Let’s start with the conclusion : I think the Tongwei module incident was amplified by emotions last Friday, and the actual impact was not so great. Next week should be a better time for photovoltaics to replenish their positions. If photovoltaics continue to be affected by the Tongwei incident Fall, may wish to boldly increase positions .

I don’t quite understand why snowball people have been looking down on components, but I think components are a very barrier link. The barriers are not reflected in technology, but in channels, brands, management, and supply chains ; for example , Are there any barriers to mineral water technology? Why is Nongfu Spring’s market value of hundreds of billions? There are also charging treasures and charging cables that you can find in any small workshop in Huaqiangbei, so why Anker Innovation can make this business global and make it a company with a market value of tens of billions.

Snowball, I usually say conclusive things directly. For example, in yesterday’s post I talked about some conclusions about overseas and distributed and new batteries: web link

Today I want to share my thought process and some interesting data and materials to demonstrate why I came to these conclusions and how I should look at components in the future:

1. From the data point of view, contrary to what most people think, modules are one of the few industries in which CR5 is concentrated in the photovoltaic sector. In 2021, CR5 will account for 76% . For some links with more “technical barriers”, such as silicon wafers, the competitive landscape is becoming more and more fragmented. Below I will explain why?

2. To understand components, you must know that in most cases, components are closer to a to C business, and channels, word-of-mouth, brand, and supply chain are more critical, rather than the to G scenario of centralized power stations. And most of the leading module manufacturers are actually based overseas. For example, Trina Solar, JA Solar and JinkoSolar all account for more than 70% of their overseas revenue. Most of the remaining 30% of domestic revenue is distributed photovoltaics. It is the scene on the household and industrial side, so what Tongwei can really affect is the centralized photovoltaic, which itself does not account for a large proportion of the revenue of the leader.

3. Even in the scenario of centralized photovoltaics, if you carefully check the previous bidding data, basically the second-tier module manufacturers will bid 5 cents to 1 cent lower when they compete with the first-tier ones. Therefore, for a newcomer like Tongwei, this is a normal tactical behavior and cannot rise to a strategic height. But because it was Tongwei this time, the capital market amplified this sentiment.

So is it possible for Tongwei to build channels, brands and supply chains in a short period of time with sufficient capital advantages and then attack traditional leaders? In other words, is Tongwei’s future strategic center a component?

My conclusion is that it is still difficult, or that this is not even Tongwei’s own strategy . Let’s break it down one by one.

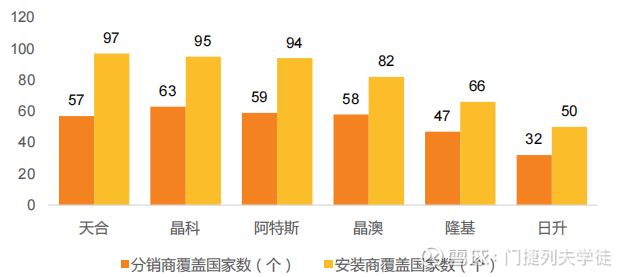

In terms of channels; we take Trina Solar as an example to see how much time and effort it takes to build the current channel advantage. First of all, in terms of time, it took Trina Solar 20 years to establish a channel network in 97 countries. In terms of the number of distributors and installers, Europe (138 distributors, 761 installers), India (21 distributors, and installers) 152), Australia (32 distributors, 569 installers).

Anyone who has done business here knows that it is not so easy to go abroad to a country. Don’t talk about going to a country, you are a company in Sichuan going to the neighboring Hubei to do business. It is estimated that you are not familiar with the place. It is necessary to understand local policies and regulations, and to have a good relationship with the local local snakes. The establishment of trust relationships with channel dealers is also a matter of eating meat, drinking and binding interests.

Speaking of the United States separately, the leading JinkoSolar and Trina Solar have both suffered lawsuits and losses in the United States. To do business in such a country, you even need to have a legal team and go through the process of others to know where the pit is.

BTW, I have never seen a business that relies on offline channels to be overtaken by competitors in a short period of time, unless photovoltaics can be Internet + in the future.

