million US dollars, of which the larger one is 1 million US dollars.

Did Derui Capital really invest in non-performing asset acquisitions with the money raised from Chinese investors? According to an English report, “they did have a fund in 2017, and this fund was basically invested in their fund in 2015,” Huang Lichong, president of Huisheng International Capital, who is well versed in American finance and law, told the market , may be able to get some back, commercial properties are mortgaged. However, if it is a big sale of debt repayment, then you may not get all of it back, or you can only get back 20%-30%.

The logic of Huang Lichong’s conclusion is that this company is a small and medium-sized company in the United States, and it is not as professional as the promotional materials say. Judging from the CEO’s resume, although he is an accountant, he has not been trained in a professional organization. As we all know, this model of commercial real estate requires a strong professionalism.

This is a high-risk investment field. From the FTSE Nareit All REITs Index (the broadest index of REITs in the United States), in the first two months of 2020 after the start of the epidemic, it turned from a slow rise to a cliff-like decline, and then suddenly V-shaped on March 1, 2020. Reversed and finally rose to December 1, 2021. Entering 2022, the index has fallen in a straight line again. As of September 16, it has fallen by about 22% from the high point in December last year.

More importantly, “Goldman Sachs is a bank that provides mortgage loans to their funds. That is, the fund’s money is used as the principal. If it loses, it will be repaid to Goldman Sachs first, and Goldman Sachs will collect the interest and principal, and then the German It is leveraged to get the fund of Rui Capital back,” Huang Lichong explained.

Although the fund of Derui Capital seems to be more about market risks, in the face of such overseas asset allocation models, financial person Ma Wenping believes that the biggest risk is the flow of funds. He prefers to describe opaque funds as “A child without a mother has many uncontrollable risk points just because he can’t see the flow.”

This is not an isolated case.

Chinese investors are “hunted” by bad currency

“Gresham’s Law” says that people hide money with high real value and spend money with low real value. This is “bad money drives out good money”.

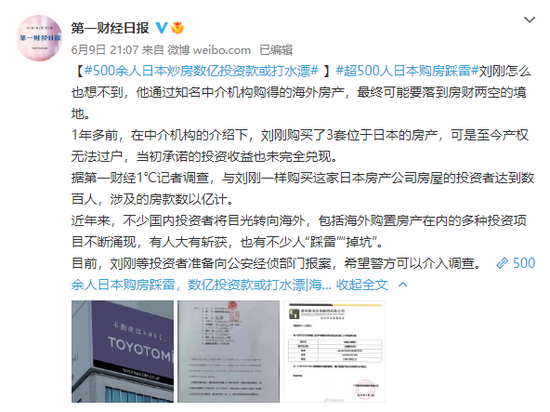

For more than 500 Chinese investors who bought a wealth management product in Japan, they were targeted by “bad money” early on. On the recommendation of an acquaintance, Feng Shaoqi bought a property in Osaka from Toyotomi Corporation in Japan. On the surface, this is to let you buy a house, but in essence, it is a financial product in the name of real estate.

Toyotomi’s business model is “a sea-view room with excellent humanities and appreciation space in xx + high-traffic with a lease package to buy back a prosperous shop + stable profit without loss of wealth management cashback + endorsement by an international real estate agent”. That is, Toyotomi operates the house you buy as a homestay, with an annualized rate of return of 6%. In the third and fourth years, if you are unwilling to rent out, the real estate company can buy back at full price.

Feng Shaoqi did receive rent for a period of time, which made him think it was a serious project. But it didn’t take long before Feng Shaoqi never received the money again. Since the beginning of this year, more and more investors have not received their money. An investor entrusted a lawyer to investigate and found out that the capital chain of Toyotomi Commercial was broken as early as 2020. The company took the money and did not continue to build houses, many of which were unfinished.

(Screenshot of Weibo)

(Screenshot of Weibo)Even so, Toyotomi Commercial also sold off-plan properties to investors through a domestic real estate service agency. It was not until June of this year that the Toyotomi business incident came into the public eye. Song Wei, a Chinese lawyer living in Japan, believes that Toyotomi’s methods have been continuously upgraded over the years, making it difficult for investors to guard against them. As early as early 2019, Song Wei knew about Toyotomi’s investment model.

