In 2021, the revenue of the petrochemical segment of Wanhua Chemical (SH600309) surpassed that of the polyurethane segment for the first time. The revenue of the two is 61.4 billion and 60.4 billion respectively. From the perspective of projects under construction, the petrochemical sector may continue to grow. Although the gross profit margin of the petrochemical sector will reach 17% in 2021, after looking at the gross profit margin for 2016-2020, some people may feel that it is not easy to make money in the petrochemical business. From 2016 to 2020, the gross profit margins of Wanhua Chemical’s petrochemical sector were 14.2%, 12.48%, 9.98%, 11.15% and 4.26%, respectively. Compared with Wanhua’s strong polyurethane sector, the gross profit margin was over 30%, and the petrochemical business was profitable. The ability is simply weak. With the further expansion of Wanhua’s petrochemical business, will this problem of increasing revenue and not increasing profits always exist?

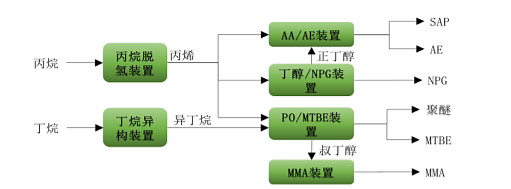

If you compare it with companies of the same type, you will find that Wanhua does not seem to have corresponding advantages, and even the disadvantages are quite obvious. From 2016 to 2020, Wanhua’s petrochemical business mainly relies on a set of 750,000 tons of propylene produced by PDH and a set of 650,000 tons of isobutane produced by a butane isomerization unit, and extended to acrylic acid and acrylate neopentane. Alcohol, propylene oxide, MTBE and MMA. There are no listed companies that completely overlap in the industrial chain, but there are companies that only do one segment. For example, Donghua Energy, which has the most PDH units in China, is mainly engaged in the production of propane dehydrogenation and polypropylene, and its industrial chain is shorter than that of Wanhua’s petrochemical business. By 2020, Donghua Energy will further classify its business, the gross profit margin of propylene will reach 19.86%, and the gross profit margin of polypropylene will reach 28.13%. Wanhua’s long industrial chain does not seem to have an advantage, and it will even fall behind in 2020.

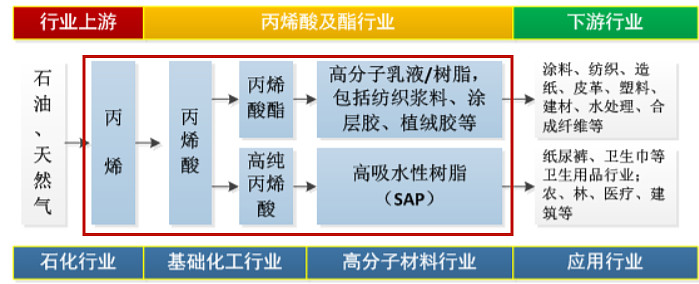

When compared with satellite chemistry, the gap appears to be even greater. The industrial chain link of Satellite Chemical is the part selected by the red box as shown in the figure below, which also overlaps with part of Wanhua’s petrochemical business. From 2016 to 2020, the gross profit margin of Satellite Chemical was 22.28%, 24.5%, 20.69%, 26.11% and 28.7%, respectively. The gross profit margin of Wanhua’s petrochemical business is obviously not as good as that of Satellite, and the gap has even reached more than 10 percentage points.

First of all, because of different statistical calibers, Wanhua Chemical’s petrochemical segment includes LPG trade with very low gross profit margins. From 2016 to 2020, Wanhua’s petrochemical business increased from 8.268 billion to 23.085 billion, and revenue increased by 179%. During this period, no large petrochemical plants were put into operation. In terms of production volume, the Wanhua Petrochemical segment produced 1.345 million tons of products in 2016 and 1.879 million tons in 2020, an increase of only 40% in output. During this period, the price of petrochemical products did not increase much, which can also be seen from the gross profit margin of Donghua and Satellite. During this period, the main incremental contribution was the LPG trade, and this business was not very profitable. Referring to Donghua Energy’s LPG trade, it has gradually declined from 5.52% in 2016 to 1.03% in 2020. If Wanhua’s 2020 LPG trade is calculated with reference to Donghua Energy’s 1.03%, and the trade business is 12 billion, the gross profit margin of Wanhua’s PO/AE units will also be less than 10%.

Secondly, Wanhua’s internal digestion of the petrochemical sector before 2020 was not included in the corresponding revenue. For example, Wanhua Chemical uses the PO/AE unit to produce 250,000 tons of propylene oxide, which is further reacted to generate polyether. There is no external sales of propylene oxide, and no revenue or profit is generated. There are similar problems in the acrylate business. With more and more internal digestion, if these businesses are not accounted for, it cannot truly reflect the operation of the petrochemical sector. For this reason, the 2021 annual report adjusted the calculation caliber, and included products similar to propylene oxide in the revenue of the petrochemical sector at the market price. As shown in the table below, there was no inter-product offsetting account before, and it will be available starting in 2021. Looking back to 2020 according to the data disclosed in the table below, the revenue of the petrochemical series should be 26 billion, with a gross profit margin of 7.64%. If you exclude the meagerly profitable LPG trade, the gross profit margin of Wanhua PO/AE units should be around 13%.

Finally, there is an MTBE business that pulls down gross margins. The method used by Wanhua Chemical to produce propylene oxide will produce a large amount of by-product MTBE, and this product has the lowest unit price among all Wanhua products, and is often not as good as the price of propylene and isobutane. Due to limited data, it is difficult for us to calculate the gross profit margin of several other items after excluding the MTBE business, but at least it is higher than 15%.

Based on the above analysis, the gap between Wanhua’s petrochemical business and its peers is not as big as it is roughly seen. Due to the wide variety of products and the existence of a potentially unprofitable by-product, MTBE, we cannot assess whether there is an advantage over satellite chemistry in the acrylics and esters business. If it were not for the production of propylene oxide, Wanhua would not have this business. And this process brings a lot of by-products. Wanhua produces 250,000 tons of propylene oxide in the PO/AE unit, and 760,000 tons of MTBE by-products are produced. It is precisely because this by-product is not easy to deal with, so Wanhua will use PO/SM device for the propylene oxide plant that will be put into operation, producing 300,000 tons of propylene oxide and 650,000 tons of styrene. The price of styrene is also significantly higher than that of MTBE, and its downstream applications are wider, and the industrial chain can be further extended when circumstances permit. Of course, the cost of extending the industrial chain may bring new by-products. In order to further invest to make up for the weakness of the polyether business, Wanhua has also developed the POCHP technology, which will have no by-products. After solving the problem of by-products, all Wanhua products do not have the kind of products that fall into losses as soon as the weak cycle is reached. It’s just a matter of earning more and earning less. Judging from the operating results over the years, Wanhua’s management is still reliable. In the newly planned Penglai Industrial Park, an employee stock ownership platform has also been introduced, and the investment amount is also huge. We have reason to believe that Wanhua’s petrochemical business can bring more profits.

There are 8 discussions on this topic in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/8743289683/222018592

This site is for inclusion only, and the copyright belongs to the original author.