In terms of brand; because the use cycle of components is 25-30 years long, many offline quality assurance and after-sales teams are often required, which will actually make customers trust the brand more. In addition, component brands with “financeable” brands can help project development. Bank financing, and the performance of various aspects of the product is an important basis for evaluating bankability.

According to the evaluation results in 2021, the bankability ratings of JA Solar, LONGi, TRW, Canadian Solar and Jinko are among the top.

Having said so much, just remember one thing. The brand of the company that has to C is not important. Dealers are reluctant to pick up a new brand. One is that it is not easy to get loans, and the other is that users do not accept it.

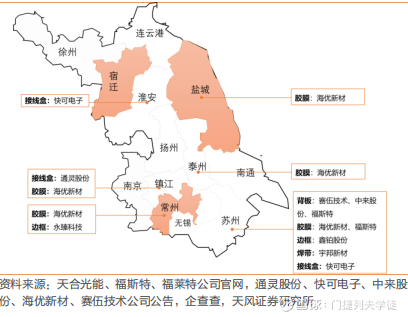

In terms of supply chain; there are indeed no barriers to component manufacturing, but the difficulty lies in the fact that this is more than the auxiliary materials and supply chain support required for silicon materials, batteries, silicon wafers and other links. To make a component requires adhesive film and backplane , glass and other auxiliary materials, or take Trina Solar as an example, the production base and auxiliary material enterprises form an industrial cluster, which can effectively reduce transportation costs and help to form a long-term and stable strategic partnership. Around the production base, there are a number of films (Haiyou New Materials, Foster), backplanes (Saiwu Technology, Jolywood, etc.), frames (Yongzhen Technology, Xinbo), welding strips (Yubang New Materials, etc.) ) and junction box (Tongling Co., Ltd., Kuaike Electronics) auxiliary material enterprises.

Seeing this, everyone should have a feeling. Of the three mentioned above, none of them can be built within 1-2 years, and there is no need to build them. After all, silicon materials and batteries are already enough to make money. So this is my guess after all, so what about Tongwei’s own signs? Obviously, neither .

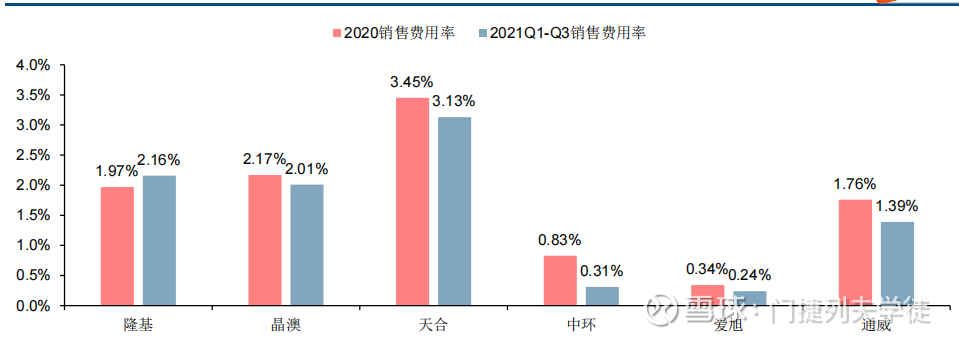

Speaking of a set of core data, module manufacturers such as LONGi, Trina Solar, and JinkoSolar must spend money to do the above things, such as setting up teams overseas or in China, advertising, bank loans, and asking for distribution. Business dinner and so on. It is reflected in the financial statements that the sales expenses are very high. The following picture is very intuitive:

This picture is very intuitive. Basically, the sales cost is 2-3 points higher than that of pure silicon wafers and batteries. Then, according to the 2022 semi-annual report that Tongwei shares has released, the sales cost is 490 million, compared with 400 million last year, only 90 million more than last year. No matter how you look at it, it doesn’t feel like you’re going to attack components in a big way.

Tongwei’s strategic center should still be on silicon materials and cells. The capital expenditure of these two is already very large and it is enough to make money.

This topic has 104 discussions in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/2874741935/228602281

This site is for inclusion only, and the copyright belongs to the original author.