That year, a friend took an investment report and asked him about Toyotomi’s compliance and risks, “The investment agreement at that time was not so exaggerated, but there was a shadow of ‘fake rent + false return + high premium’ in it. “Song Wei recalled. In September 2021, Song Wei received the first legal service entrustment from Toyotomi Commercial.

“We made some plans for our customers, but we didn’t follow up.” But at that time, the sale and purchase agreement that Song Wei saw had been upgraded from what he saw in 2019. “There is a vague suspicion of serious fraud. Toyotomi is afraid It’s going to explode.” Song Wei came to this judgment based on his analysis of Japan’s economic environment, in addition to doubts about the compliance of the Toyotomi model.

Under the influence of the epidemic, the rental market in Japan is sluggish, and the homestay hotel industry is even more saddened. As a tourist hotspot, real estate companies in Osaka are also frequently reported to close their doors. This means that, assuming that Toyotomi has its own real estate, it is impossible for Toyotomi to maintain this “game” without the impetus of the tourism industry.

In Song Wei’s view, compared with traditional domestic routines, Toyotomi’s model is to put all the play styles into it. Among them, funds going overseas, gaining overseas status, etc., especially hit the weakness of human nature. In February and March of this year, Song Wei found that more and more people consulted, many of whom came through multiple introductions.

However, judging from the information verified by Song Wei, the nature of Toyotomi’s case is worse than that exposed by the media: Toyotomi Commercial has bought and sold buildings that are not under its own name, and whether the contract is valid is still to be discussed; Afterwards, the payee is the Chinese personal account of the legal representative. Are these funds remitted to Toyotomi’s corporate account? Does it violate national foreign exchange control? There are many mysteries to be solved.

Taking the Toyotomi case as a lesson, Song Wei told the city community that if you are not sure about the culture and laws of overseas countries, but use Chinese logic to understand it, you will definitely hit a wall. Be sure to find a really reliable intermediary or partner, sign a substantive agreement with it, and play a joint and several responsibility. Or find a reliable law firm and let it help you do this.

A glimpse of the leopard in the tube can be seen. Not only individuals, but also the overseas investment road of enterprises has been quite difficult. Take a domestic company called Sunflower Capital as an example. As a fund manager, this company issued a fund called “Sunflower-Israel Venture Capital Private Equity” in September 2016. The underlying target of this fund is Israel or high-tech companies with an Israeli background.

This fund expired in March 2020, but due to the impact of many factors such as the epidemic, it has never been able to complete the liquidation work. Although Sunflower Capital tried to give investors an explanation through discounts, introducing companies to subscribe for shares, etc., the market has learned that more than half of 2022 has passed, and the fund has not withdrawn even a single transaction so far.

Senior financial planner He Chen told the market that equity investment is particularly risky in overseas asset allocation. If a company goes public successfully, it can achieve a benign exit. If a business goes out of business, do it at your own risk. Although some funds are an investment method with multiple targets, due to the cross-border investment, this involves complex issues such as geographical restrictions and whether the project due diligence is in place.

Why do Chinese investors encounter so many “bad coins” on their overseas gold nuggets, and how many difficulties do they have to overcome?

Why are there so many difficulties?

In order to understand the reasons why Chinese investors are not smooth in overseas Nuggets, we have to start with the channels and forms of my country’s overseas asset allocation.

The formal channels for domestic and overseas asset allocation are ODI (Overseas Direct Investment), QDII (Qualified Domestic Institutional Investor), QDLP (Qualified Domestic Limited Partner), QDIE (Qualified Domestic Investment Enterprise) and so on. However, due to the tight quota and poor performance, many investors have little interest in this.

Although asset allocation is mainly used to diversify risk, many investors still use it as a means of earning excess profits. Wang Zhaojiang, chairman of Shenzhen Huihe Chuangshi Investment Management Co., Ltd., often asks investors that “the first is that you guarantee me the capital, and the second is how much profit can you help me realize”. In Wang Zhaojiang’s view, this is related to the habit of Chinese people to make short-term money and make quick money.

For a long time, the yield of RMB wealth management products remained high. For example, housing prices in China’s first-tier cities are often rising at double-digit growth rates; trust investment and private debt investment income are also close to or exceeding 10%; bank wealth management and fixed-income investments also have a rate of return of about 4%, exceeding 10%. Similar investments in Europe and the United States. The turning point started in 2016.

This year, as various domestic investment yields declined, institutions engaged in “overseas asset allocation” businesses sprang up like mushrooms after a rain. Among these institutions, of course, there are also financial institutions with qualifications such as QDII, but “good money” is always driven out by “bad money”. Some domestic institutions have joined forces with overseas companies to harvest China’s “leek”. The most important feature of the financial products they promote is “high yield”, but there are various methods.

Qiao Mu, a Chinese living in the United States, told the city community that at first, offline preaching was the main focus. After the epidemic, it will be mainly online. But some big clients or private clients are more likely to find acquaintances offline. For example, if there is a big boss, or an individual demolished, who has a sum of money in his hand, they will conduct targeted marketing.

Hu Feng, a financial practitioner, recognizes the term “targeted marketing”. “These asset management companies will go everywhere to raise funds. He will package the product according to the characteristics of each country, and then go to raise funds.” Chinese Investors Lao Lei, figured out the trick. He once bought a US private equity fund, for which more than 500,000 yuan was lost.

In addition to conventional sales methods, Lao Lei told the market that some financial or wealth companies will also hire many beautiful young ladies, who will use “beauty tactics” to let you buy overseas financial products. In addition to high returns, these products often claim that their backers are overseas listed companies. However, roses have thorns.

Interlaced like mountains. Many investors do not understand the business model of the financial products they purchase, nor do they realize that China’s investment thinking is not applicable overseas. When allocating overseas assets, in addition to the operational risks of the selected investment institutions, there are market risks, exchange rate risks, legal risks, etc.

Take the Congo for example. Most investors are attracted by Congo’s rich mineral resources and cheap labor. However, the country’s law stipulates that the discovered raw ore cannot be exported, and certain processing procedures must be carried out on the mined ore before it can be exported. However, the export tariffs imposed on all foreign-invested enterprises are very high. If investors lack understanding of the investment environment in Congo, it is easy to cause illegal acts and economic losses.

More importantly, in addition to domestic formal channels, other overseas asset allocation models are on the edge of the law. Taking the Toyotomi case as an example, “According to Japanese law, it is illegal to sell off-plan properties to Japanese residents. But if they are sold to non-Japanese residents, that is, overseas residents, this is a legal gray area.” Song Wei pointed out.

Even if the investor has USD funds in the overseas account, does the institution that conducts overseas asset allocation (whether domestic or foreign) obtain the corresponding qualifications? Investors overseas who do not have U.S. dollar funds, how do their funds go out? It’s murky here.

After seeing the truth about overseas asset allocation, Hu Feng resolutely left the company he worked for, which is the branch of an overseas asset management company in China. “It is essentially illegal to do this kind of propaganda in China.” Although it is quite difficult to prosecute overseas companies, at least one thing is certain, “Whether it is the financial platform in the Derui Capital case or the real estate service company in the Toyotomi case, have these institutions achieved compliance? Have they done their best? Necessary audit obligations?” He Chen asked.

Based on this, Hechen suggested that when investors choose an institution, they should first confirm whether it is safe and reliable, whether it has the corresponding investment or service qualifications, and whether it is supervised by the corresponding regulatory agency, etc., and then consider its investment service capabilities.

When the black swan of risk strikes, the phrase “finance is the management of risk” is always mentioned. Many investors hope that while the wealth in their hands will increase in value in the capital market, it is best to have easy access. However, it is the investors themselves who are ultimately responsible for the assets.

How to catch up with the upsurge of overseas asset allocation, this is obviously a technical job.

(Hechen, Hu Feng and Feng Shaoqi are pseudonyms in the text)

This article is reproduced from: http://finance.sina.com.cn/tech/csj/2022-09-19/doc-imqqsmrn9691505.shtml

This site is for inclusion only, and the copyright belongs to the original author.